The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

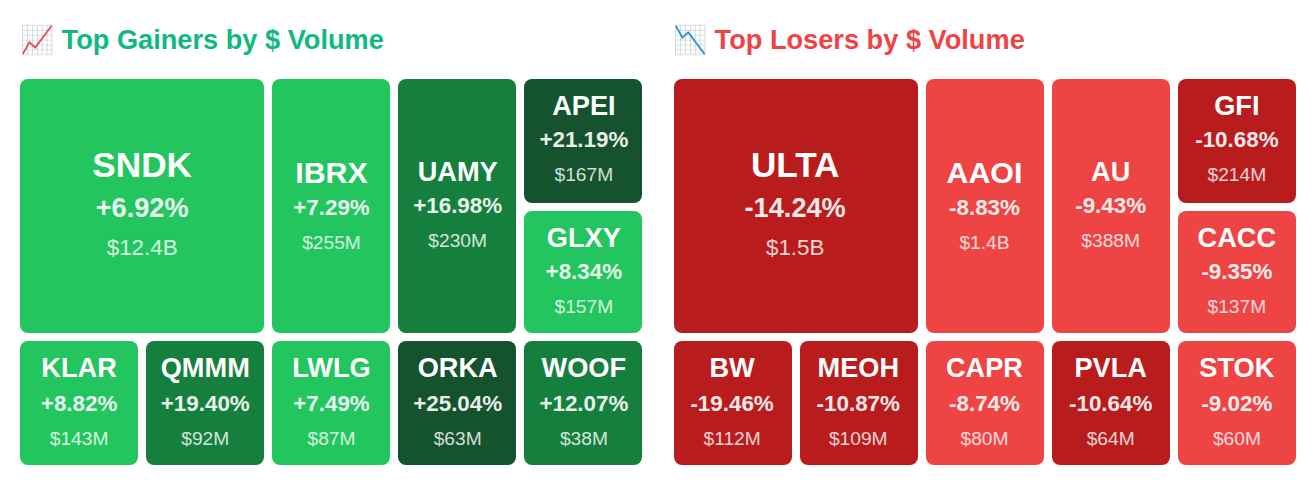

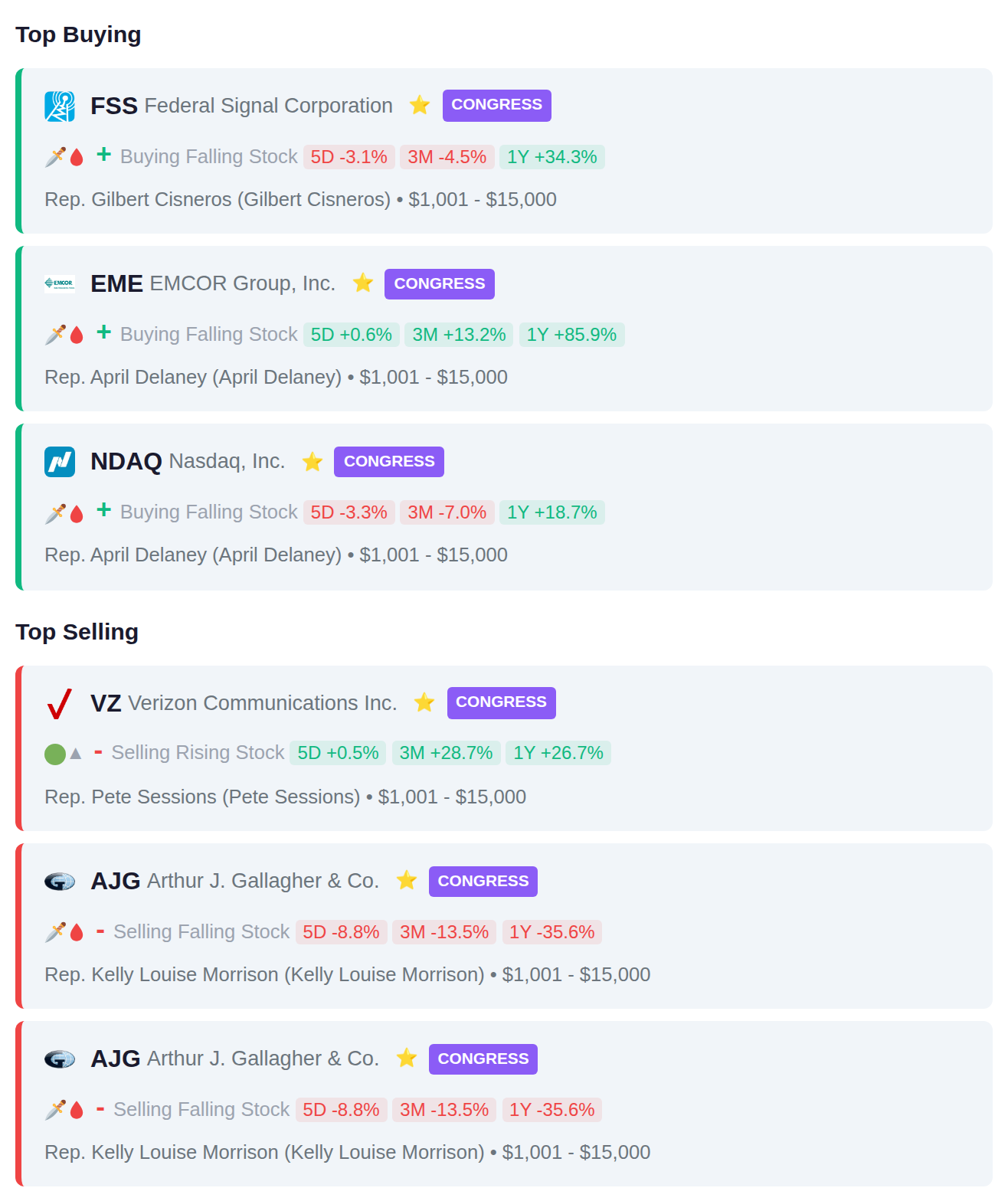

While Rep. Gilbert Cisneros (D-CA) quietly scooped up Federal Signal Corporation (FSS) shares worth up to $15,000, four insiders at NRG Energy (NRG) stampeded for the exits with $5.3 billion in sales—and that's before we get to the Klarna (KLRN) chairman throwing $50 million at his own bleeding stock or the curious case of ImmunityBio (IBRX) popping 7.3% on BCG shortage hopes despite lawyers circling Galaxy Digital Holdings (GLXY) like vultures. The VIX screamed 14.9% higher to 27.3 while smart money logged a staggering $2.4 trillion net inflow, suggesting someone knows something the rest of us are still squinting at. Here's what smart money is doing today.

