The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

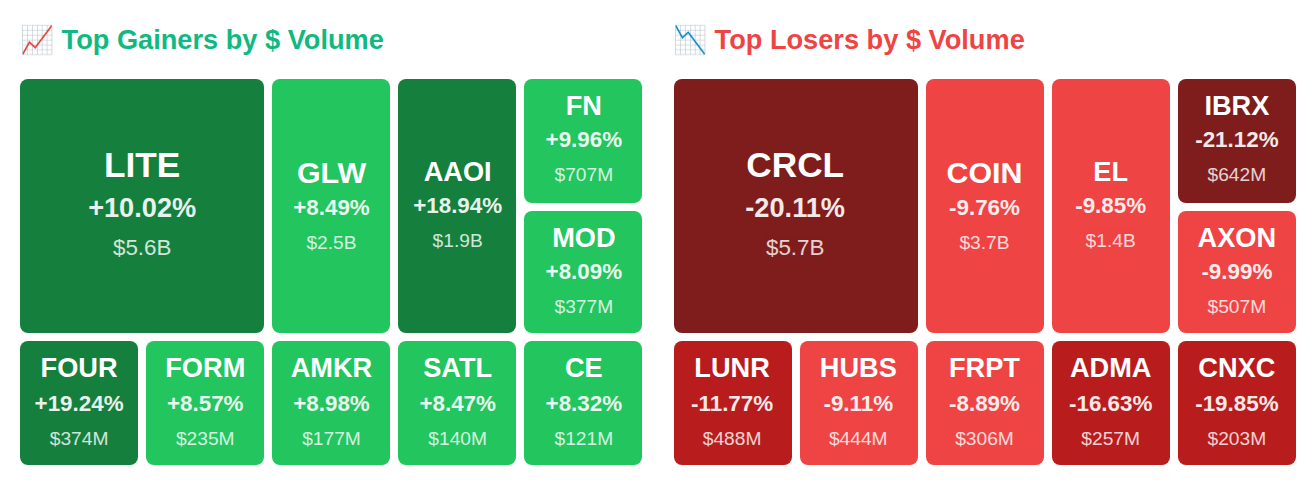

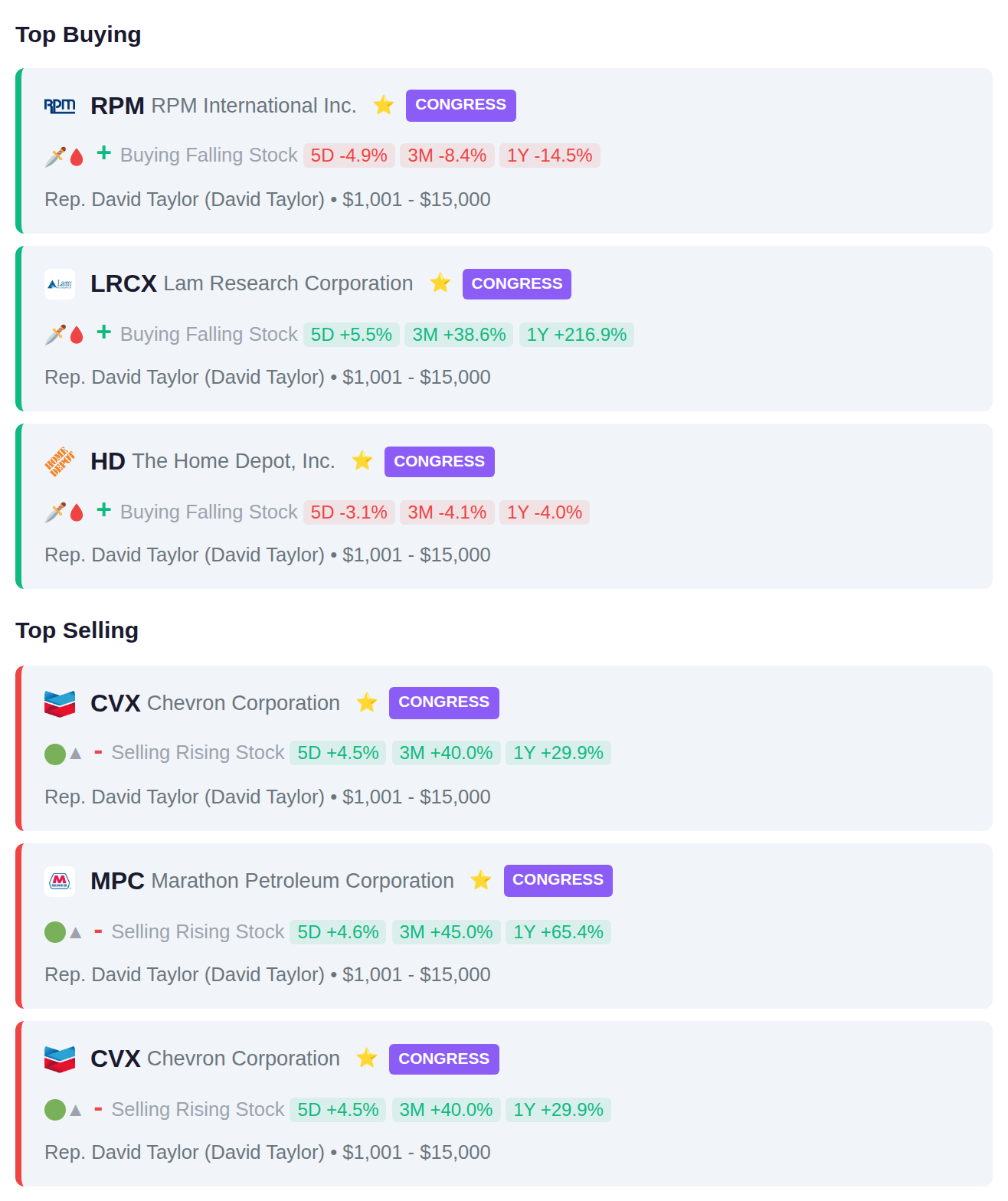

While the VIX spiked 11.2% to 26.1 and insiders at Wheeler Real Estate Investment Trust (WHLR) dumped $31.4 billion in stock, Rep. David Taylor quietly added RPM International Inc. (RPM) shares worth up to $15,000—and after hours, Applied Optoelectronics Inc. (AAOI) rocketed 19% to $114 on hyperscale data center orders while BNP analysts called for Lumentum Holdings Inc. (LMTR) to hit $1,000 (up 1,100% in a year). The smart money flow today showed a staggering $31.4 trillion net outflow, but certain corners of the AI and data center universe saw cash flooding in like it's 1999 all over again. Here's what smart money is doing today.

📚 Jargon Buster

Core PCE

Jerome’s favorite inflation number. Strips out food and energy because apparently nobody eats or drives.

Market volatility indicators are presenting a mixed picture, with the VIX equity fear gauge climbing 11.2% week-over-week to 26.15, placing it in high fear territory typically associated with heightened uncertainty in stock markets. In contrast, the MOVE index measuring bond market volatility declined 8.0% to 13.65, indicating relatively calm conditions in fixed income markets. This divergence suggests investors are pricing in considerably more risk and potential price swings in equities compared to bonds, a dynamic that often emerges when equity-specific concerns outweigh broader systemic or interest rate anxieties.

|| Market Sutra ||

"The best trades are obvious only in hindsight."

