The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

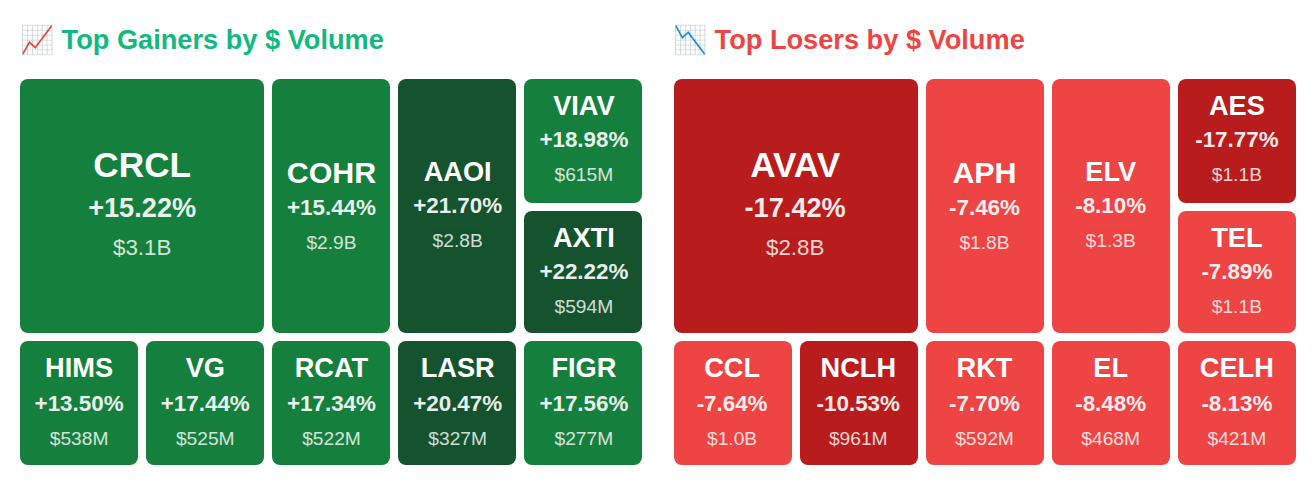

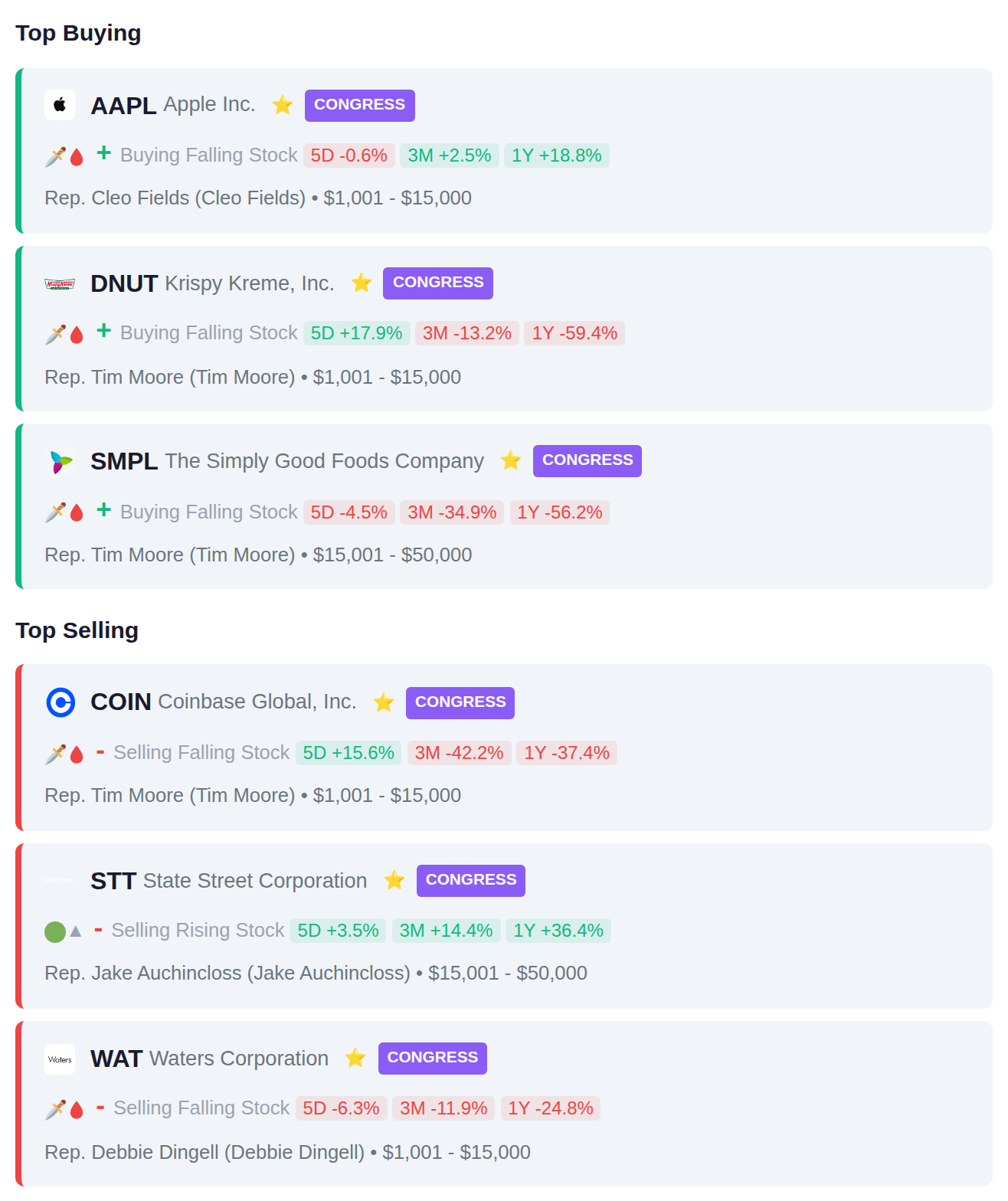

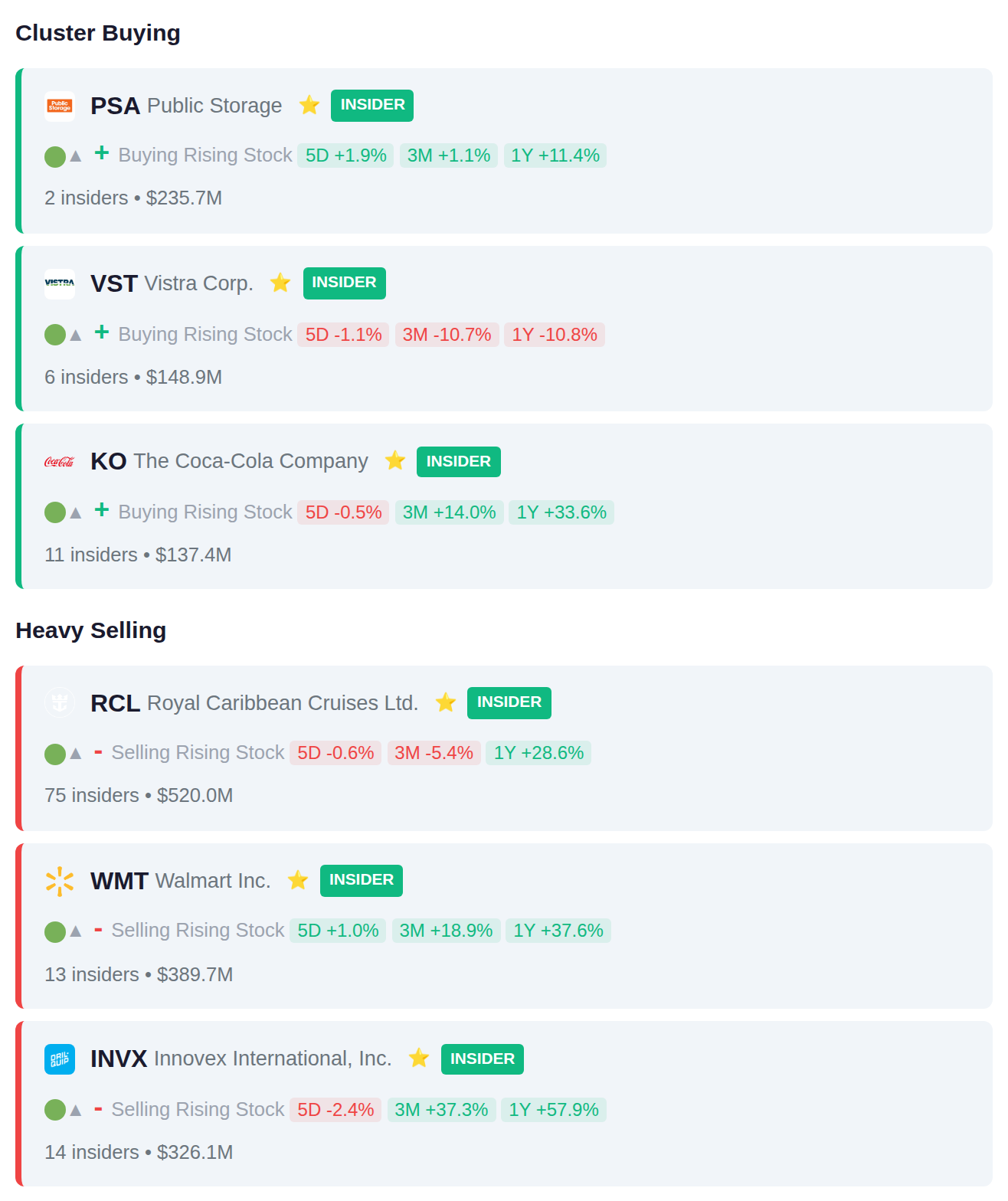

While Rep. Cleo Fields (D-LA) quietly picked up Apple Inc. (AAPL) shares worth up to $15,000, a stampede of 75 insiders at Royal Caribbean Cruises Ltd. (RCL) dumped a staggering $520.0 million in stock—the kind of exodus that makes you wonder what they're seeing on the horizon. Meanwhile, aftermarket traders went absolutely feral over laser tech, sending Lumentum Holdings Inc. (LITE) up 11.8% and Coherent Corp. (COHR) up 15.4% on conference room whispers and Nvidia name-drops, while Circle Internet Group Inc. (CRCL) rode USDC mania to a 15.2% pop. Here's what smart money is doing today.

