The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

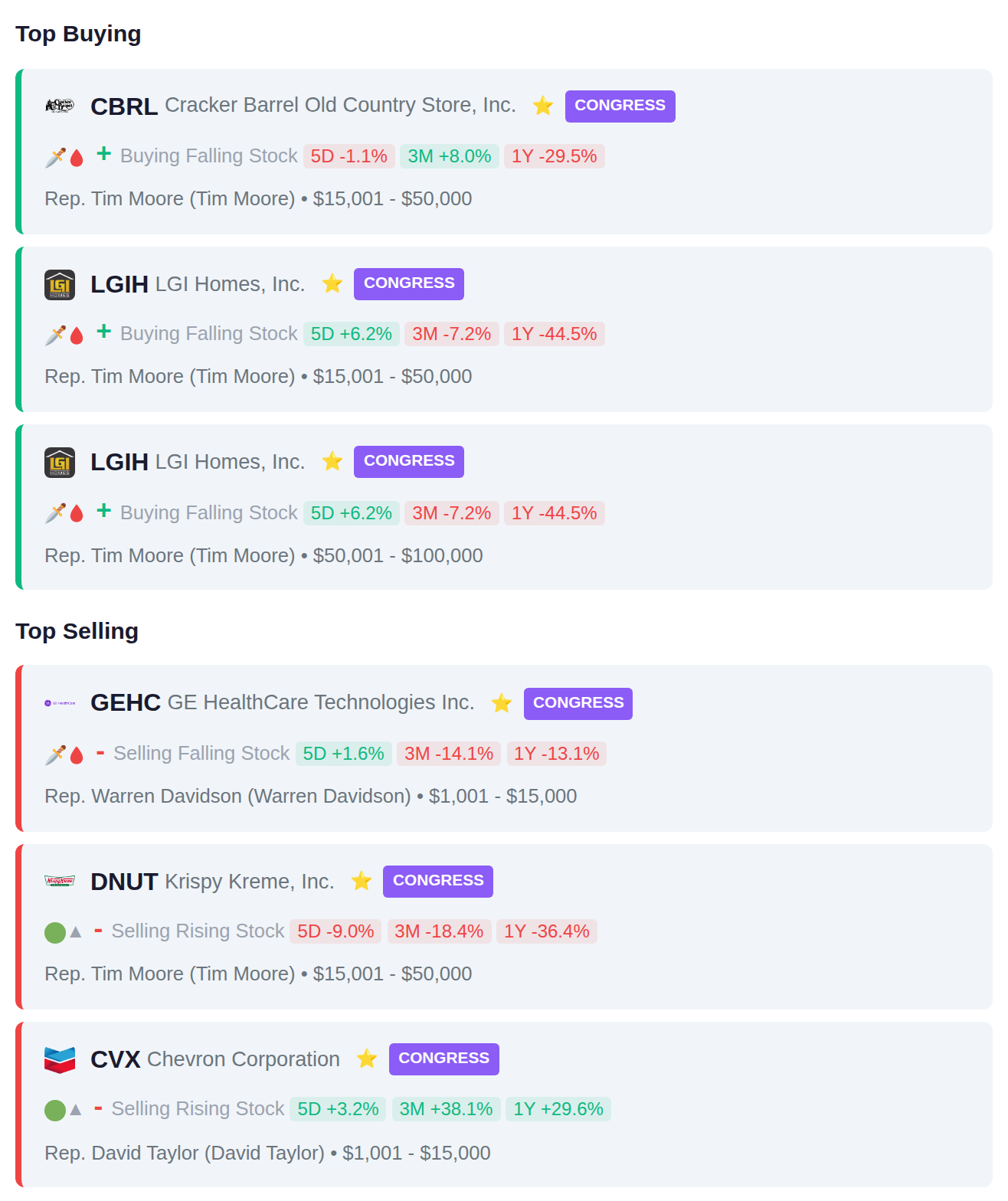

Rep. Tim Moore added Cracker Barrel Old Country Store (CBRL) while insiders at Wheeler Real Estate Investment Trust (WHLR) dumped $31.4 billion—because nothing screams confidence like a casual ten-figure exit before markets open. After hours, Brown-Forman (BF.B) popped nearly 10% on Pernod Ricard merger whispers, Regeneron Pharmaceuticals (REGN) surged 12% on biotech hype, and Kodiak Sciences (KDK) rocketed 75% after its eye drug aced trials, all while the Fed quietly pumped $1.2 billion into the system and smart money recorded a $31.4 trillion net outflow. Here's what the insiders, institutions, and politicians actually did with their money today.

