The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

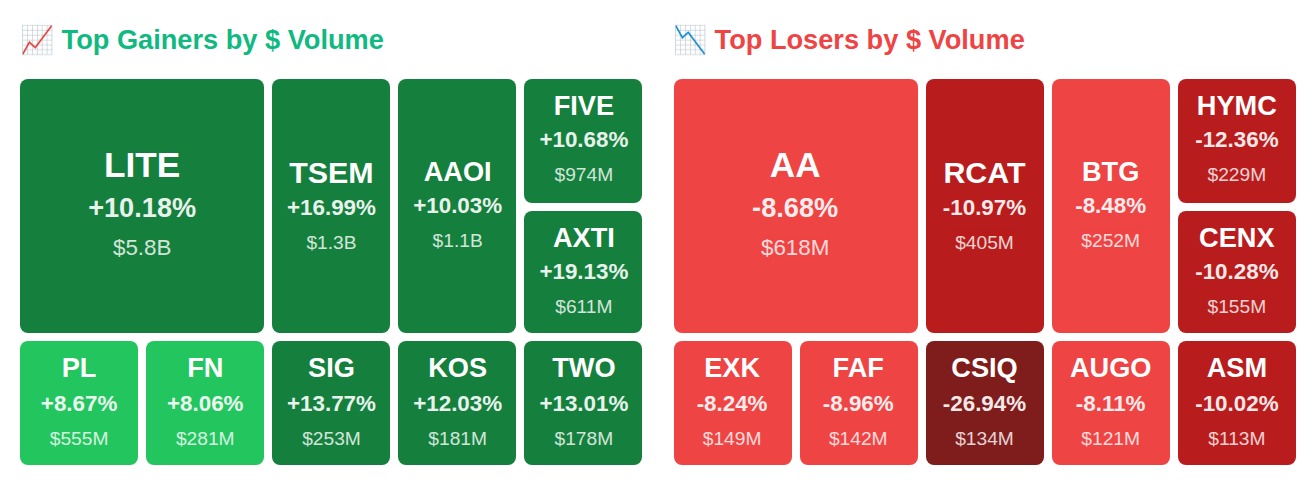

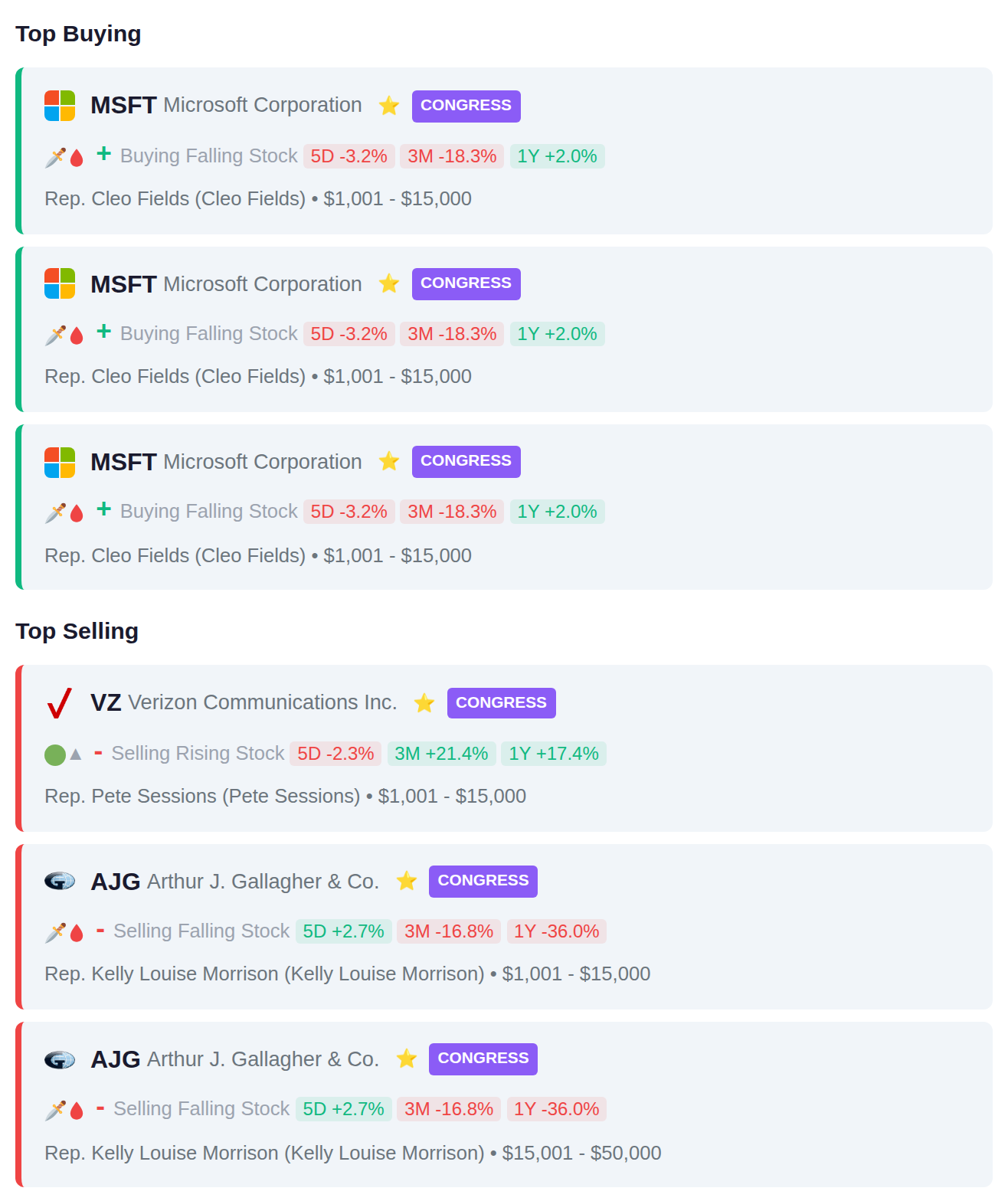

Rep. Cleo Fields purchased Microsoft (MSFT) stock worth up to $15,000 while insiders at Modelon (MDLN) dumped $2.2 billion—and that's just the warm-up before Lumentum Holdings (LITE) ripped 10.2% to $772 after hours on Nvidia halo effect, Tower Semiconductor (TSEM) exploded 17% to $166 on AI power chip news, and Applied Optoelectronics (AAOI) spiked 10% to $102 despite dilution concerns. Smart money recorded $4.6 billion in net outflows today while the VIX climbed 3.5% to 25.1 and the Fed quietly injected $9.6 billion in liquidity into the system. Here's what smart money is doing today.

📚 Jargon Buster

Hard Landing

Recession, baby. Stocks cry, jobs disappear, and the Fed says “oopsie.”

The VIX currently sits at 25.09, reflecting elevated fear in equity markets after rising 3.5% over the past week and crossing into the high volatility threshold above 25. Meanwhile, the MOVE index measuring bond market volatility remains subdued at 14.54 despite an 11.6% weekly increase, suggesting fixed income markets are experiencing relatively calm conditions. This divergence indicates stock investors are pricing in considerably more uncertainty than their bond market counterparts, an unusual dynamic that typically reflects equity-specific concerns rather than broader systemic stress.

|| Market Sutra ||

"The first mistake hurts; the second destroys."

