The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

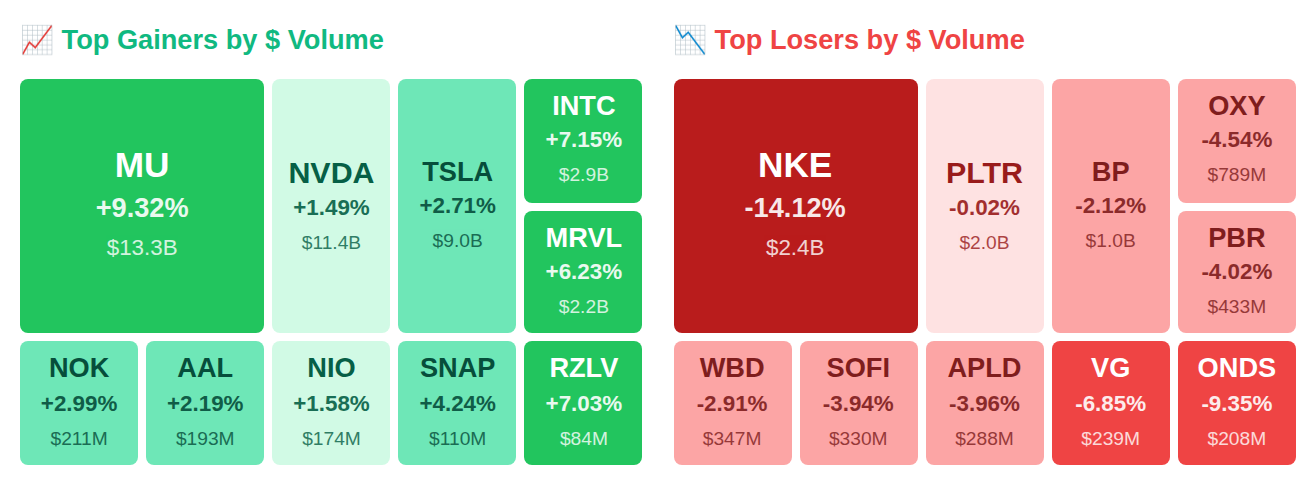

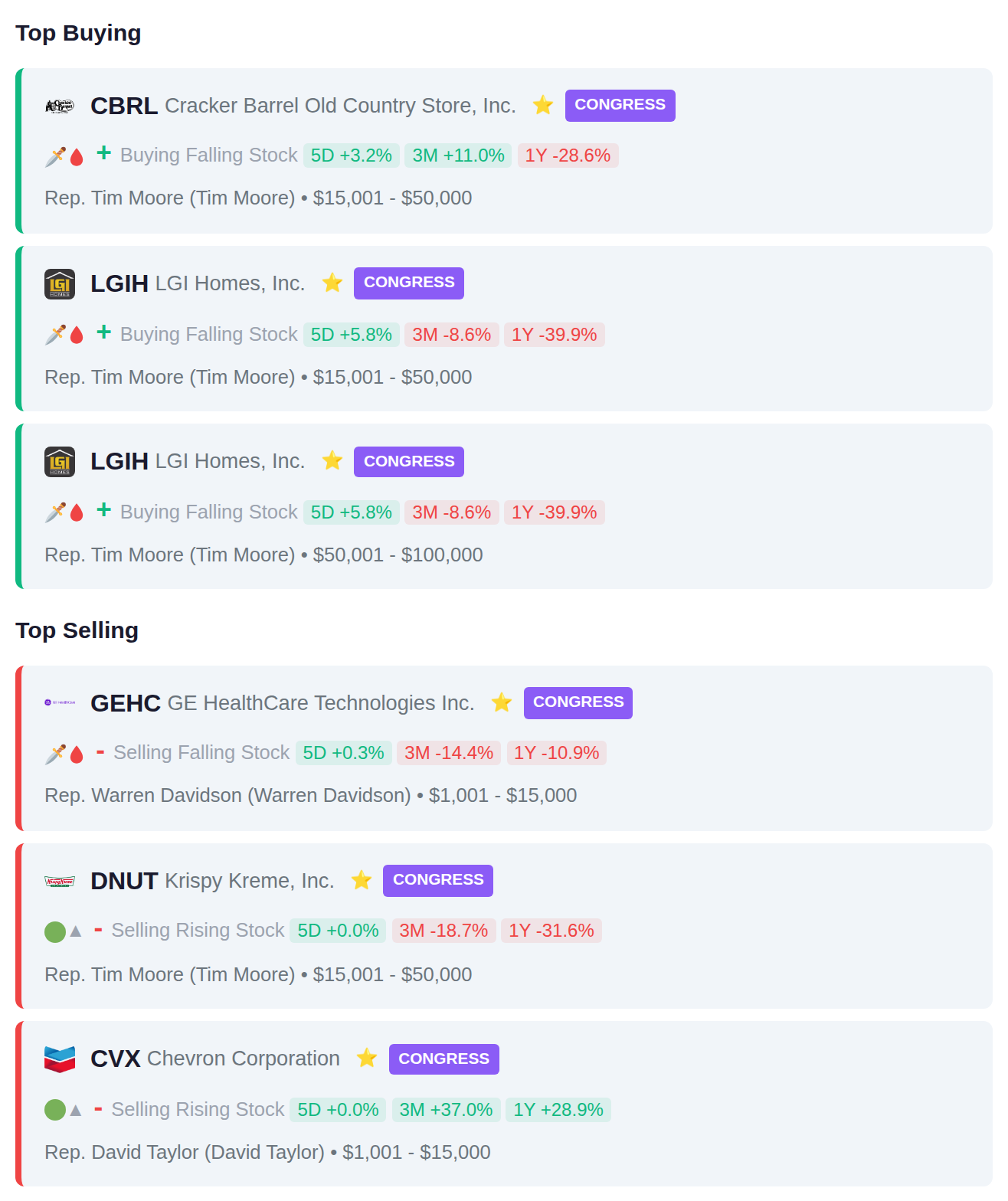

While Rep. Tim Moore (R-NC) quietly scooped up Cracker Barrel Old Country Store (CBRL) shares worth up to $50,000, six insiders at Wheeler Real Estate Investment Trust (WHLR) unloaded a staggering $31.4 billion—part of a $31.4 trillion net outflow that makes today's smart money flow look like a fire sale in reverse. The VIX spiked 17.1% to 30.6 as fear crept back in, yet after hours told a different story: Micron Technology (MU) surged 9.4% on memory supercycle revival talk, Intel (INTC) jumped 9.9% after reacquiring its Irish chipmaking facility, and Lumentum Holdings (LITE) popped 9.9% on whispers of Nvidia (NVDA) pouring billions into strategic plays. Here's what smart money did today while volatility rattled the cages.

📚 Jargon Buster

Labor Force Participation

What percent of adults actually want to work. Been stuck since COVID like your uncle on the couch.

The VIX surged 17.1% over the past week to reach 30.61, signaling heightened fear in equity markets and placing volatility well into the high-stress territory typically associated with significant market uncertainty or turmoil. In contrast, the MOVE index measuring bond market volatility registered just 13.82 with a modest 1.4% weekly increase, indicating that fixed income markets remain relatively calm. This divergence suggests equity investors are pricing in considerably more near-term risk than their bond market counterparts, a dynamic that often emerges during periods of stock-specific concerns rather than broader systemic financial stress.

|| Market Sutra ||

"A bull ends when buyers stop caring about price."