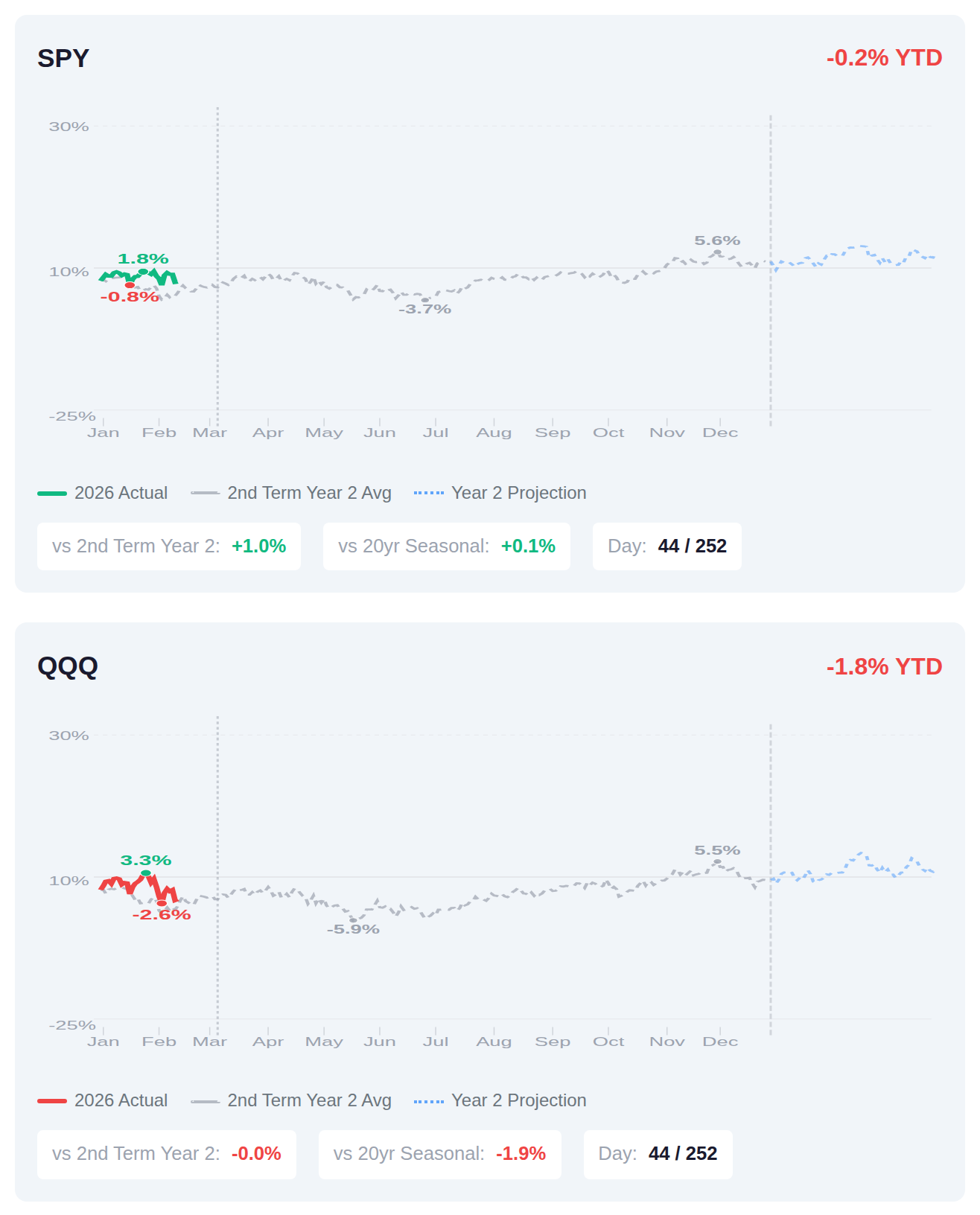

We're 44 days into what historically ranks as the weakest year of the presidential cycle, and the S&P 500 is running roughly 1% ahead of the typical second-year trajectory despite being slightly red year-to-date. The Nasdaq's 1.8% decline has it tracking right in line with historical second-year performance, which tends to see choppiness through the first half before institutional money typically returns in Q4. If the pattern holds, history suggests the final three quarters of second-term Year 2 have added an average of 3.3% from current levels, though smart money positioning data through mid-March will be the real tell on whether this cycle follows the script.

📚 Jargon Buster

Rug Pull

Crypto founders promise you the moon, then yank the liquidity and disappear to Dubai with your life savings. Surprise, honey!

The VIX currently sits at 19.86, remaining within normal ranges despite a 4.0% weekly increase, suggesting equity markets are experiencing measured uncertainty rather than distress. Meanwhile, the MOVE index jumped 28.6% week-over-week to 12.95, though this sharp percentage gain still leaves bond market volatility at historically low levels. This divergence indicates that while equity investors are pricing in moderate risk, fixed income markets continue to reflect relative calm about interest rate movements.

|| Market Sutra ||

"Sharp rallies in downtrends are invitations, not reversals."