— Averaging down ARKK names in 2021–2022 led to irreversible drawdowns

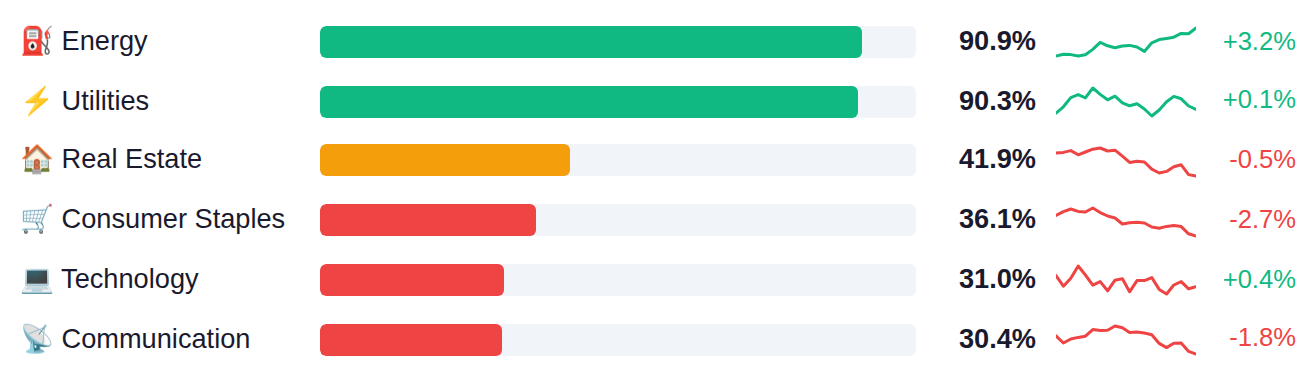

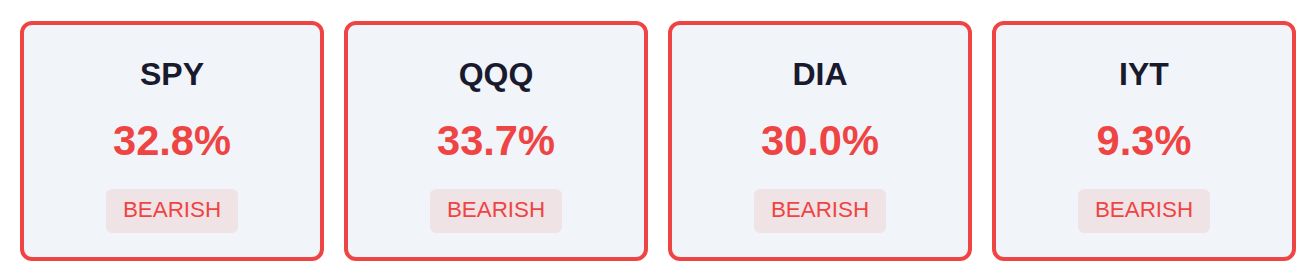

Market breadth remains narrow across major indices, with roughly one-third of SPY and QQQ components trading above their moving averages while IYT shows particularly weak participation at just 9%. Defensive sectors like Energy and Utilities are demonstrating relative strength above 90%, contrasting sharply with growth-oriented areas including Consumer Discretionary and Semiconductors languishing near 21% and Financials at just 12%. This divergence between defensive leadership and weakness in cyclical sectors suggests investors are currently rotating toward traditionally lower-volatility areas of the market.

As of March 18, Fed net liquidity stood at $6.66 trillion, up $9.6 billion from the previous week, indicating a modest expansion in system-wide liquidity conditions that historically correlates with supportive environments for risk assets. The next H.4.1 release drops Thursday, March 26, which will show whether this liquidity expansion continued or reversed course.

Yesterday's data painted a mixed picture as the labor market showed unexpected resilience with initial jobless claims falling to 205K versus the 215K estimate, while January new home sales collapsed to 587K from a revised 712K prior month, missing estimates by 133K units—the weakest reading since August 2024. The Philadelphia Fed Manufacturing Index surged to 18.1, crushing the 10.0 estimate by 8.1 points and marking the strongest expansion in the region since October 2024, even as the Atlanta Fed trimmed its Q1 GDP tracking from 2.7% to 2.3%. Today's CFTC positioning data will reveal whether speculators maintained their net short stance on S&P 500 futures (last at -134.5K contracts) amid this resilient economic backdrop, while traders tomorrow will watch for any further revision to the Atlanta Fed's GDP nowcast and whether the Chicago Fed's National Activity Index confirms the persistent economic momentum that's kept recession fears at bay.