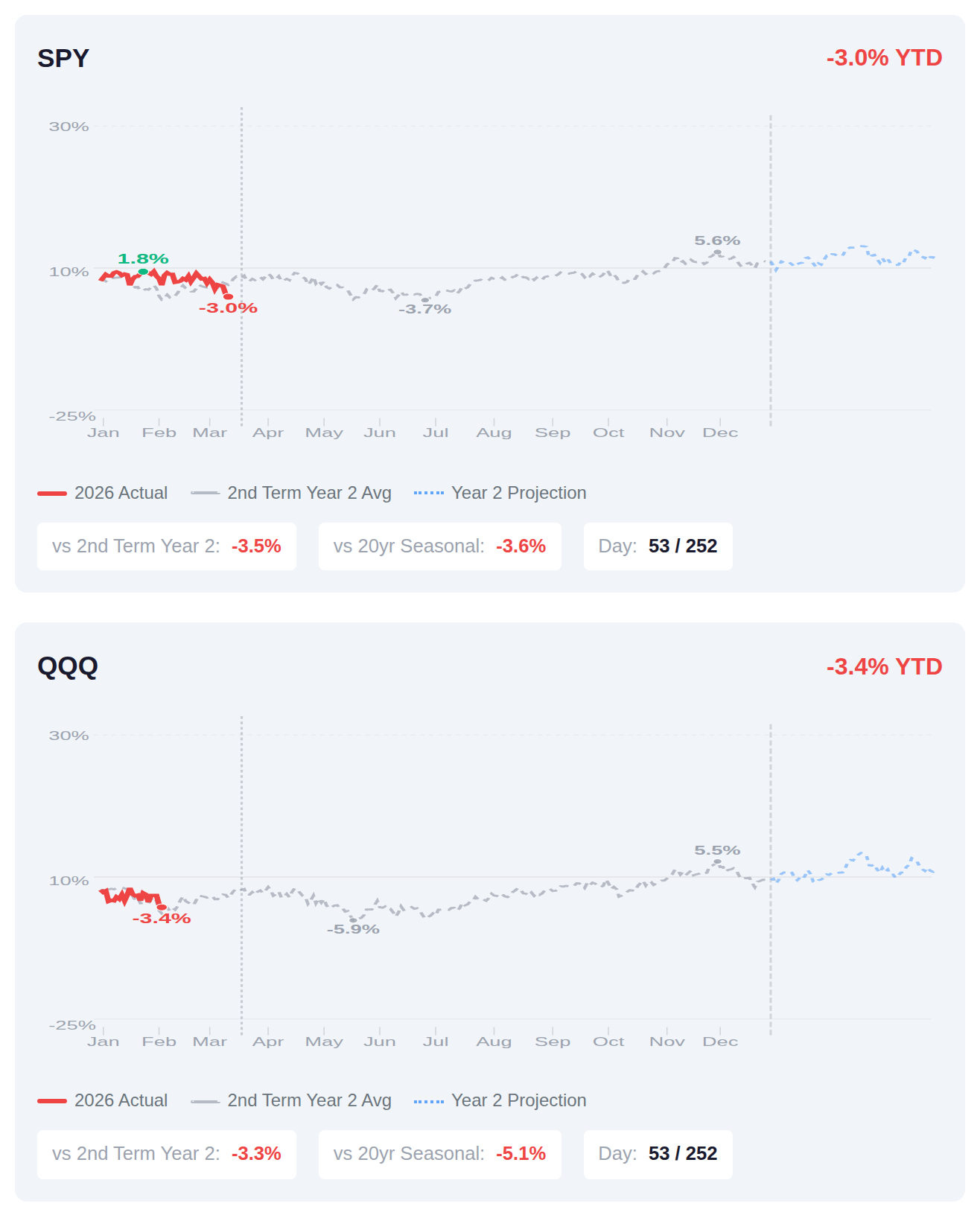

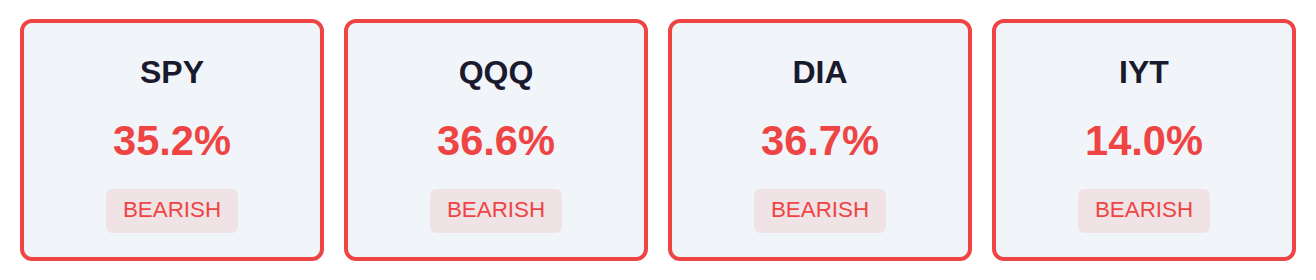

We're 53 trading days into Year 2 of Trump's second term, and both SPY and QQQ are running about 3.5% behind the typical second-term midpoint year pattern, with SPY down 3.0% versus a historical average gain of around 3.5% for full Year 2 periods. The gap is particularly notable since we're already through a fifth of the trading year, and historical data suggests Year 2 Q1 typically adds another 1.5% by mid-March—a pattern we're clearly not tracking at the moment. If the historical playbook holds from here, we'd need a significant reversal to catch up to the typical second-term Year 2 trajectory, though it's worth noting these seasonal patterns describe averages across very different market environments.

📚 Jargon Buster

Dovish

Fed talking like your chill uncle who just wants everyone to have a good time. Means lower rates and risk-on party.