— 2001–2002 had massive bear-market rallies before lower lows.

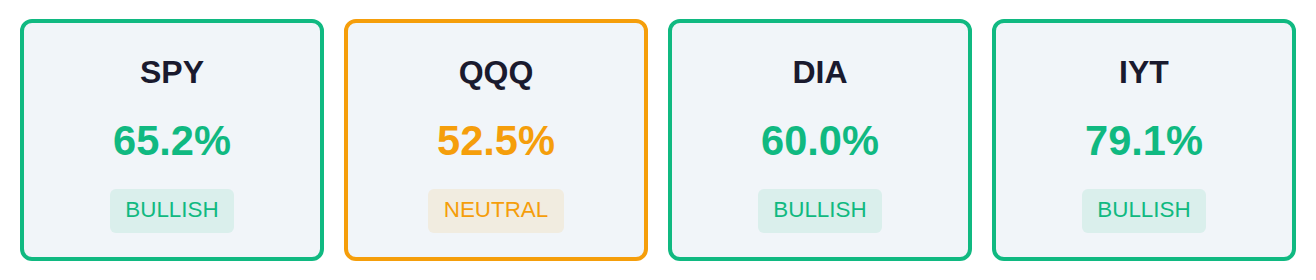

Market breadth shows defensive positioning with Materials, Utilities, and Consumer Staples leading at 97-100% participation rates, while growth-oriented sectors lag significantly with Communication, Financials, and Technology registering below 50% breadth. Transportation stands out with 79% breadth despite broader market divergences, as the Nasdaq shows notably weaker internal participation at 52% compared to the S&P 500's 65%. This configuration reflects a risk-off environment where capital has rotated toward traditional defensive plays while growth and cyclical sectors experience reduced participation.

As of February 25, Fed net liquidity stood at $6.61 trillion, essentially flat with a week-over-week increase of just $0.4 billion—indicating stable monetary conditions with minimal change in the liquidity available to financial markets. The next H.4.1 data release drops Thursday, March 5, which will show whether the Fed's balance sheet operations are continuing to provide steady liquidity support or if conditions are beginning to shift.

Yesterday's ISM Manufacturing PMI came in at 52.4, beating the 51.3 estimate by 1.1 points but still slightly below January's 52.6, keeping the manufacturing sector in expansion territory for the third consecutive month after contracting for 16 of 17 months through November 2024. The employment component at 48.8 beat expectations of 48.0 but remains in contraction for the 14th straight month, suggesting factories are still reluctant to add workers despite improved business conditions. Tomorrow's focus shifts to the services sector with ISM Non-Manufacturing PMI expected at 53.5 and ADP Employment at just 19,000—down from 22,000 prior—ahead of Friday's official jobs report, while the Fed's Beige Book will provide granular regional economic intelligence as policymakers assess whether the economy can handle restrictive rates with the Economic Surprise Index holding flat at +1.2.