— Meme stock mania peaked when fundamentals no longer mattered

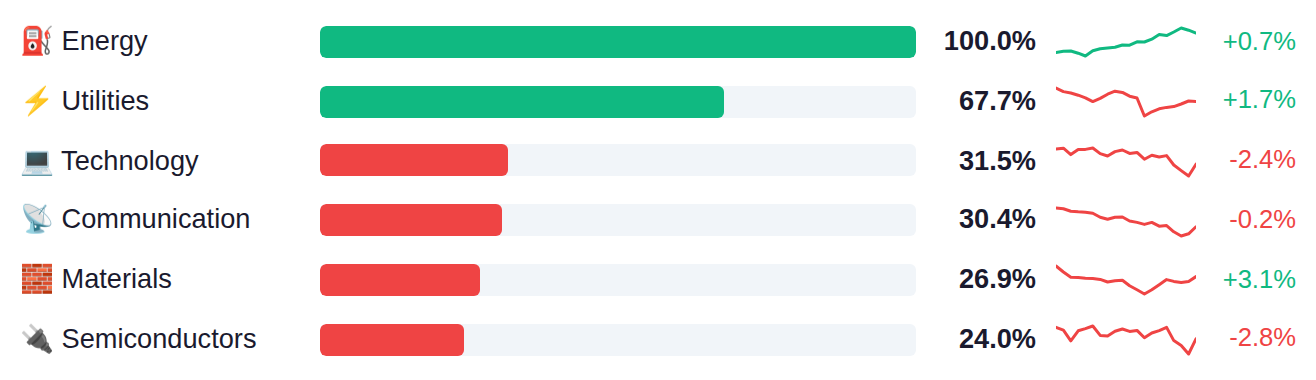

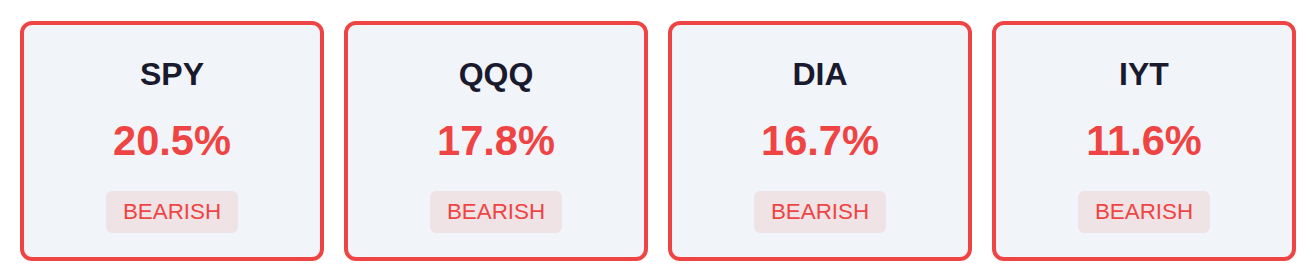

Energy and Utilities are dominating sector leadership with 100% and 68% readings respectively, while defensive positioning is evident as Technology shows moderate strength at 32% and traditional cyclical sectors like Financials, Industrials, and Real Estate lag significantly near zero. Index breadth remains notably weak across major benchmarks, with SPY at only 20% and QQQ at 18%, creating a divergence between the narrow sector leadership in Energy and Utilities and the poor participation across the broader market.

Fed net liquidity stood at $6.66 trillion as of March 25, up $1.2 billion from the prior week, indicating a modest expansion in available dollar liquidity that historically correlates with supportive conditions for risk assets. The next H.4.1 report releases Thursday, April 2, which will show whether this gradual liquidity increase continues or reverses.

Yesterday's data painted a mixed picture as Consumer Confidence surged to 91.8 versus 88.0 expected—a notable beat that contrasts with housing weakness, where Case-Shiller's 1.2% year-over-year gain marked the slowest pace since early 2012 and missed estimates for the third consecutive month. Chicago PMI dropped sharply to 52.8 from 57.7, missing expectations by 2.2 points in the steepest monthly decline since late 2023, while JOLT openings fell to 6.882 million, near the lowest level since 2021 and signaling continued labor market cooling. Today's retail sales data dominated with a clean sweep of beats—headline MoM came in at 0.6% versus 0.3% expected and the core ex-autos print at 0.5% versus 0.3%—though this strength will be weighed against ISM Manufacturing at 52.7 (barely above estimates) and tomorrow's jobless claims, where initial filings are expected to tick up to 212K from 210K as markets watch for any acceleration in labor softness that could influence Fed speakers Musalem and Barr today, followed by Logan and Bowman tomorrow.