Equity market volatility spiked into high-fear territory this week, with the VIX climbing 14.9% to 27.29, signaling heightened uncertainty among stock traders using options to hedge positions. In contrast, bond market volatility remained subdued, as the MOVE index edged down 1.9% to 13.24, suggesting fixed income markets are experiencing relative calm despite equity turbulence. This divergence between equity and bond volatility indicates fear is concentrated primarily in stock markets rather than reflecting broader systemic concerns across asset classes.

|| Market Sutra ||

"Trends grow quiet before they grow loud."

— Semiconductors rotated quietly in 2016 before exploding into a multi-year boom

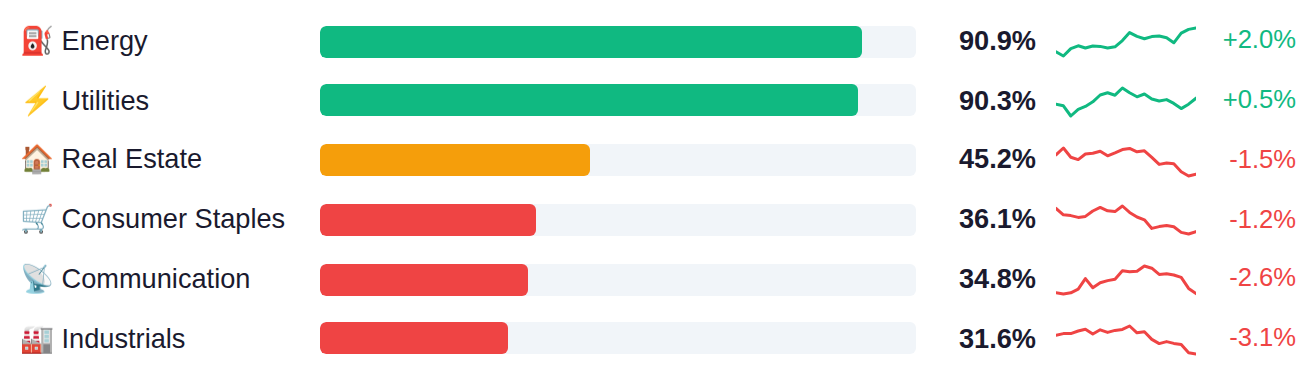

Market breadth remains narrow, with only about one-third of constituents participating in the recent advance across major indices, while the transport sector shows particularly weak internals at just 14%. A notable defensive rotation has emerged, as Energy and Utilities lead with over 90% of stocks in uptrends, while growth-oriented areas including Semiconductors and Consumer Discretionary lag significantly with less than 25% participation. This bifurcation between defensive sector strength and weakness in economically-sensitive areas reflects increased caution among market participants.

As of March 11, Fed net liquidity stood at $6.65 trillion, down $17.4 billion week-over-week, indicating a modest tightening in financial system liquidity that historically correlates with reduced market support. The next H.4.1 Federal Reserve balance sheet release drops Thursday, March 19, which will show whether this liquidity drain continued or reversed.

Yesterday's headline GDP figure of 0.7% for Q4 dramatically undershot the 1.4% estimate and marked a sharp deceleration from Q4's prior 4.4% reading, though this was partly offset by the Federal Reserve's preferred inflation gauge—Core PCE—holding steady at 0.4% month-over-month while the annual PCE Price Index improved to 2.8% from 2.9%, slightly better than the 2.9% consensus. The surprise uptick in JOLTs job openings to 6.946 million versus 6.7 million expected, combined with Personal Spending beating at 0.4% versus 0.3% estimated, signals continued consumer resilience despite weaker income growth (0.4% actual versus 0.5% forecast), while durable goods orders came in flat against a 1.2% expected gain. Today's focus shifts to the NY Empire State Manufacturing Index (estimated at 3.2 versus prior 7.1) and Industrial Production (estimated 0.1% versus prior 0.7%) as traders gauge whether the manufacturing sector is extending its recent weakness, while tomorrow's Pending Home Sales data (estimated -0.5% versus prior -0.8%) will test whether housing demand is stabilizing amid elevated mortgage rates.