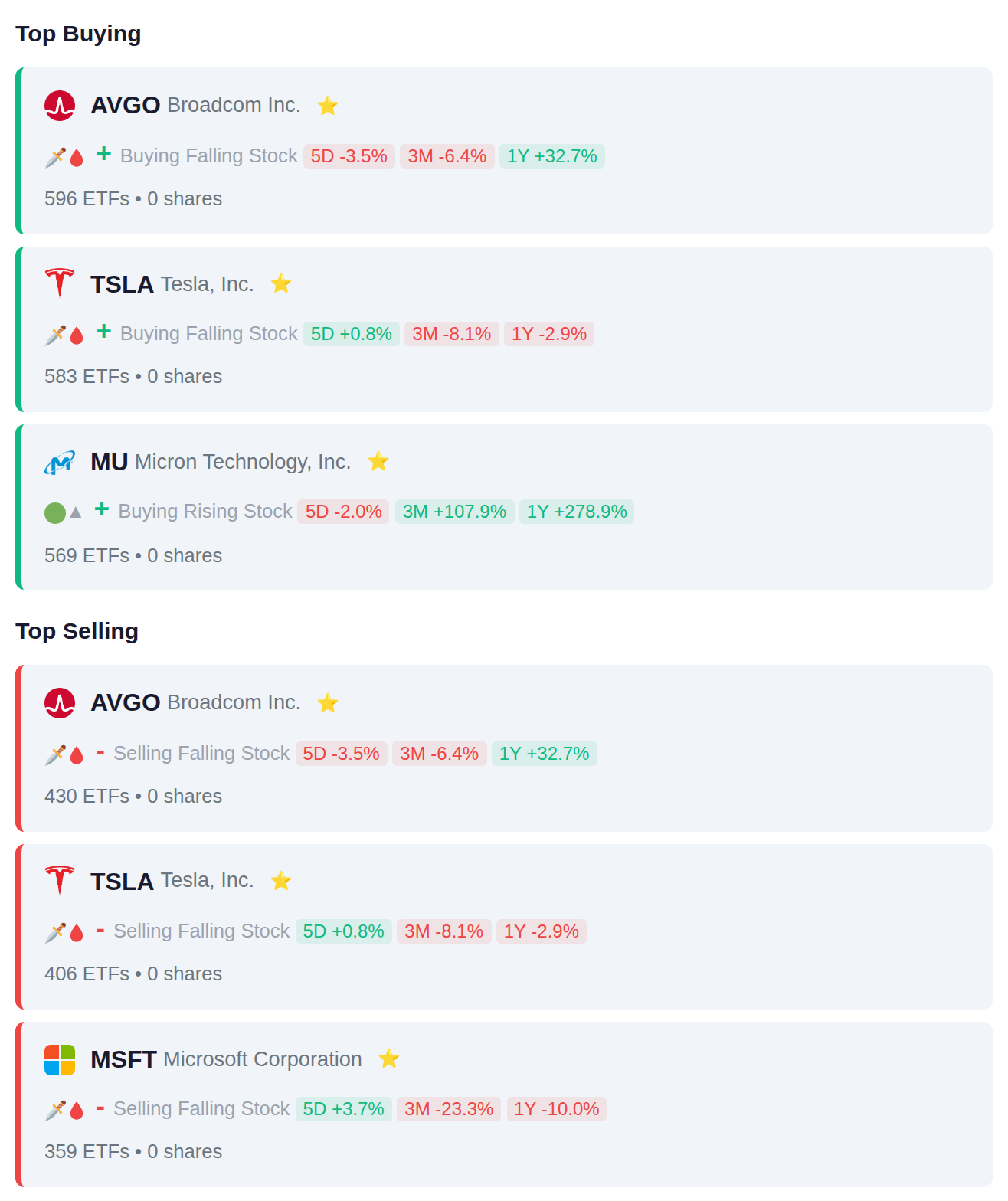

Exchange-traded funds displayed mixed positioning in technology holdings during the latest period, with 10 ETFs adding exposure and 10 reducing it across the sector. The flow data revealed concentrated activity in semiconductors (AVGO, MU) and electric vehicles (TSLA), where roughly 60% of position changes were additions rather than reductions, while mega-cap software (MSFT) saw primarily exits.