— Buying Nvidia in 2019 looked uncertain—now it looks genius

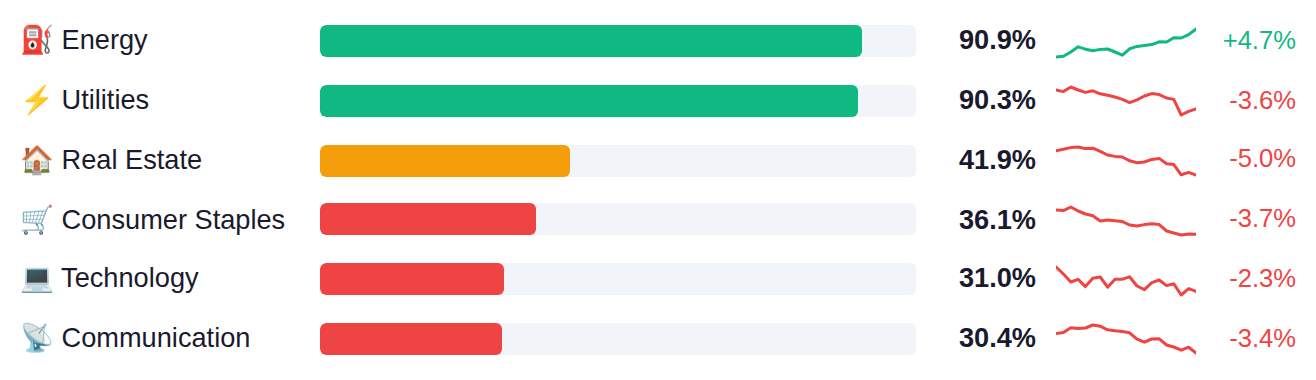

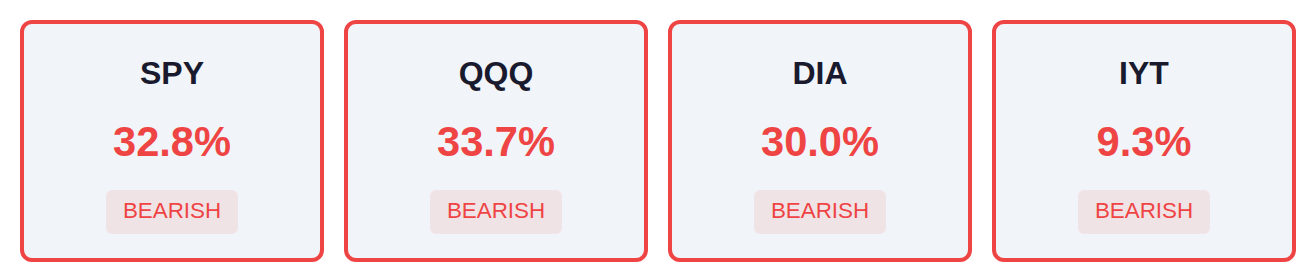

Market breadth remains constrained across major indices, with roughly one-third of SPY and QQQ components advancing while the Dow Jones and Transportation Index show similar or weaker participation. A notable divergence has emerged between defensive sectors like Energy and Utilities, which are advancing in over 90% of their constituents, and growth-oriented areas including Consumer Discretionary and Semiconductors, where fewer than one in four stocks are participating in gains. This defensive sector leadership combined with narrow overall breadth suggests investors are rotating toward traditionally stable areas of the market while avoiding more cyclical and technology-related exposures.

Fed net liquidity stood at $6.66 trillion as of March 18, up $9.6 billion from the prior week, indicating a continued expansion in system liquidity that has historically correlated with supportive market conditions. The next H.4.1 release drops Thursday, March 26, which will show whether this liquidity expansion accelerates, stabilizes, or reverses.

Yesterday's PMI data painted a mixed picture as manufacturing unexpectedly strengthened to 52.4 (versus 51.3 expected), marking its highest reading since September 2022, while services slipped to 51.1 from 51.7, though the composite index still beat estimates at 51.4 versus 50.5 expected—keeping the economy in expansion territory above 50 for the sixth consecutive month. Crude oil inventories rose 2.3 million barrels according to API data, a sharp reversal from the expected 1.3 million barrel draw, which could pressure energy prices if confirmed by today's official EIA report that estimates a more modest 0.5 million barrel build. Markets will focus on this morning's import price data (expected up 0.5% versus 0.2% prior) for fresh inflation signals, while tomorrow's initial jobless claims forecast at 210,000 versus last week's 205,000 will test whether the labor market remains as tight as recent sub-211,000 readings suggest, with three Fed speakers including Vice Chair Barr potentially addressing the inflation-employment balance ahead of the May policy meeting.