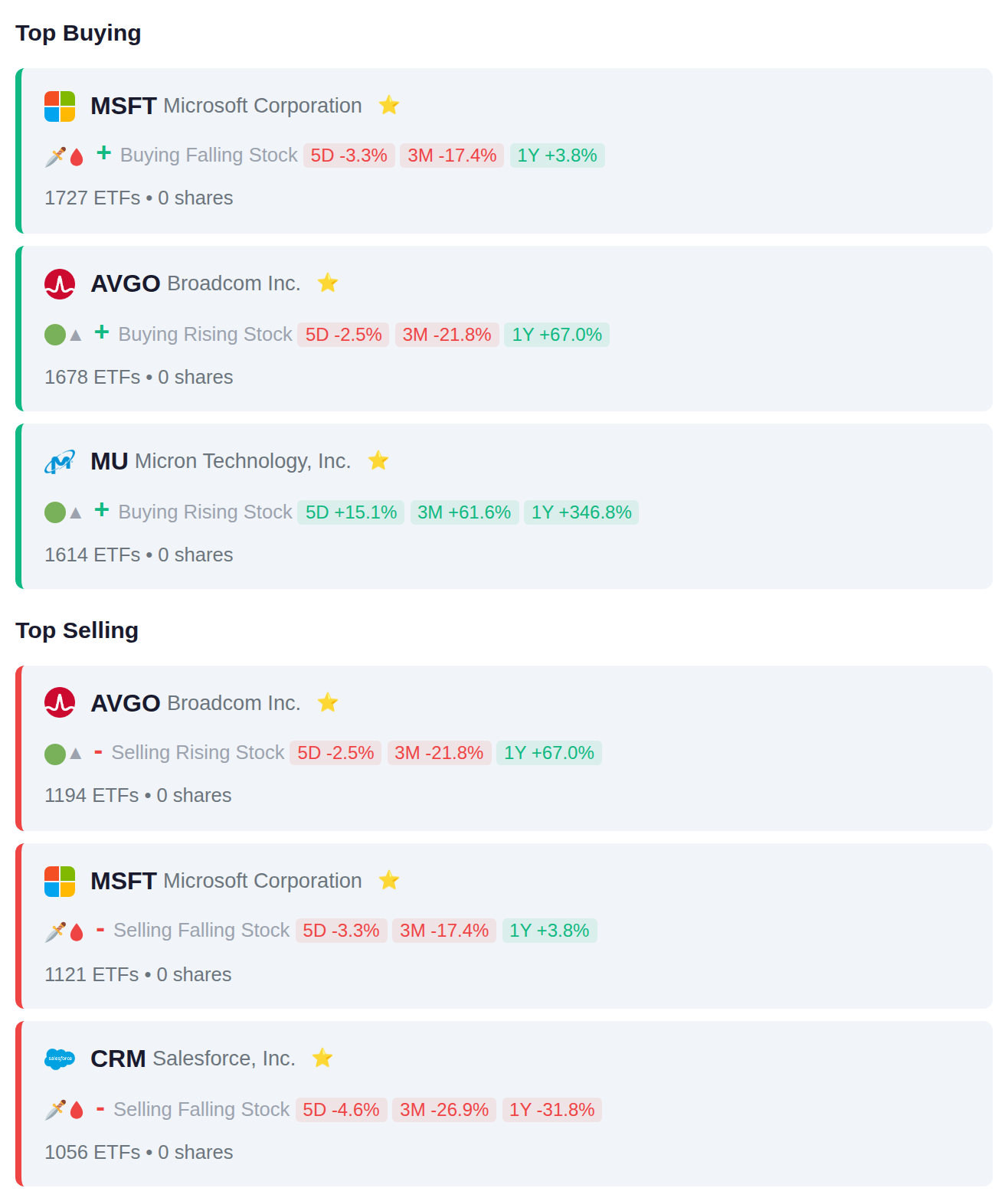

Institutional flows this period showed balanced but opposing activity across mega-cap technology, with 1,727 ETFs adding Microsoft positions while 1,121 reduced them, and similar two-way action in Broadcom (1,678 adding, 1,194 removing). The concentration in semiconductors and enterprise software—including Micron's 1,614 ETF additions and Salesforce's 1,056 reductions—suggests rotation within technology rather than sector-wide accumulation or distribution.