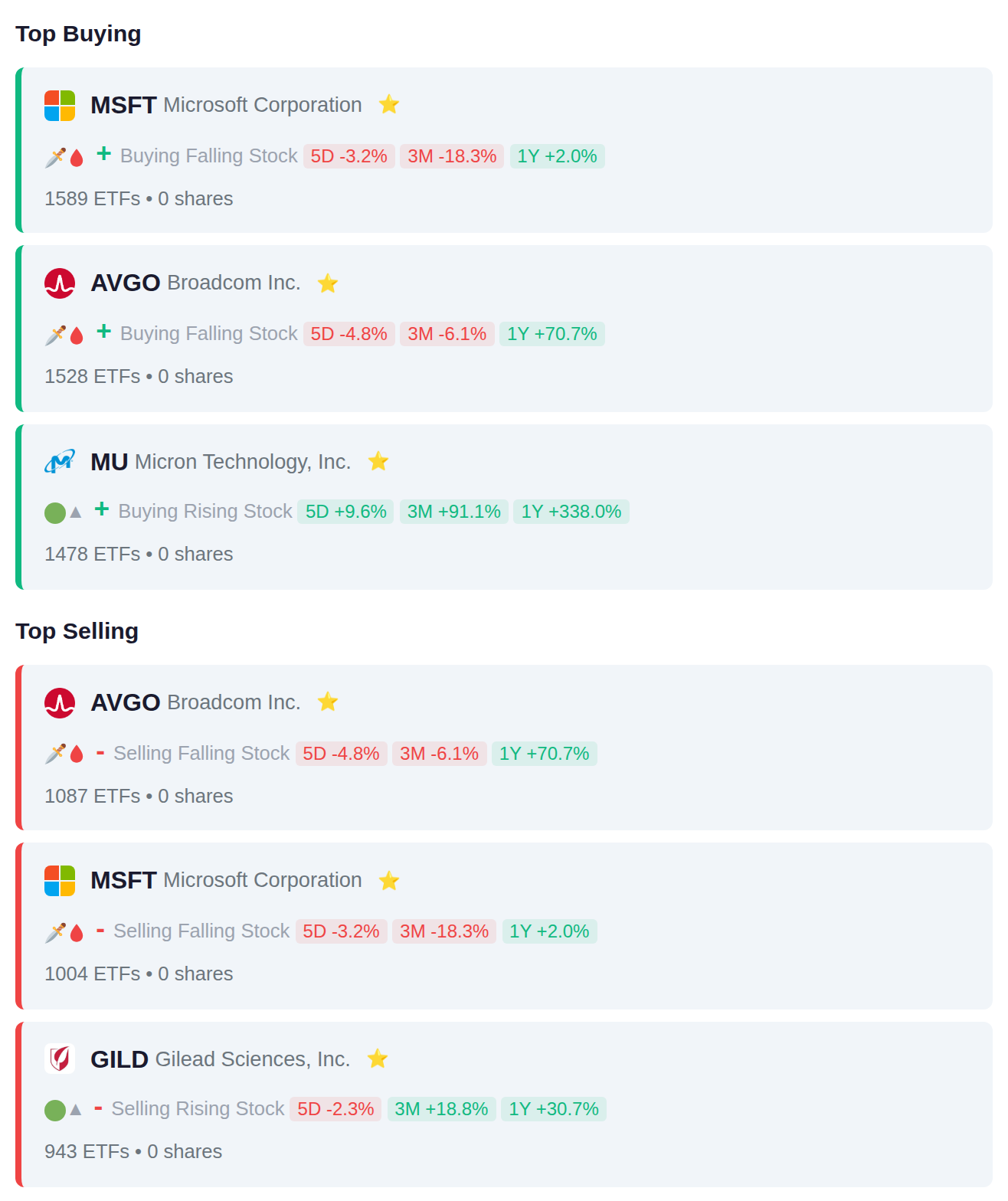

Exchange-traded funds displayed mixed positioning in technology during the period, with 1,589 ETFs adding Microsoft and 1,478 adding Micron in the semiconductor space, while 1,087 ETFs simultaneously reduced Broadcom holdings despite it also appearing among top additions. The institutional flow suggests selective rotation within technology sectors, as funds rebalanced between software, chip manufacturers, and diversified semiconductor positions, while healthcare also saw notable distribution with 943 ETFs reducing Gilead Sciences.

Rep. Cleo Fields made three separate purchases of Microsoft (MSFT) shares, while Rep. Pete Sessions sold Verizon (VZ) and Rep. Kelly Louise Morrison executed two sales of Arthur J. Gallagher & Co. (AJG). The activity shows concentrated buying interest in big tech and multiple exits from both telecommunications and insurance brokerage positions.

