The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

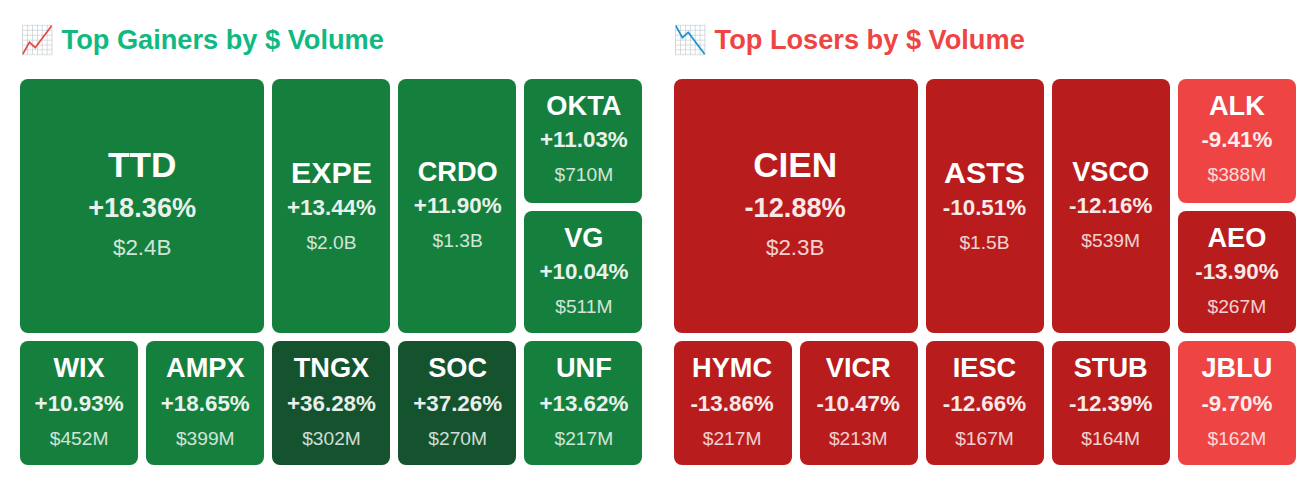

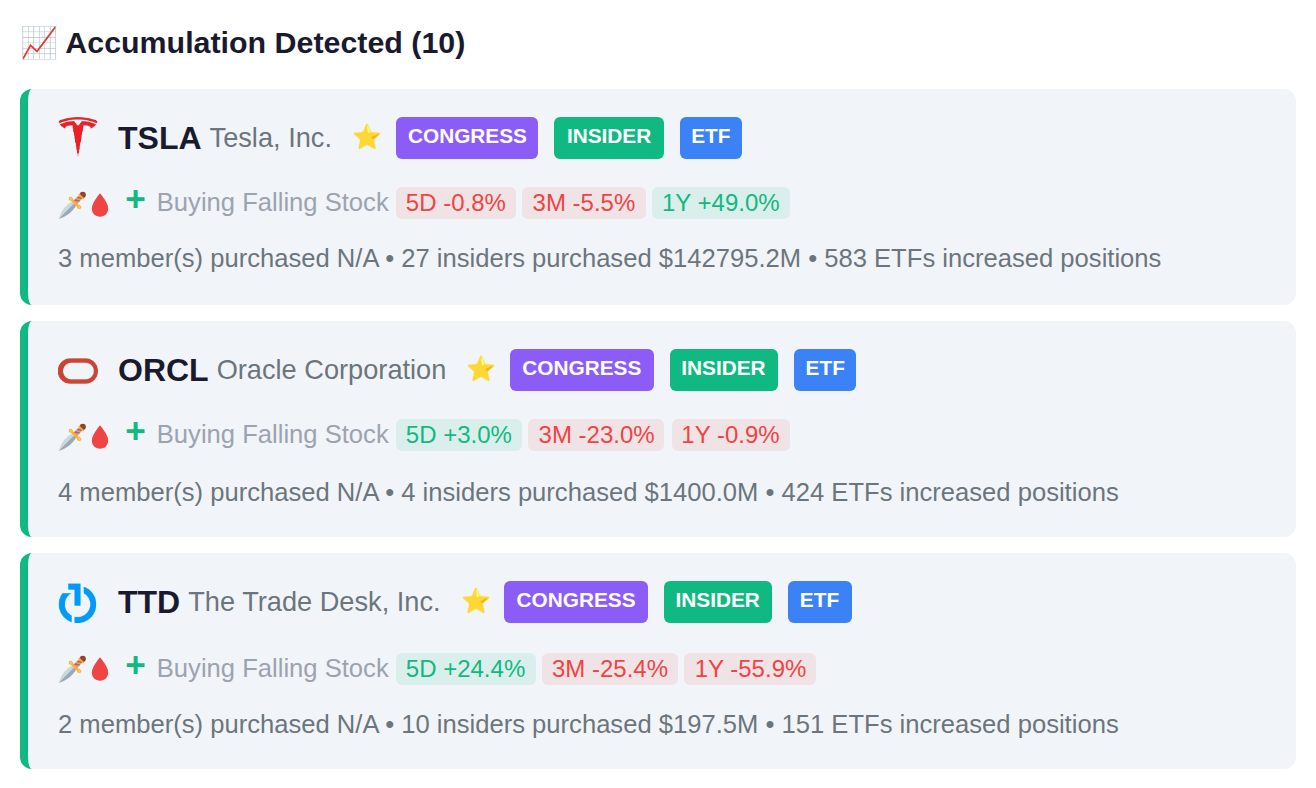

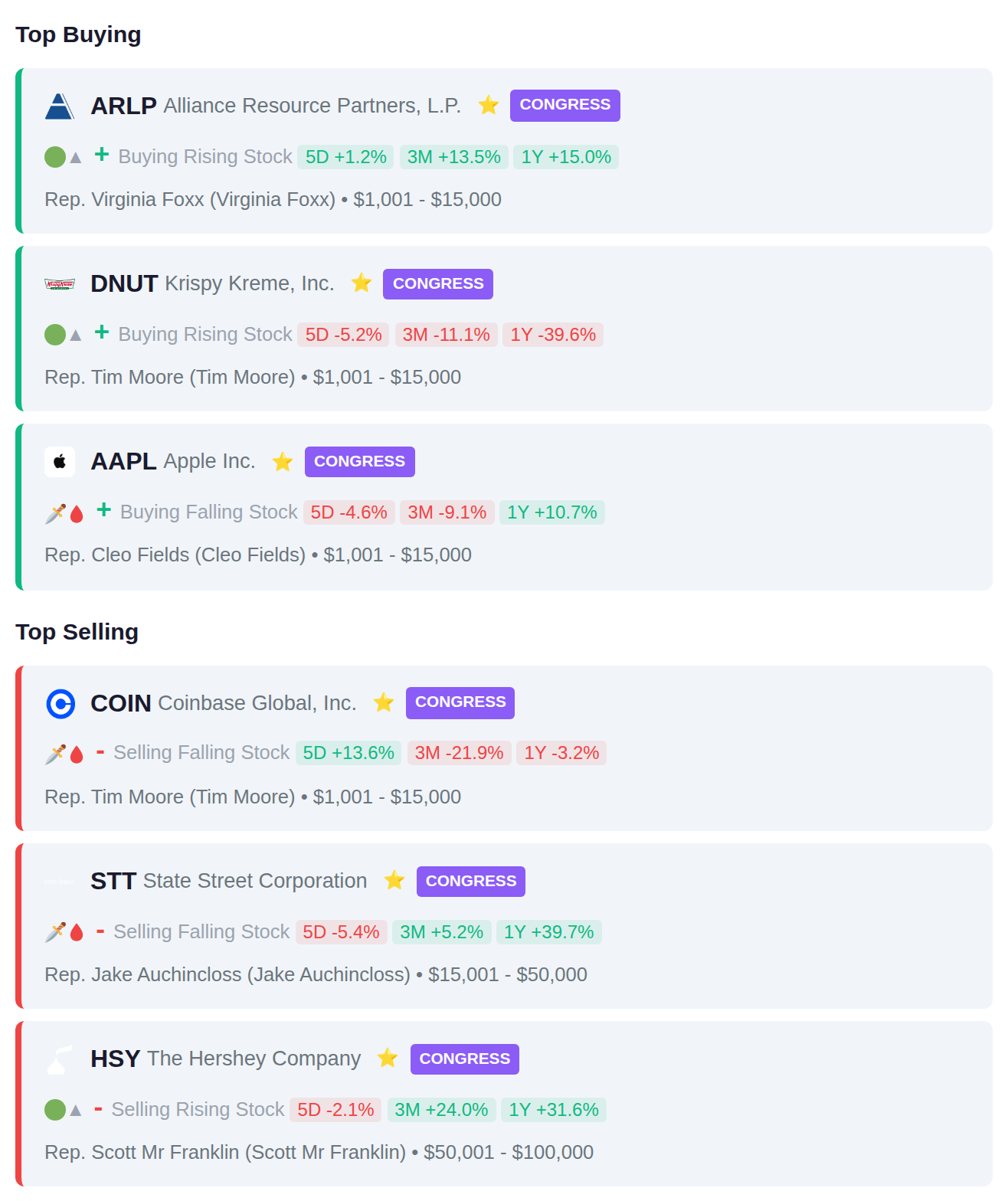

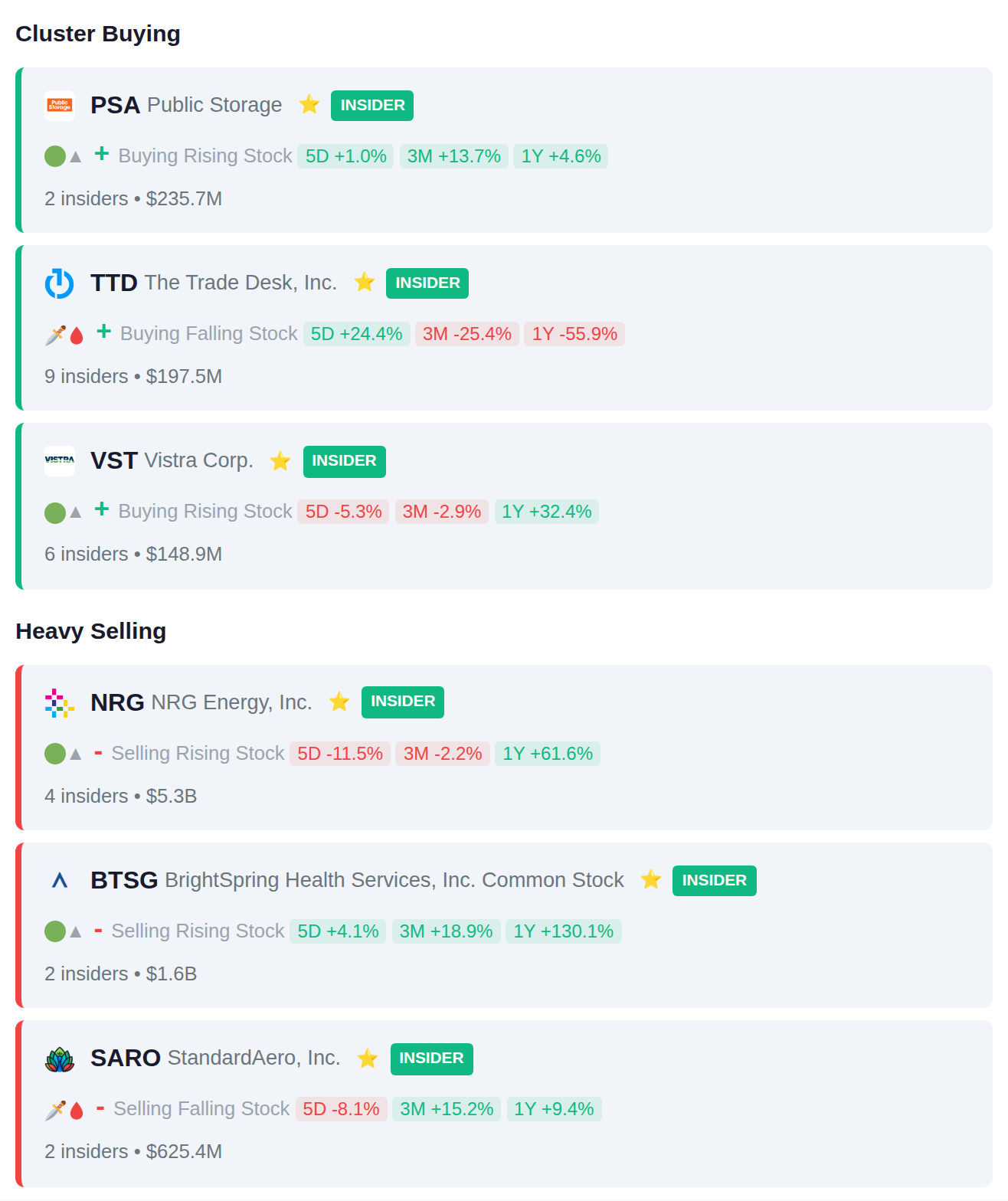

While Rep. Virginia Foxx quietly added Alliance Resource Partners (ARLP) to her portfolio, NRG Energy (NRG) insiders executed a staggering $5.3 billion in sales—part of a $9.1 billion net outflow day that had smart money heading for the exits even as the VIX spiked 18% and CEOs like Jeff Green at The Trade Desk (TTD) doubled down on their battered stocks. Meanwhile, OpenAI's e-commerce ambitions spooked nobody who matters: Booking Holdings (BKNG) rocketed 8.5% and Expedia (EXPE) surged 13.4% after hours as institutional traders shrugged off AI checkout fears. Here's what smart money did today while everyone else was panicking about travel bots.