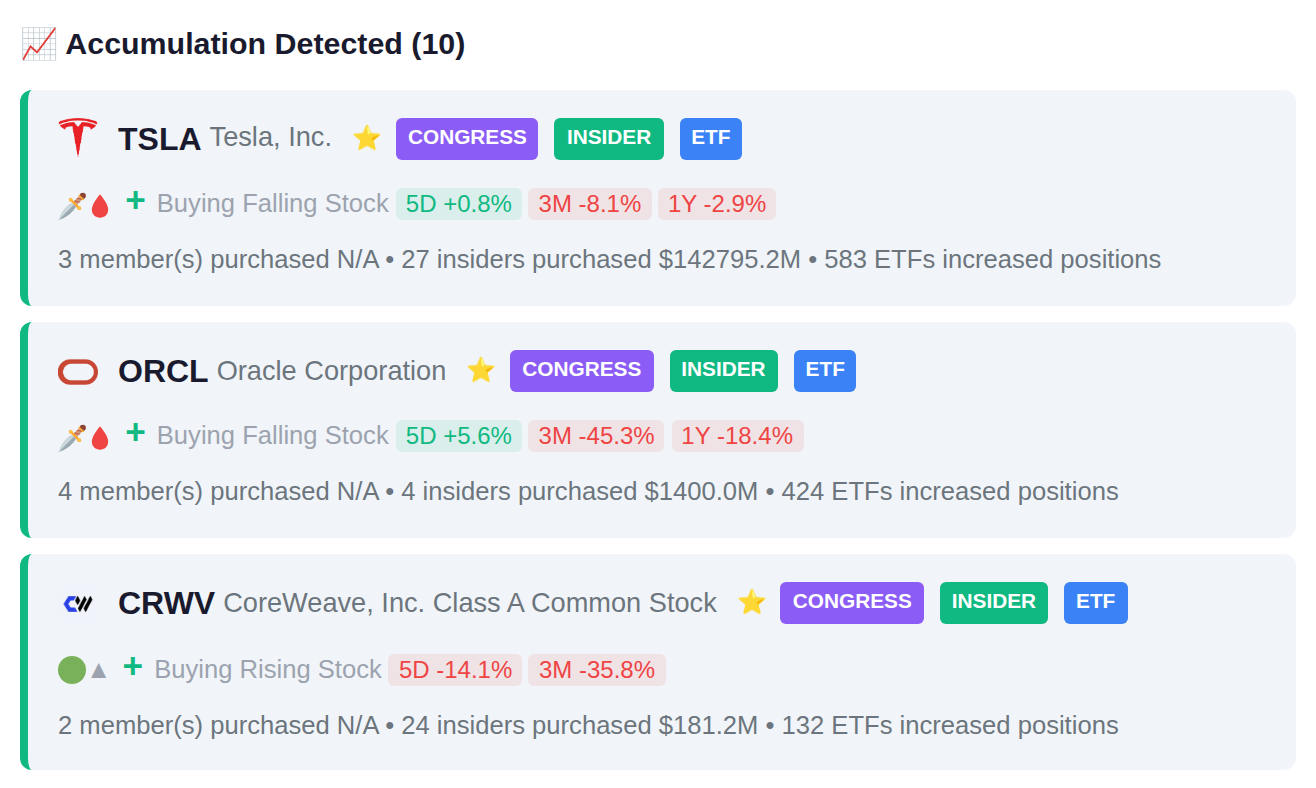

Congressional trading activity this period showed Rep. Tim Moore executing multiple transactions, purchasing positions in DNUT and SMPL while exiting COIN, alongside Rep. Cleo Fields adding AAPL shares. Additional selling activity included Rep. Jake Auchincloss reducing STT holdings and Rep. Debbie Dingell divesting from WAT.

Insider activity showed balanced signals this week with notable cluster purchases at KO where 11 insiders accumulated shares and at VST where 6 insiders added positions. On the distribution side, RCL recorded the largest cluster activity with 75 insiders collectively selling $520.0M in shares, followed by significant selling at WMT where 13 insiders reduced positions totaling $389.7M.

355 companies report earnings today, with INCO.JK and ADRO.JK showing recent accumulation patterns heading into their announcements, while BYAN.JK and BBAR.BA have experienced distribution activity. Yesterday's session saw significant moves with DRVN dropping 33.3%, ASTH surging 32.8%, and TDGMW advancing 26.0%. Tomorrow's calendar includes 290 companies scheduled to report quarterly results.