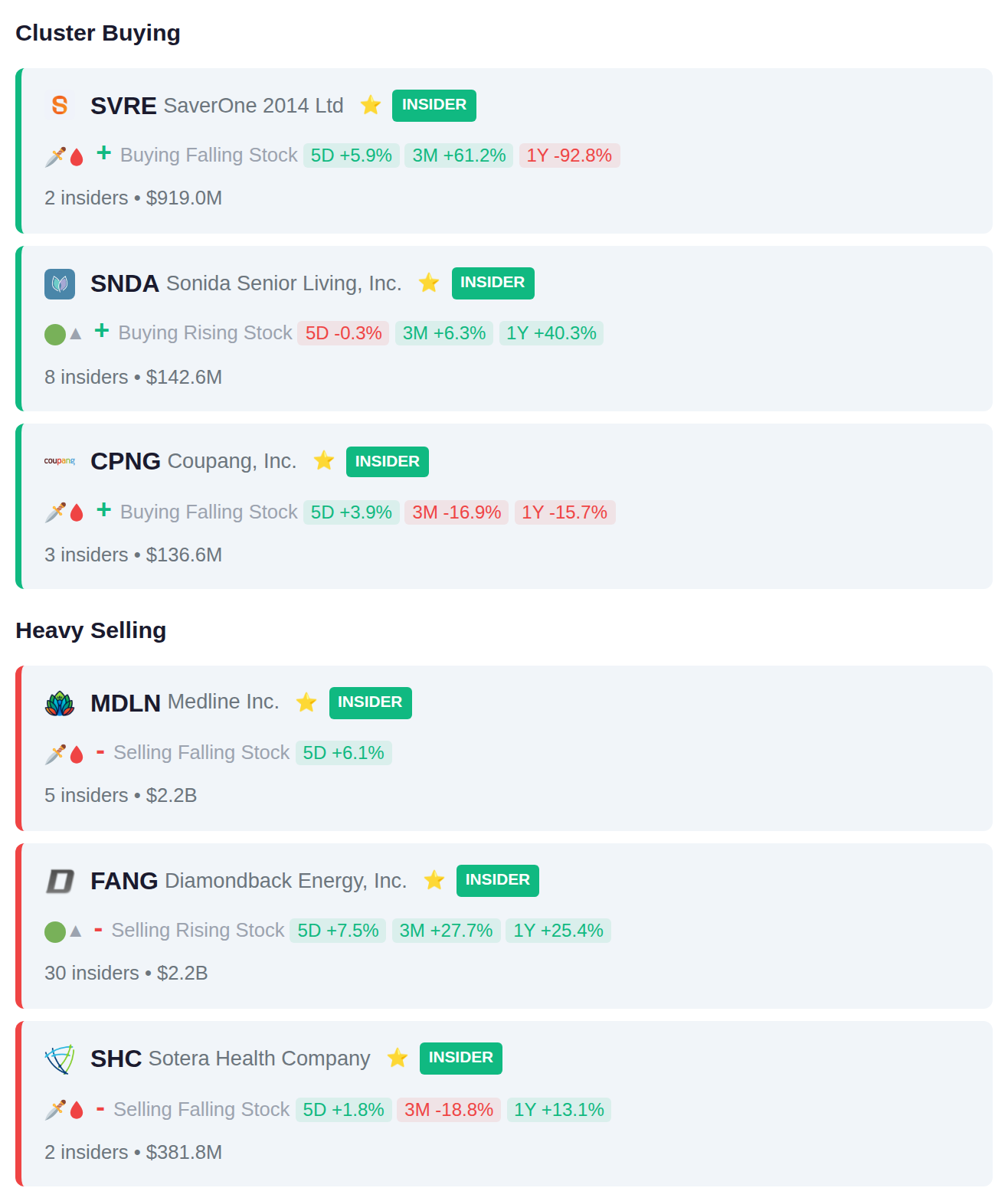

Multiple insiders at SNDA accumulated shares with 8 separate purchases, while FANG saw the largest cluster of selling activity with 30 insiders collectively disposing of $2.2 billion in holdings. MDLN also experienced significant distribution as 5 insiders sold a combined $2.2 billion, representing notable coordinated activity on both sides of the ledger.

185 companies report earnings today, with VAPORES.SN and AKRN.ME showing recent institutional accumulation patterns heading into their results. TLKM.JK and SMRA.JK are experiencing distribution activity among large holders ahead of their reports. Yesterday's session saw notable declines in OLA.TO and ORLA, both down more than 21%, alongside an 18.4% drop in ALM.