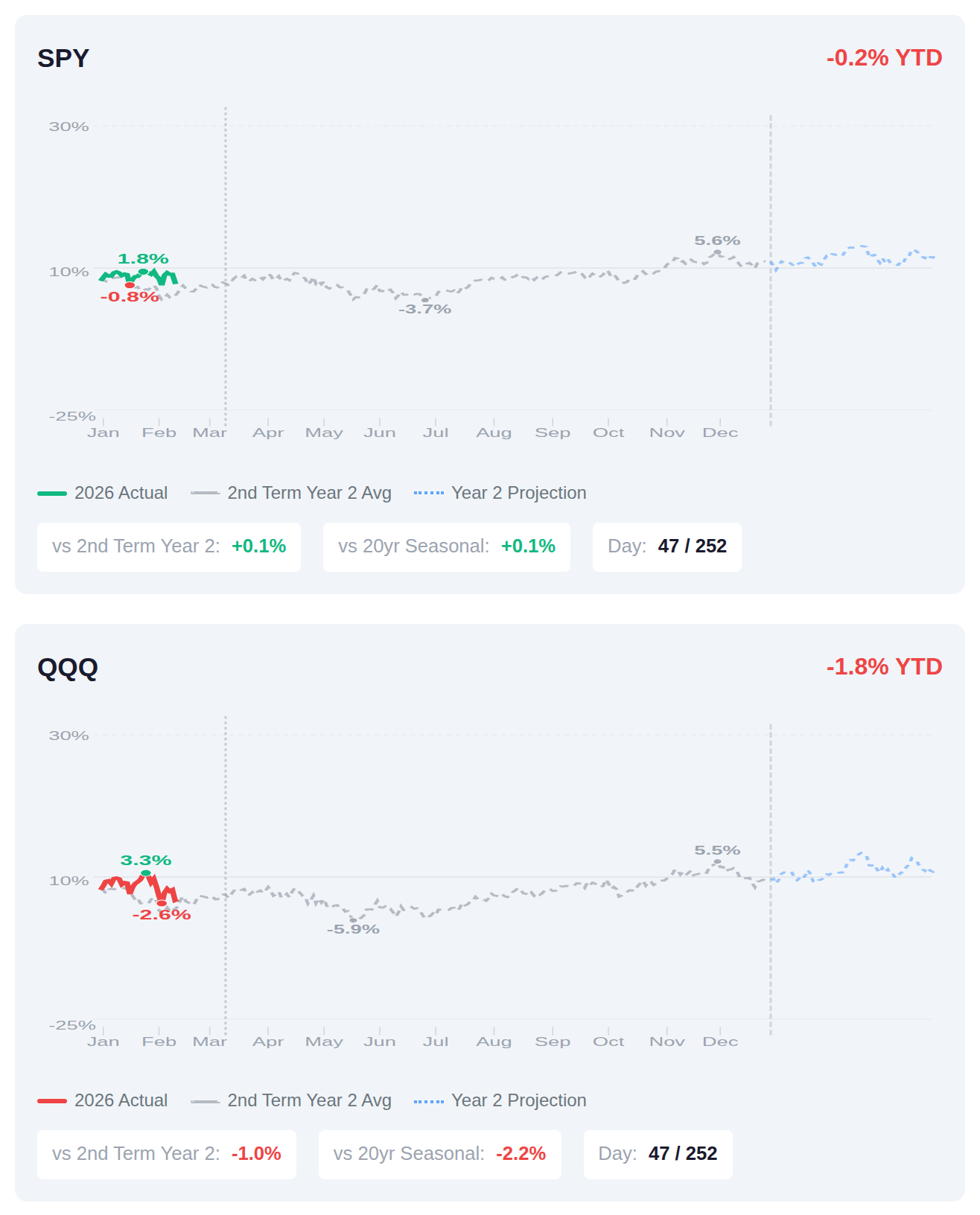

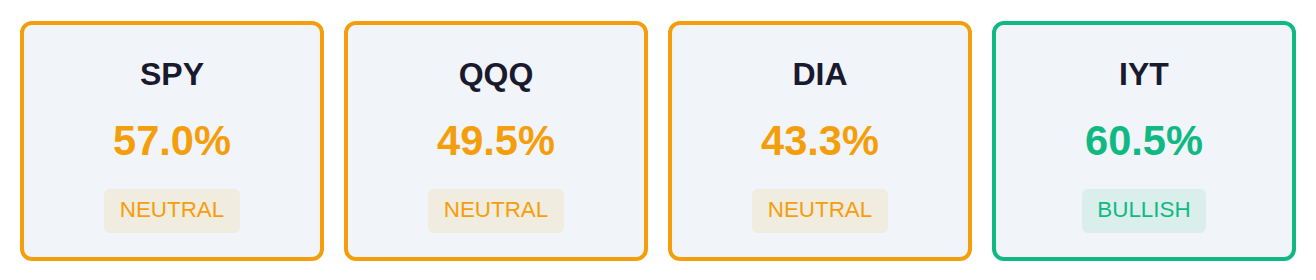

We're about a fifth of the way through Year 2 of Trump's second term, and the major indices are tracking remarkably close to historical norms—SPY sits just 0.1% ahead of the typical 2nd Term Year 2 pattern while QQQ lags by about 1%, which isn't unusual given tech's volatility in midterm cycles. Historical data shows Year 2 tends to be the choppiest of the four-year presidential cycle, averaging around 3.5% for the full year with most of those gains backloaded into the second half, though the next six weeks through mid-March have historically added another 1.5% as Q1 earnings season unfolds. The current performance suggests we're right in the middle of the typical Year 2 sideways grind that historically precedes stronger action as political uncertainty around the midterm elections starts getting priced in later this spring.

📚 Jargon Buster

Ex-Dividend Date

The day your shares wake up poorer because the company already mailed the checks. Stock drops by the dividend amount like clockwork.

The VIX climbed 18.0% this week to reach 21.15, moving into elevated fear territory as equity market participants priced in increased uncertainty. Meanwhile, the MOVE index rose 26.3% to 14.54 but remains at historically low levels, indicating bond market expectations for volatility continue to be subdued despite the sharp weekly increase. This divergence suggests heightened concern specific to equity markets while fixed income traders appear relatively unconcerned about near-term Treasury volatility.

|| Market Sutra ||

"You trade your belief in the future, not the facts of the present."

— Early investors in Amazon had little present data—only conviction.