📚 Jargon Buster

PPI

Wholesale inflation. What companies pay before they mark it up and blame “supply chains.”

The VIX currently sits at 25.33, indicating elevated fear in equity markets and representing a slight 1.0% increase from the prior week, while remaining in the high volatility zone above the 25 threshold. In contrast, the MOVE index measuring bond market volatility registered 14.79, up 1.7% week-over-week but remaining at historically low levels, suggesting fixed income markets are experiencing relative calm. This divergence between equity and bond volatility reflects differing stress levels across asset classes, with stock market participants pricing in considerably more uncertainty than their bond market counterparts.

|| Market Sutra ||

"Liquidity hides insolvency."

— Many zombie companies stayed alive only because of near-zero interest rates

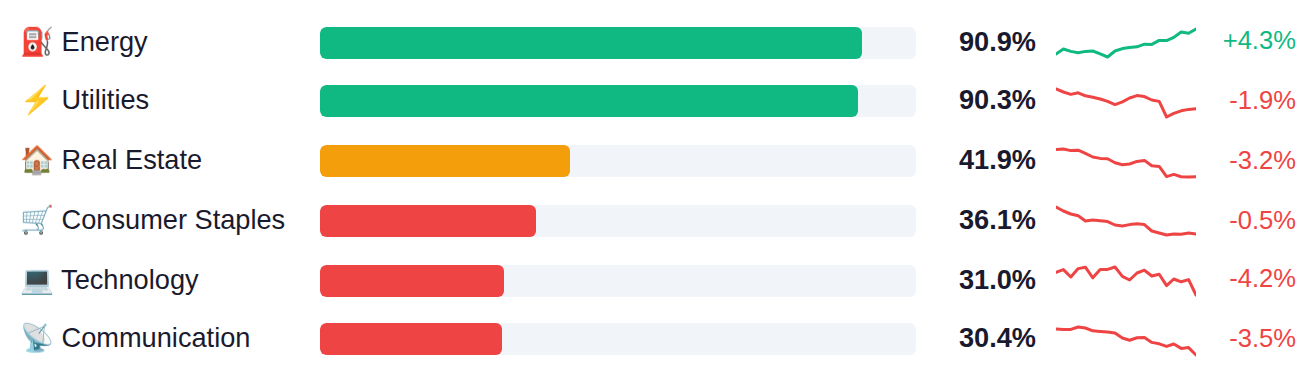

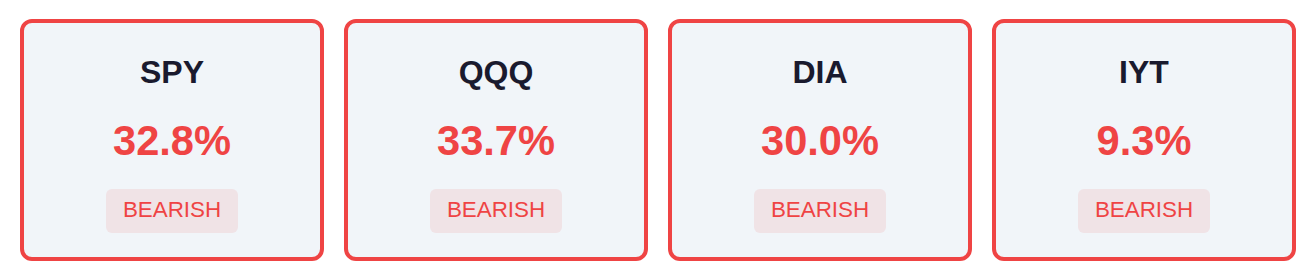

Market breadth remains weak across major indexes, with only about one-third of SPY and QQQ constituents trading above their moving averages, while transportation stocks show particular weakness at just 9%. Traditional defensive sectors are demonstrating relative strength, with Energy and Utilities showing participation rates above 90%, while growth-oriented areas like Consumer Discretionary and Semiconductors lag significantly at around 21%, suggesting investors are rotating toward more conservative positioning.

As of March 25, Fed net liquidity stands at $6.66 trillion, up $1.2 billion from the prior week, indicating a marginal increase in system-wide dollar availability that typically correlates with supportive conditions for risk assets. The next H.4.1 release drops Thursday, April 02, which will show whether this modest liquidity expansion continues or reverses.