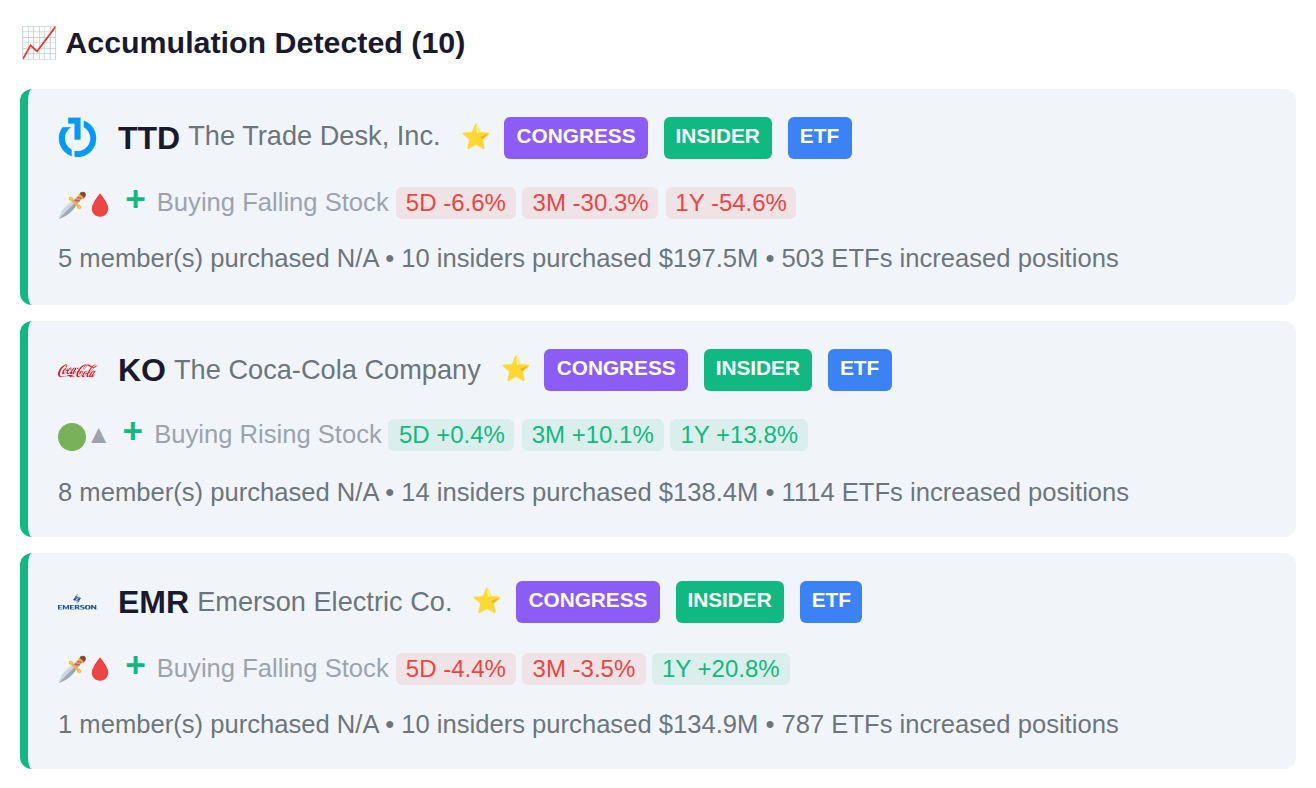

Rep. April Delaney made two purchases in the financial services sector, acquiring shares of both EME and NDAQ, while Rep. Gilbert Cisneros also added a position in FSS. On the sell side, Rep. Pete Sessions reduced holdings in telecom giant VZ, and Rep. Kelly Louise Morrison executed two separate sales of insurance broker AJG.