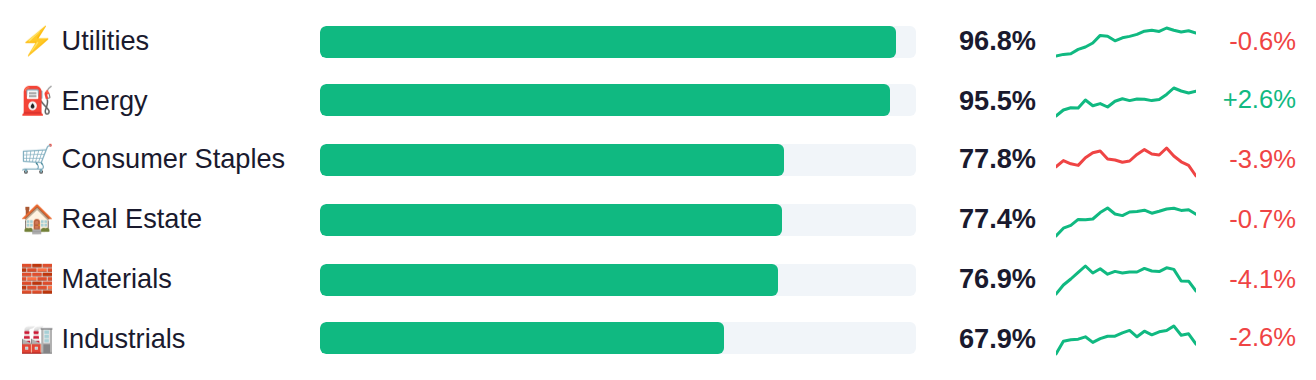

Market breadth remains middling with major indices showing participation rates between 43% and 60%, while a clear defensive rotation has emerged as Utilities and Energy lead with participation above 95% and Consumer Staples at 78%. Growth and cyclical sectors are lagging significantly, with Technology at just 33% and Financials at 30%, suggesting investors have repositioned toward traditionally defensive areas of the market. The divergence between defensive sector strength and weak participation in growth-oriented names indicates a notable shift in market character from the risk-on positioning that characterized earlier periods.

Fed net liquidity stood at $6.63 trillion as of March 04, up $15.1 billion week-over-week, indicating a modest expansion in system liquidity that historically correlates with supportive conditions for risk assets. The next H.4.1 Federal Reserve balance sheet update releases Thursday, March 12, which will show whether this liquidity expansion continues or reverses.

Yesterday's data painted a mixed picture for inflation and labor market health, with unit labor costs surging to 2.8% versus expectations of a -0.7% decline—a significant 3.5 percentage point beat that marks a sharp reversal from the -1.8% prior reading—while productivity growth slowed to 2.8% from 5.2%, missing the 4.0% estimate by 1.2 points and suggesting rising wage pressures aren't being offset by efficiency gains. Export prices also ran hotter than expected at 0.6% versus 0.4% estimates, though initial jobless claims at 213K remained near historically low levels consistent with a still-tight labor market. Today's focus shifts to the February employment report where nonfarm payrolls are expected to cool sharply to 70K from 130K—potentially the weakest reading since pandemic distortions cleared—alongside retail sales data for January that's projected at -0.3% following December's -0.1% contraction, which would mark back-to-back monthly declines for the first time since mid-2023 and raise questions about consumer resilience heading into Q1.

