The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

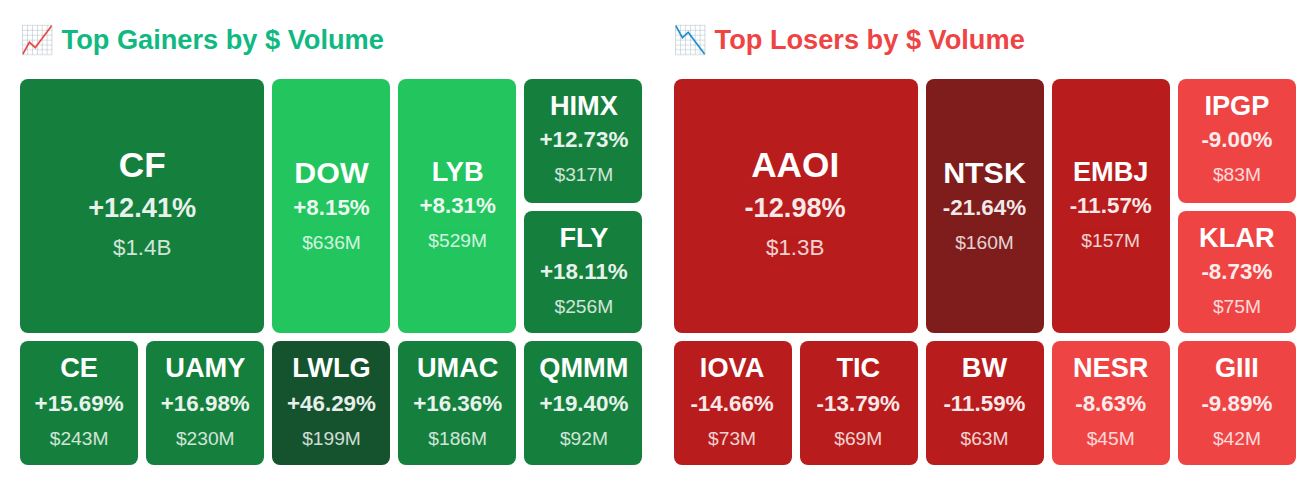

While Rep. Gilbert Cisneros (D-CA) quietly scooped up Federal Signal Corporation (FSS) shares worth up to $15,000, four insiders at NRG Energy (NRG) dumped a staggering $5.3 billion—the kind of exit that makes you wonder what they're seeing that we're not. Meanwhile, fertilizer stocks CF Industries (CF) and The Mosaic Company (MOS) are riding geopolitical chaos to double-digit after-hours gains as smart money registered a massive $9.8 billion net outflow today, even as the Fed pumped $15.1 billion in fresh liquidity into the system. Here's what smart money is doing today.