Yesterday's jobless claims data showed continuing claims improved to 1,819K against expectations of 1,850K, marking a 31K beat that suggests labor market resilience remains intact despite the four-week average holding steady at 210.5K. Today's focus shifts to the University of Michigan Consumer Sentiment reading, expected to decline further to 54.0 from 56.6—which would mark the lowest level since June 2022 if realized—alongside inflation expectations forecast to tick down to 3.2% from 3.3%. The CFTC positioning data will also be scrutinized for shifts in speculative sentiment, particularly the S&P 500's net short position of -113.1K contracts, an unusual stance that could signal either hedging activity or outright bearish bets amid the recent market volatility.

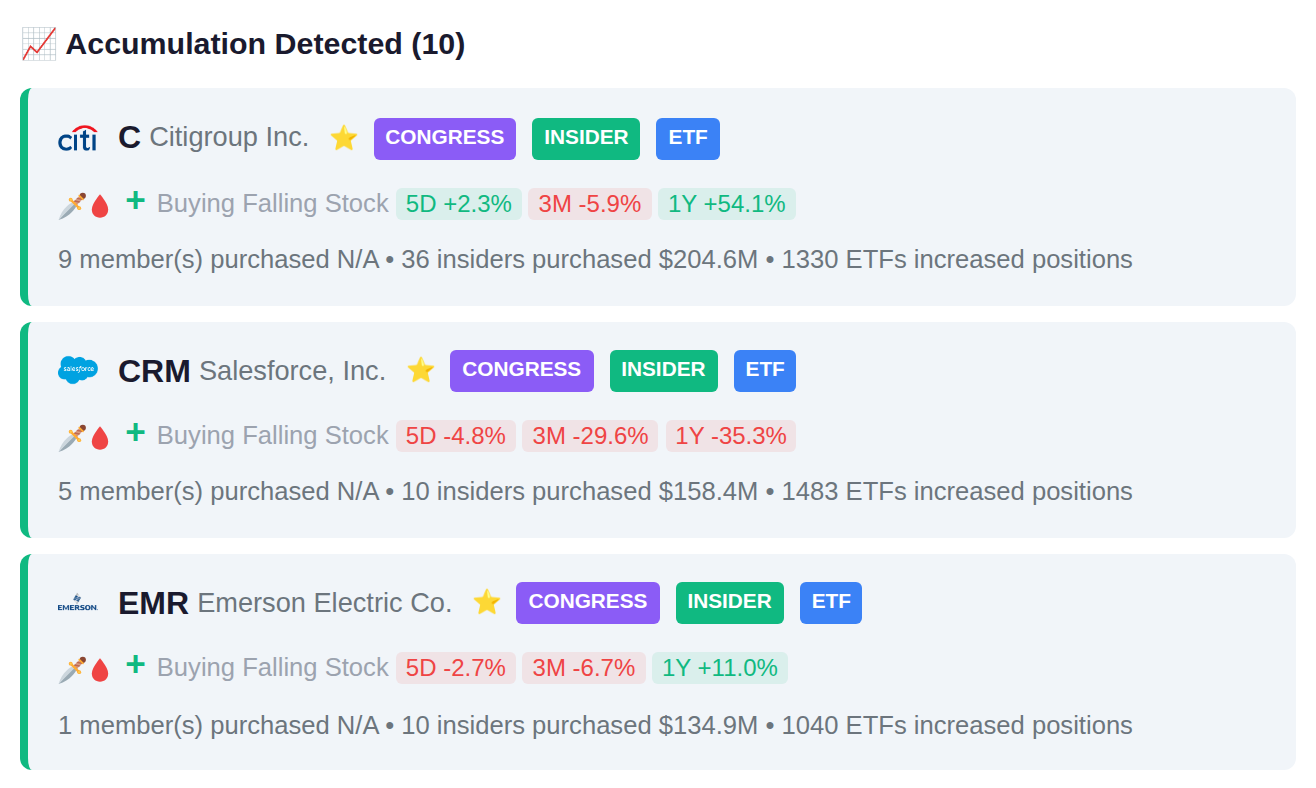

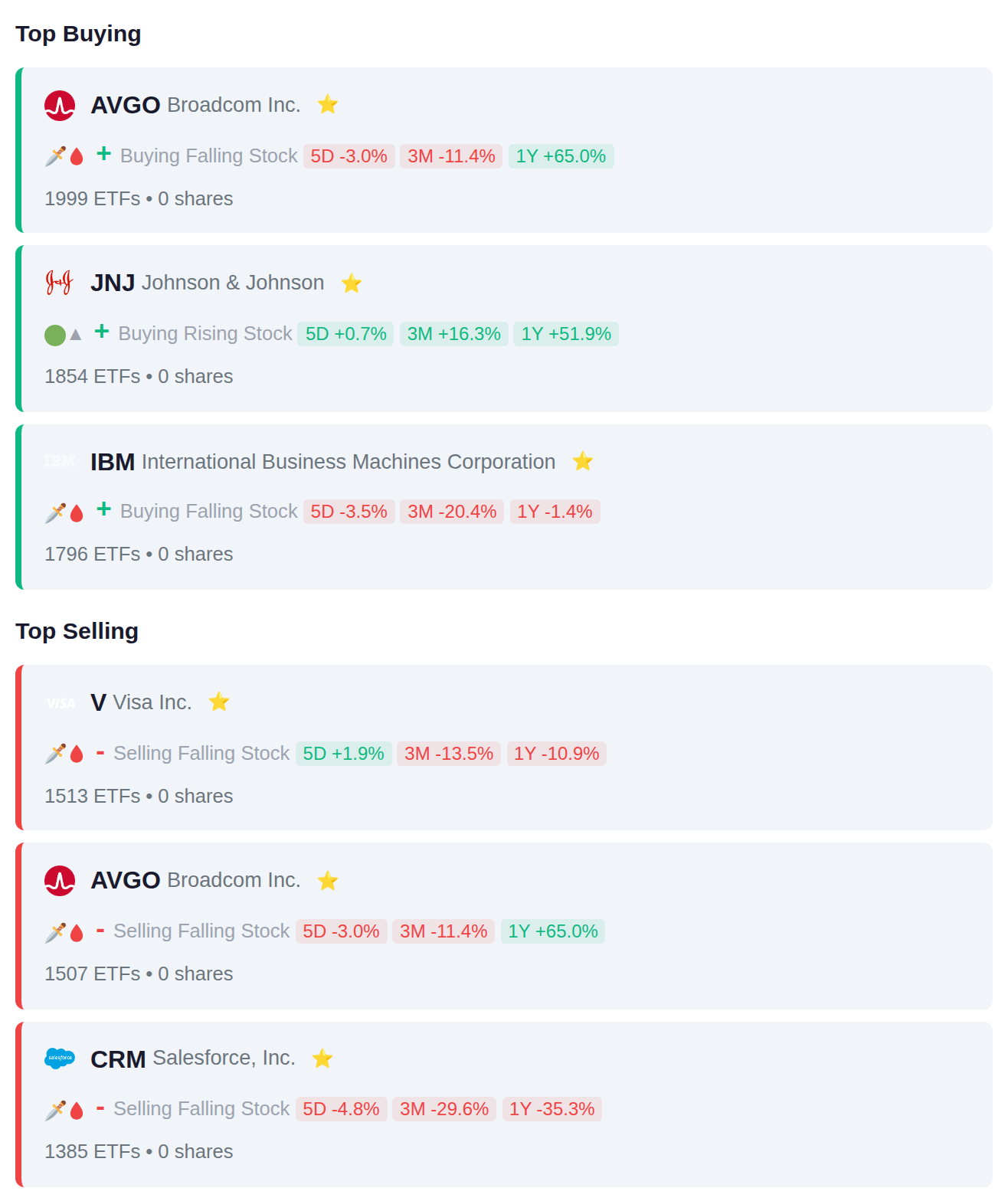

## Institutional Flow Summary ETFs displayed mixed positioning in technology during the recent period, with 1,999 funds adding Broadcom while 1,507 simultaneously reduced their positions, suggesting rotation within the semiconductor space. The data shows institutions added healthcare exposure through Johnson & Johnson (1,854 ETFs) and legacy technology via IBM (1,796 ETFs), while reducing payments infrastructure holdings in Visa (1,513 ETFs) and enterprise software positions in Salesforce (1,385 ETFs).

# Congressional Trading Activity Rep. Tim Moore executed multiple transactions this period, purchasing shares of CBRL and making two separate purchases of LGIH, while also selling his position in DNUT. Additionally, Rep. Warren Davidson sold shares of GEHC and Rep. David Taylor sold CVX. The activity shows Rep. Moore as the most active trader with four total transactions, demonstrating concentrated buying interest in LGIH with two separate purchases alongside his other moves.