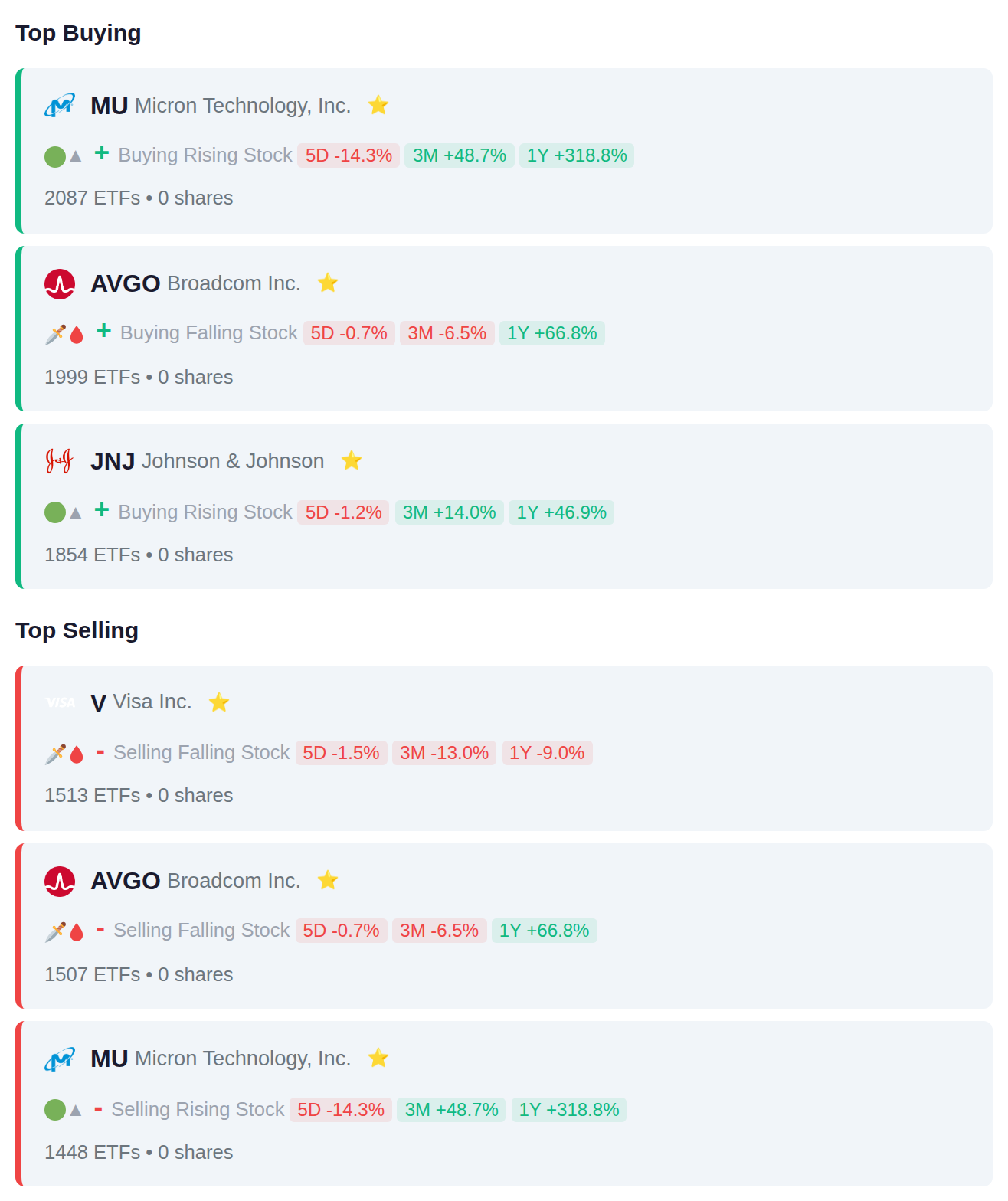

Institutional flows show mixed positioning in semiconductor names, with 2,087 ETFs adding Micron and 1,999 adding Broadcom even as 1,507 and 1,448 ETFs respectively reduced those same positions, suggesting active rebalancing within the chip sector. Defensive healthcare exposure increased as 1,854 ETFs added Johnson & Johnson, while payment processor Visa saw net reduction with 1,513 ETFs trimming positions.