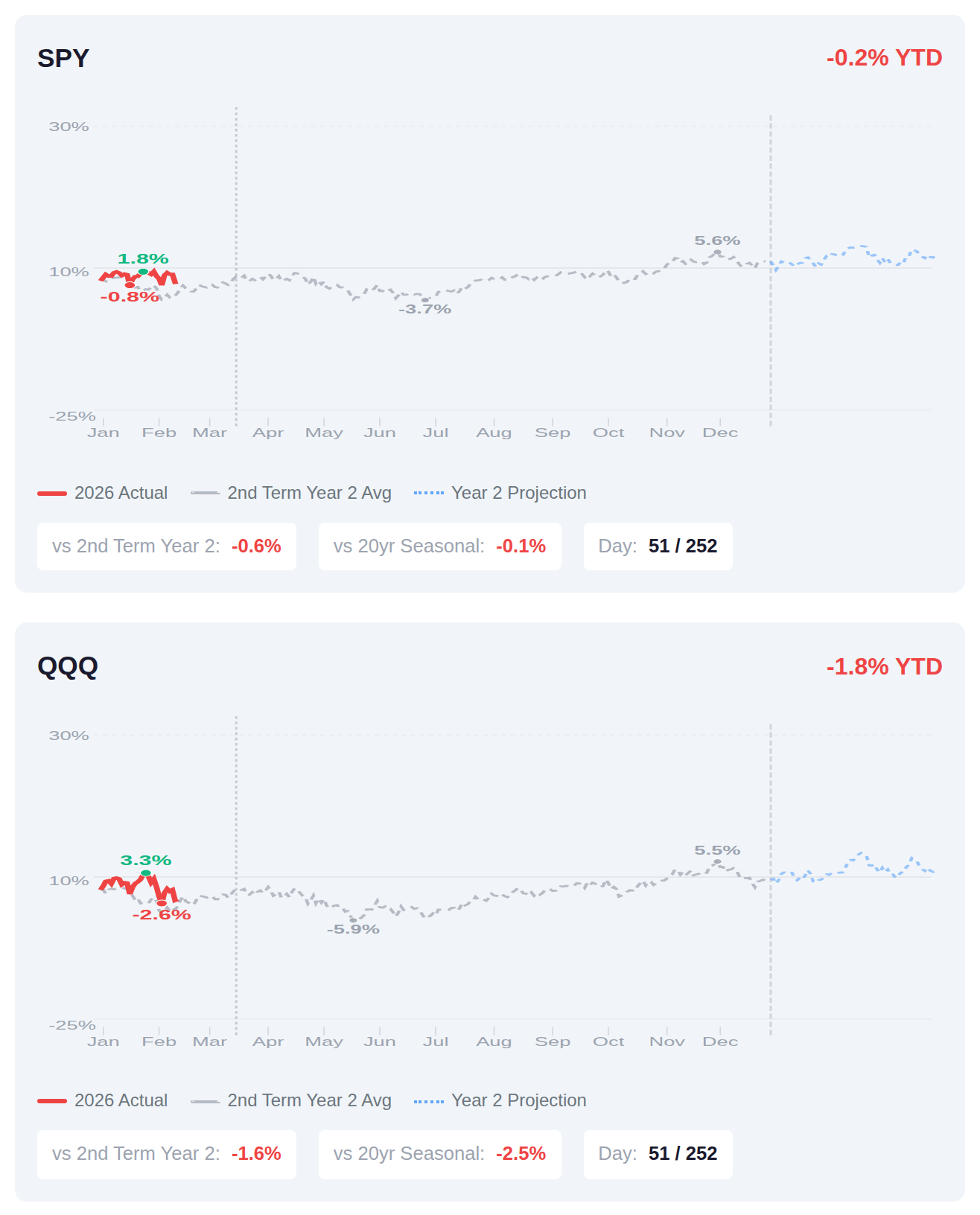

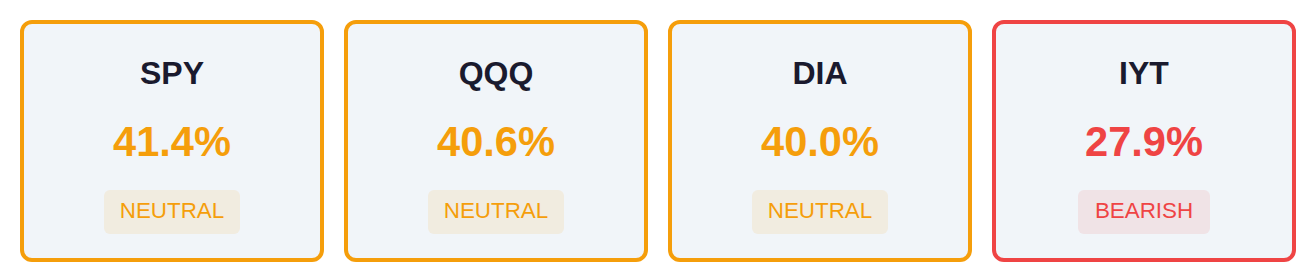

We're about 20% through the year and both SPY and QQQ are running slightly cooler than the typical second-term Year 2 pattern, with SPY sitting 60 basis points below its historical average for this point in the cycle and QQQ tracking 160 basis points under its comp. History shows second-term Year 2s have averaged 3.5% full-year returns for SPY, with Q1 typically contributing an additional 1.5% through mid-March—though we're clearly not seeing that seasonal lift materialize yet as both indices hover near flat. The presidential cycle data suggests the back half of Year 2 has historically provided the bulk of gains, but the current lag versus seasonal patterns indicates either a delayed start or a potential deviation from the typical midterm blueprint.

📚 Jargon Buster

Basis Point

One-hundredth of a percent. Wall Street’s way of sounding fancy instead of saying “0.01%.”