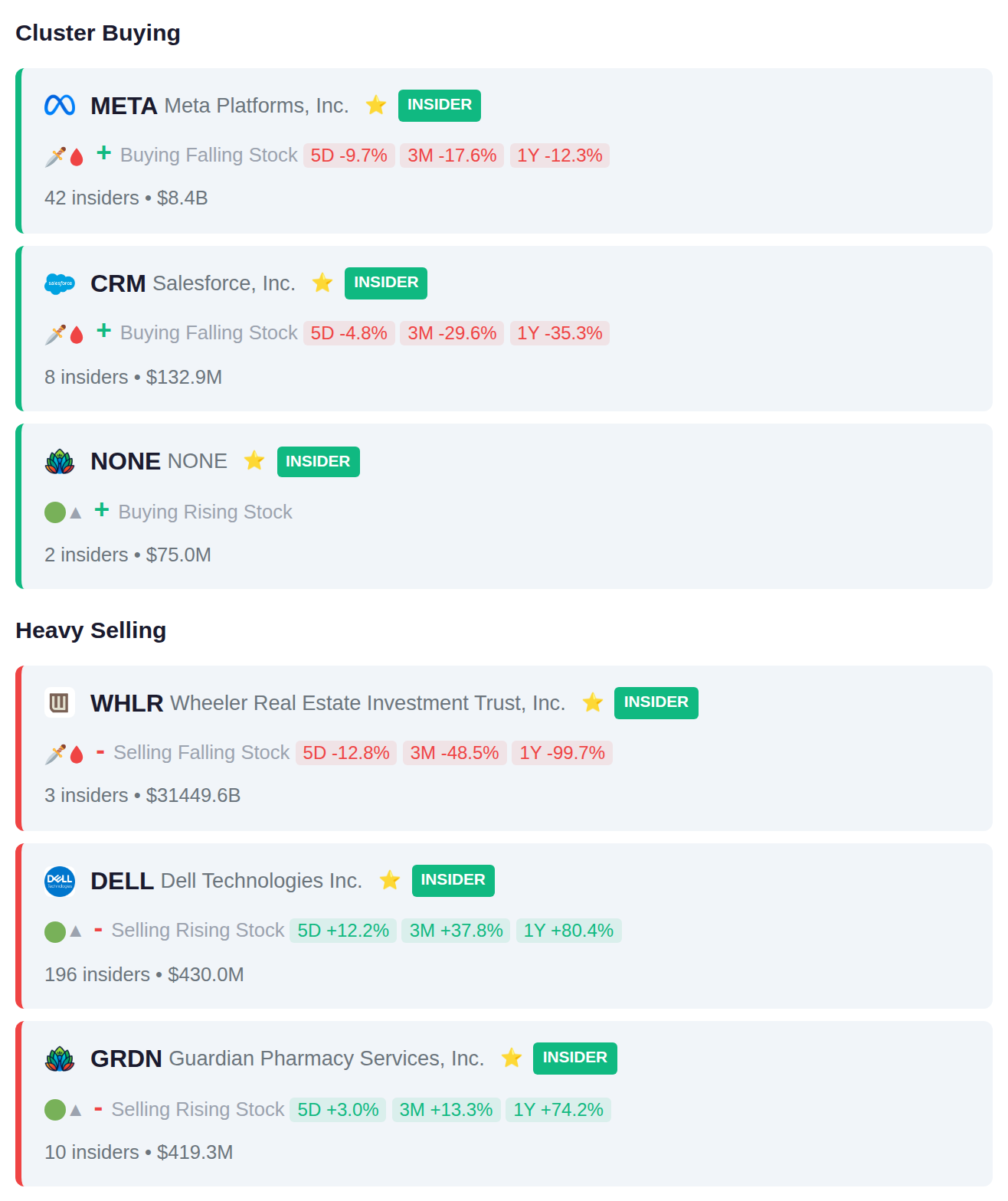

META recorded the highest concentration of insider activity with 42 insiders receiving purchases or awards, while CRM saw 8 insiders participate in similar transactions. On the distribution side, DELL had the largest cluster with 196 insiders collectively selling $430.0M in shares, followed by GRDN where 10 insiders reduced positions totaling $419.3M.

Today 351 stocks report earnings, with notable accumulation signals appearing in PTBA.JK ahead of its results, while TLKM.JK and BRPT.JK show distribution patterns before reporting. Yesterday's session saw significant moves in ABXX.NE, which gained 26.1%, followed by SMTGF up 21.8% and ABXXF adding 21.3%. No companies are scheduled to report tomorrow.