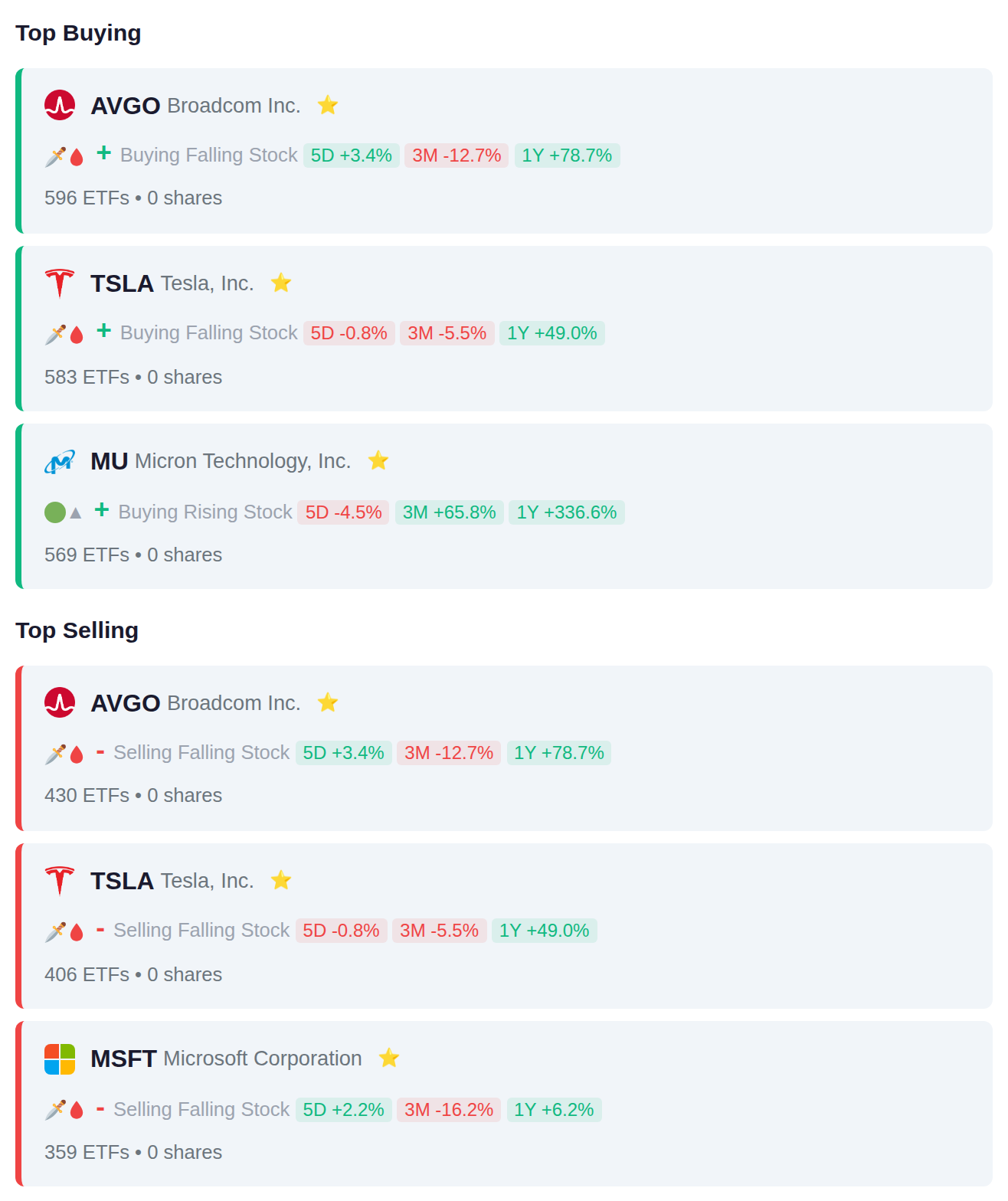

# Institutional Flow Summary Exchange-traded funds showed mixed positioning in mega-cap technology this week, with 596 ETFs adding Broadcom shares while 430 reduced their holdings, and a similar split in Tesla (583 adding vs 406 removing). The data suggests rotation within the semiconductor space, as 569 ETFs increased Micron positions while Microsoft saw net reduction with 359 ETFs trimming exposure, indicating institutional rebalancing across chip makers and software giants rather than broad sector exit.

Rep. Virginia Foxx purchased ARLP, Rep. Tim Moore purchased DNUT while selling COIN, Rep. Cleo Fields purchased AAPL, Rep. Jake Auchincloss sold STT, and Rep. Scott Mr Franklin sold HSY. The recent activity shows members adding positions in energy partnerships, consumer brands, and big tech, while reducing exposure to cryptocurrency-related stocks and financial services.

Multiple insiders accumulated shares at TTD with 9 participants and VST with 6 participants, while on the distribution side, 4 insiders at NRG collectively sold $5.3 billion in stock. The overall insider activity showed balanced signals with 15 accumulation events matching 15 distribution events across the tracked companies.

Today's earnings calendar features 123 companies reporting results, with OTP.BD and 2884.TW showing recent accumulation patterns while ARTO.JK and EDN.BA have experienced distribution activity ahead of their reports. Yesterday's session saw significant moves in TNGX, which surged 47.6%, while DSGR declined 26.7% and PMOIF advanced 21.9%. Tomorrow's calendar expands to 239 companies scheduled to report quarterly results.