Equity volatility remains elevated with the VIX at 24.93, up 5.8% week-over-week and sitting just below the threshold that typically signals high fear in stock markets. This contrasts sharply with bond market conditions, where the MOVE index at 14.01 indicates unusually calm trading in Treasuries despite a modest 1.5% weekly increase. The divergence suggests investors are pricing in significantly more uncertainty for equities than for fixed income, a pattern that historically reflects concerns specific to corporate earnings or equity valuations rather than broader systemic or monetary policy risks.

|| Market Sutra ||

"The market forgives slowness, but never stubbornness."

— Kodak refused to adapt to digital—market moved on without it

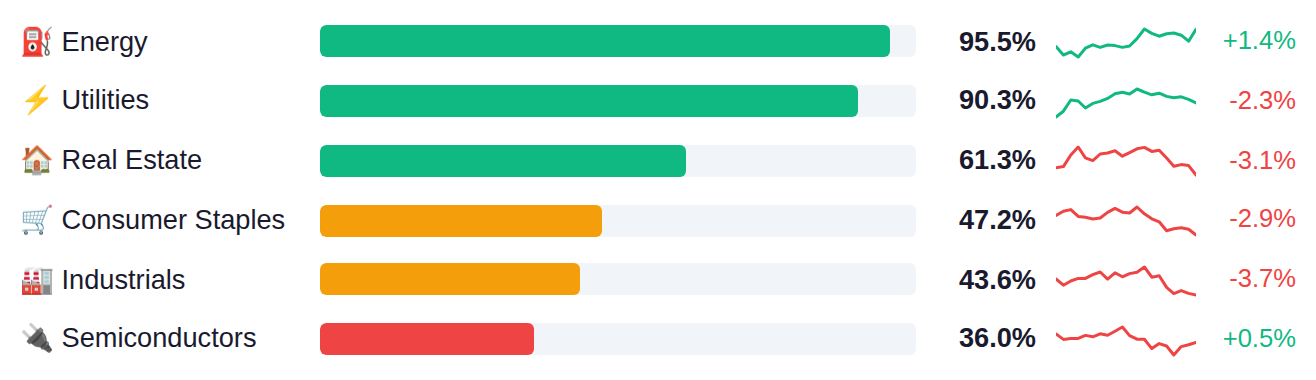

The market is showing narrow leadership with defensive sectors dominating as Energy and Utilities claim the top spots at 96% and 90% respectively, while growth-oriented areas like Consumer Discretionary and Financials languish near the bottom at 26% and 18%. This defensive rotation is occurring against a backdrop of weak index breadth, with all major indices showing participation rates around 40%, creating a notable divergence between sector strength at the top and the underlying health of the broader market. The concentration in traditionally defensive plays coupled with subdued breadth across SPY, QQQ, and DIA suggests institutions are positioning cautiously despite pockets of sector strength.

The Fed's net liquidity stood at $6.63 trillion as of March 4, up $15.1 billion week-over-week, indicating a modest expansion in system liquidity that historically correlates with supportive conditions for risk assets. The next H.4.1 release drops Thursday, March 12, which will show whether this liquidity expansion continues or reverses.

Yesterday's February CPI report came in precisely as expected across all metrics with headline inflation holding at 2.4% year-over-year and core at 2.5%, while the monthly core rate decelerated to 0.2% from 0.3%, keeping the Fed's cautious stance intact. The only notable miss came from the Monthly Budget Statement showing a $308 billion deficit versus the $170 billion estimate—a significant deterioration from January's $95 billion shortfall. This morning brought stronger-than-anticipated housing data with starts jumping 7.2% month-over-month to 1.487 million units (versus 1.37 million expected), though building permits declined 5.4% against expectations for just a 1.5% drop, suggesting potential softening ahead, while initial jobless claims came in at 213,000, better than the 217,000 forecast and indicating continued labor market resilience. Market attention now shifts to this afternoon's Producer Price Index—expected to show 0.2% monthly growth after February's flat reading—and tomorrow's critical Q4 GDP final revision (estimated at 1.4% versus the prior 4.4% in Q3, marking a sharp growth deceleration) alongside January's PCE Price Index readings, the Fed's preferred inflation gauge where core PCE is expected to tick down to 0.3% monthly from 0.4%.