Rep. David Taylor executed multiple transactions, purchasing shares of RPM International (RPM), Lam Research (LRCX), and Home Depot (HD) while divesting energy sector holdings with two separate sales of Chevron (CVX) and one sale of Marathon Petroleum (MPC). The trading pattern indicates a rotation out of oil and gas equities into positions spanning specialty chemicals, semiconductor equipment manufacturing, and home improvement retail.

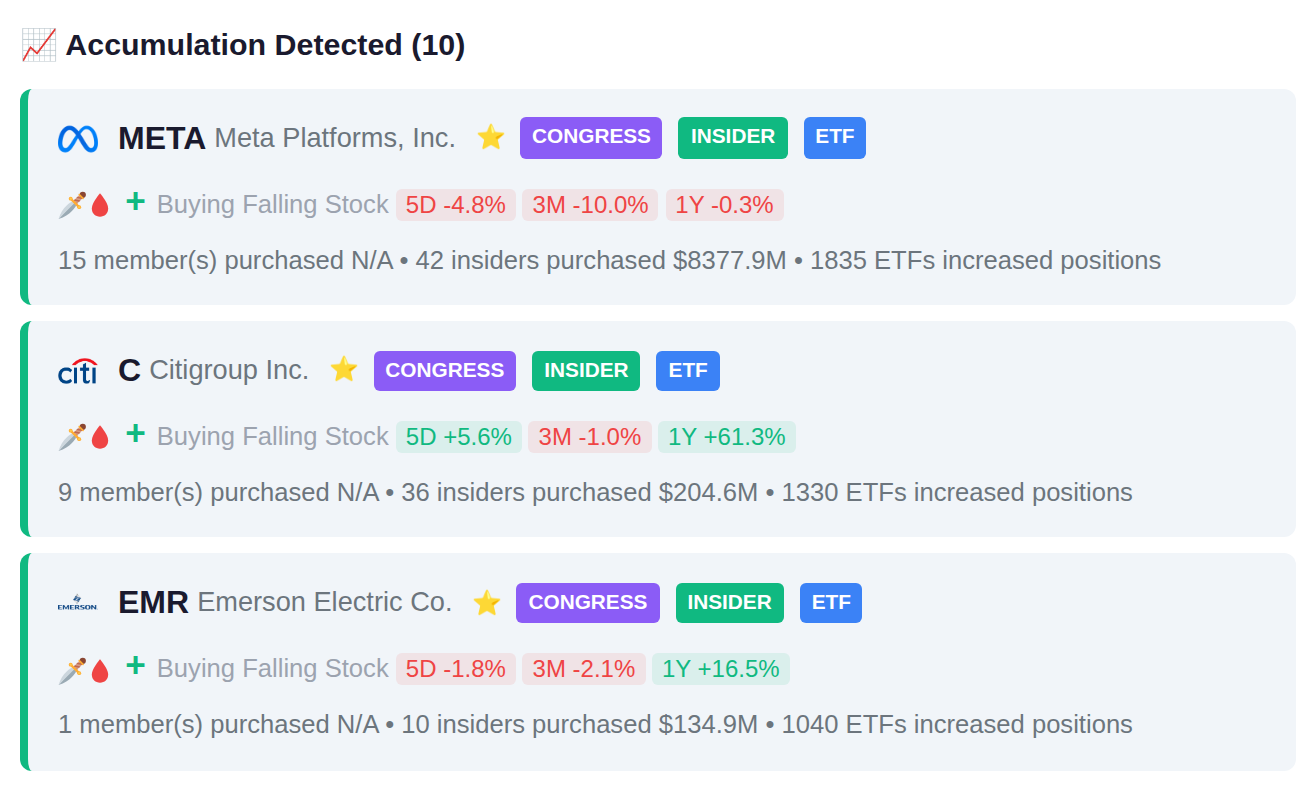

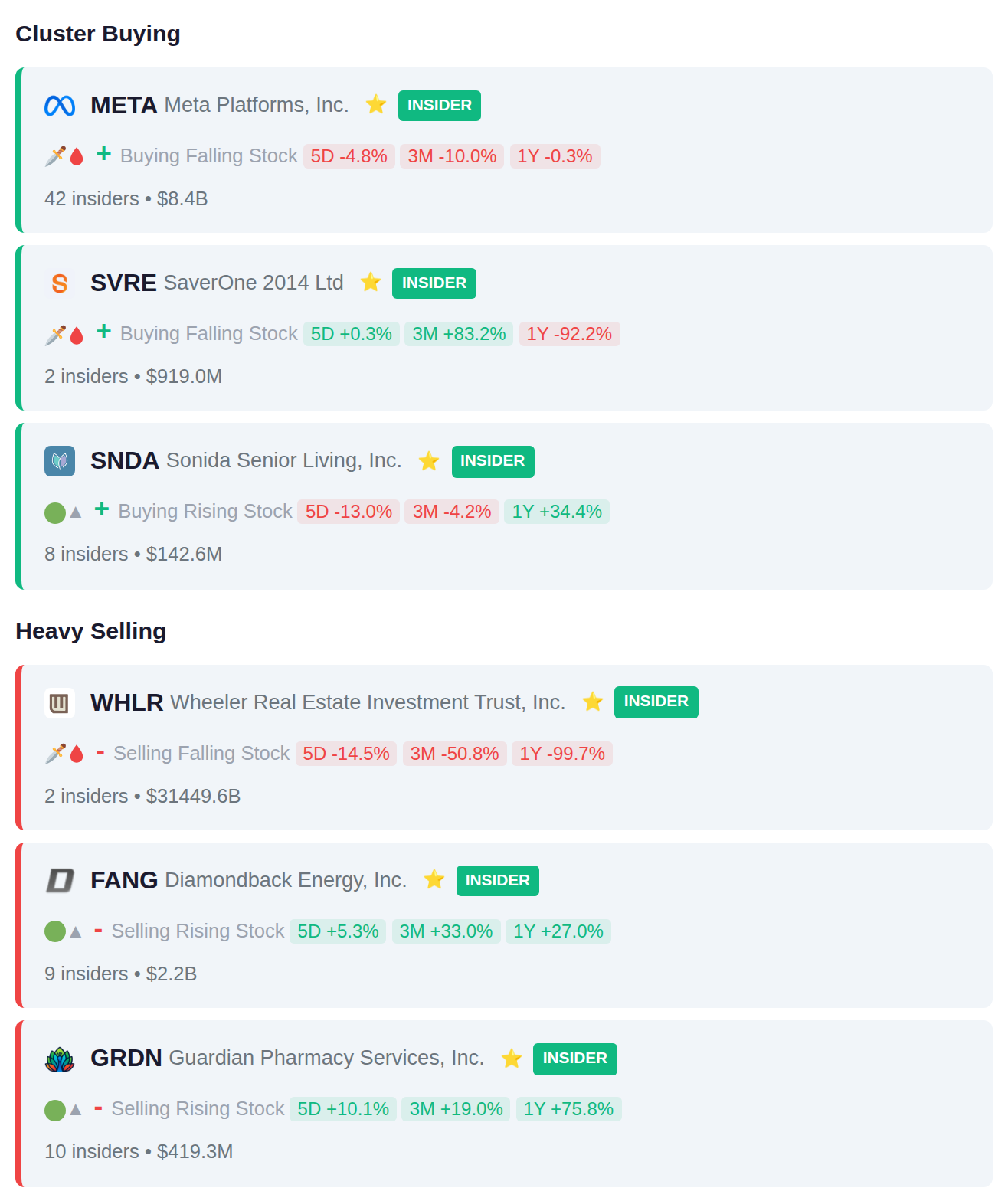

Recent insider activity shows clustered transactions at several companies, with 42 insiders at META recording purchases or awards, while 10 insiders at GRDN collectively sold $419.3M in shares. Additional coordinated activity includes 9 insiders at FANG disposing of $2.2B in holdings and 8 insiders at SNDA adding positions, resulting in balanced 15-15 accumulation versus distribution signals across tracked companies.

Today's earnings calendar features 256 companies reporting, with BNBR.JK and INDY.JK showing recent accumulation by institutional holders ahead of results, while TLKM.JK and ICBP.JK have experienced distribution activity. Yesterday saw significant declines in ELE, CNXC, and BWY.L following their reports. No companies are scheduled to report tomorrow.