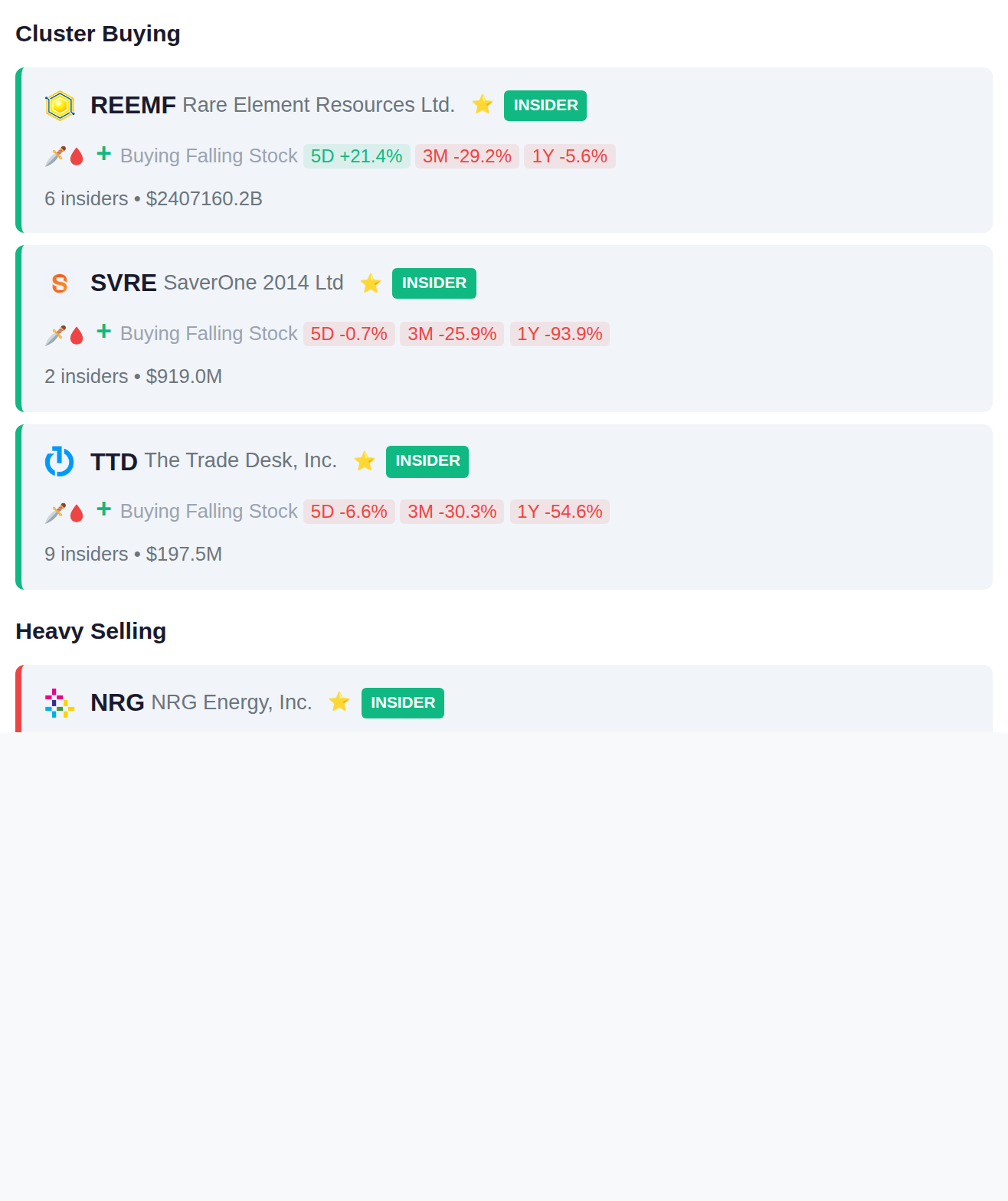

Insider activity this period showed balanced signals with 15 accumulation and 15 distribution events, though notable clustering occurred at TTD where 9 insiders received awards, REEMF with 6 insider purchases, and on the selling side NRG where 4 insiders collectively disposed of $5.3 billion in holdings. Additional coordinated selling activity was observed at MDLN with 5 insiders distributing $2.2 billion and BTSG where 5 insiders reduced positions totaling $1.6 billion.

Today's earnings calendar features 329 companies reporting results, with accumulation signals present in INCO.JK and INKP.JK, while BRPT.JK and SAME.JK show distribution patterns ahead of their reports. Yesterday's session saw significant movement in GLVHF, which gained 49.4%, alongside notable advances in 7712.TWO and SDF.DE. Tomorrow's calendar includes 161 companies scheduled to report quarterly results.