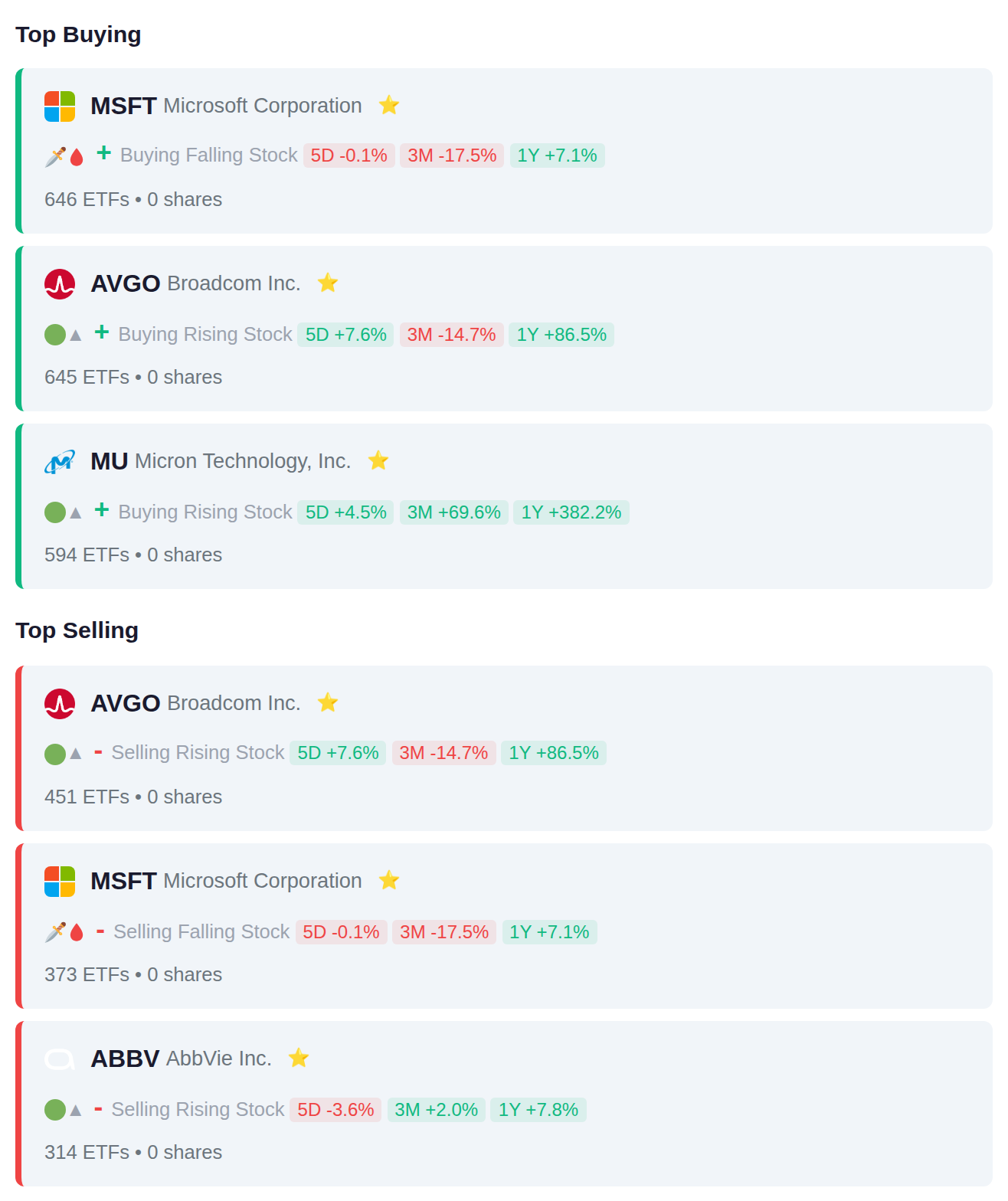

# Institutional Flow Summary Institutional money managers executed a notable rotation within technology during the recent period, with 646 ETFs adding Microsoft positions and 594 increasing Micron holdings, while simultaneously 451 ETFs reduced Broadcom exposure. The split action on mega-cap tech—particularly the 646 adds versus 373 removes in MSFT and the divergent flows in AVGO—suggests institutions rebalanced within the semiconductor and software sectors rather than abandoning technology altogether, with healthcare's AbbVie seeing net liquidation by 314 ETFs.

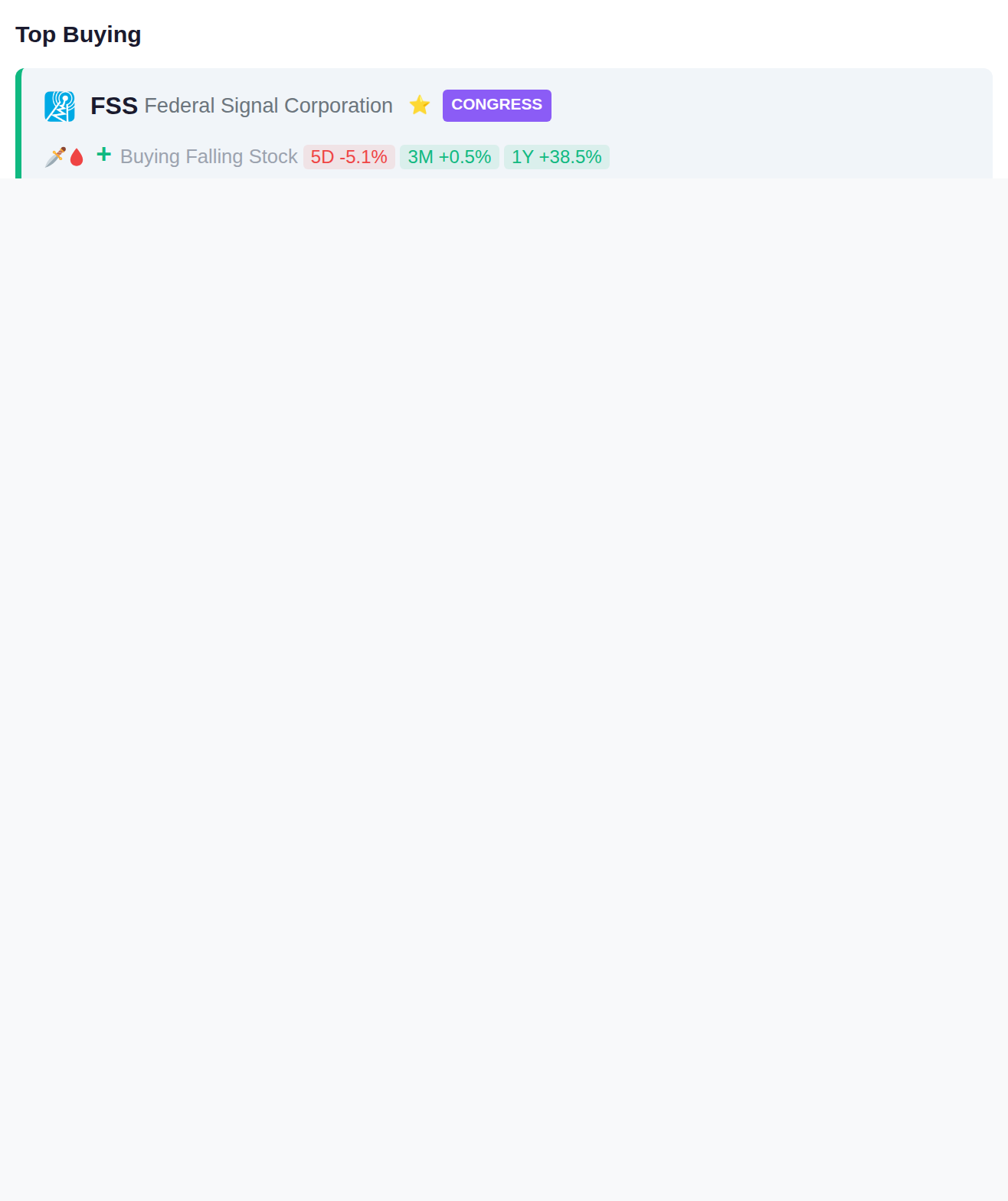

Rep. April Delaney made multiple purchases in the financial sector, acquiring positions in both FSS and NDAQ, while Rep. Gilbert Cisneros also purchased FSS. On the sell side, Rep. Pete Sessions reduced their position in telecommunications company VZ, and Rep. Kelly Louise Morrison executed two separate sales of insurance broker AJG.

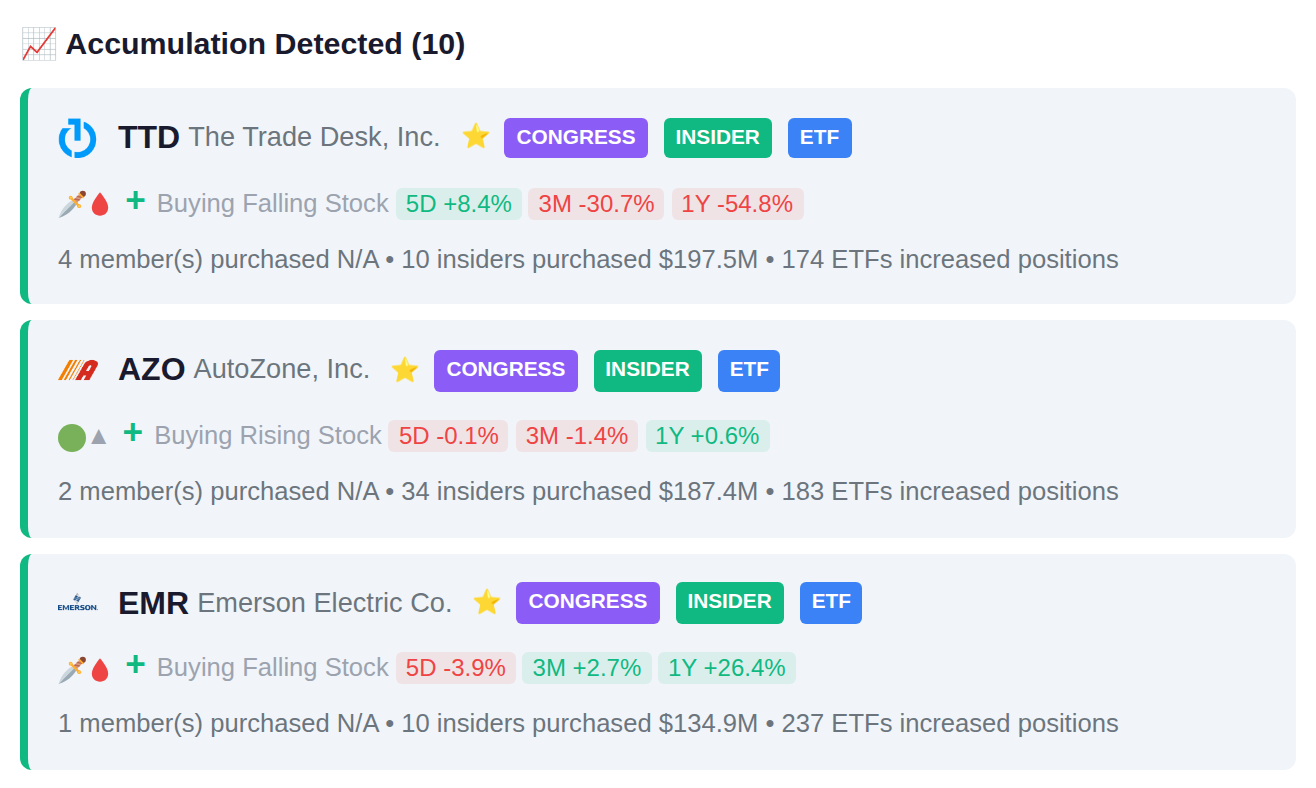

Notable cluster activity this week shows 24 insiders at GD adding positions alongside 11 at KO and 9 at TTD through purchases and awards. On the distribution side, 14 insiders at WMT reduced holdings totaling $706.3M, while concentrated selling occurred at NRG with 4 insiders offloading $5.3B and 5 insiders at BTSG selling $1.6B in positions.

587 companies report earnings today, with accumulation signals detected in INKP.JK and 034730.KS ahead of their releases, indicating recent institutional positioning. Distribution patterns have emerged in GOTO.JK and ARTO.JK, suggesting smart money has reduced exposure prior to their reports. Yesterday's session saw significant moves in 6223.TWO, SCR.TO, and 3653.TW, all advancing over 20%.