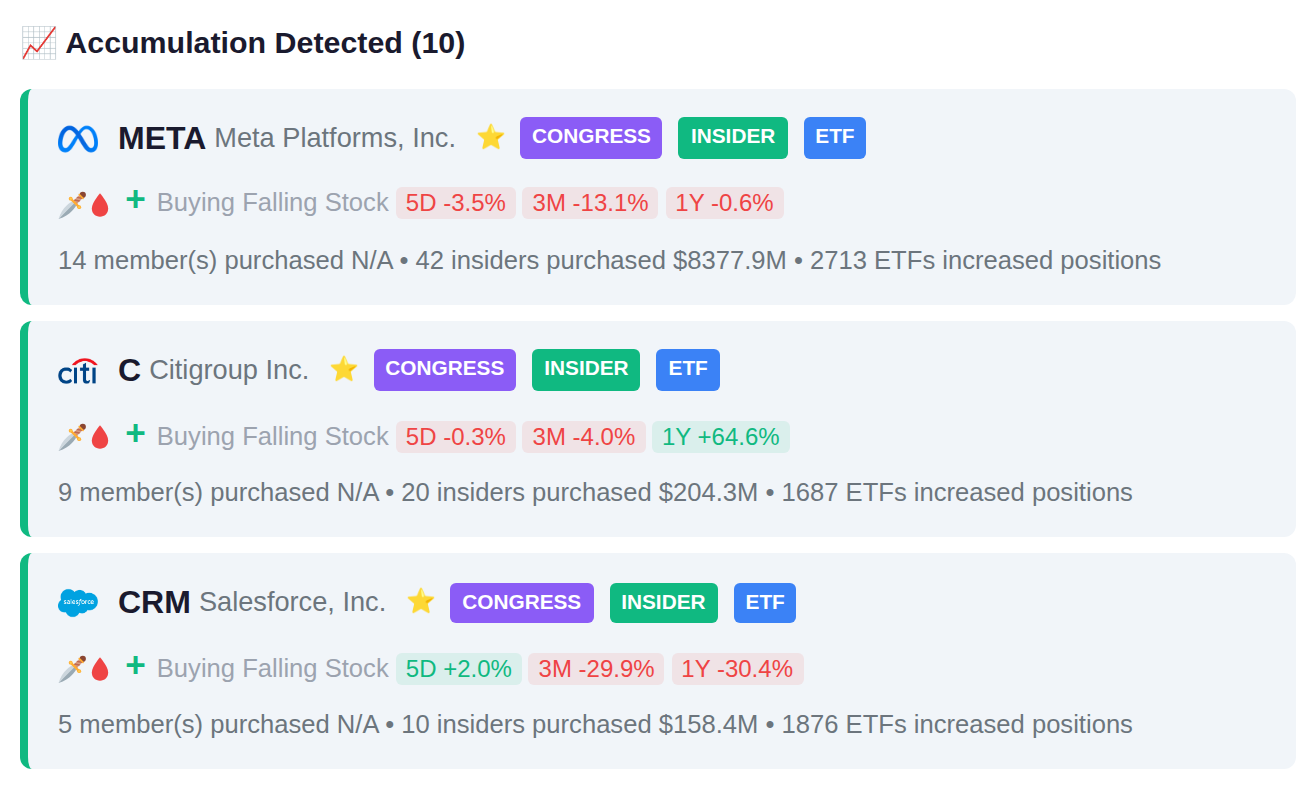

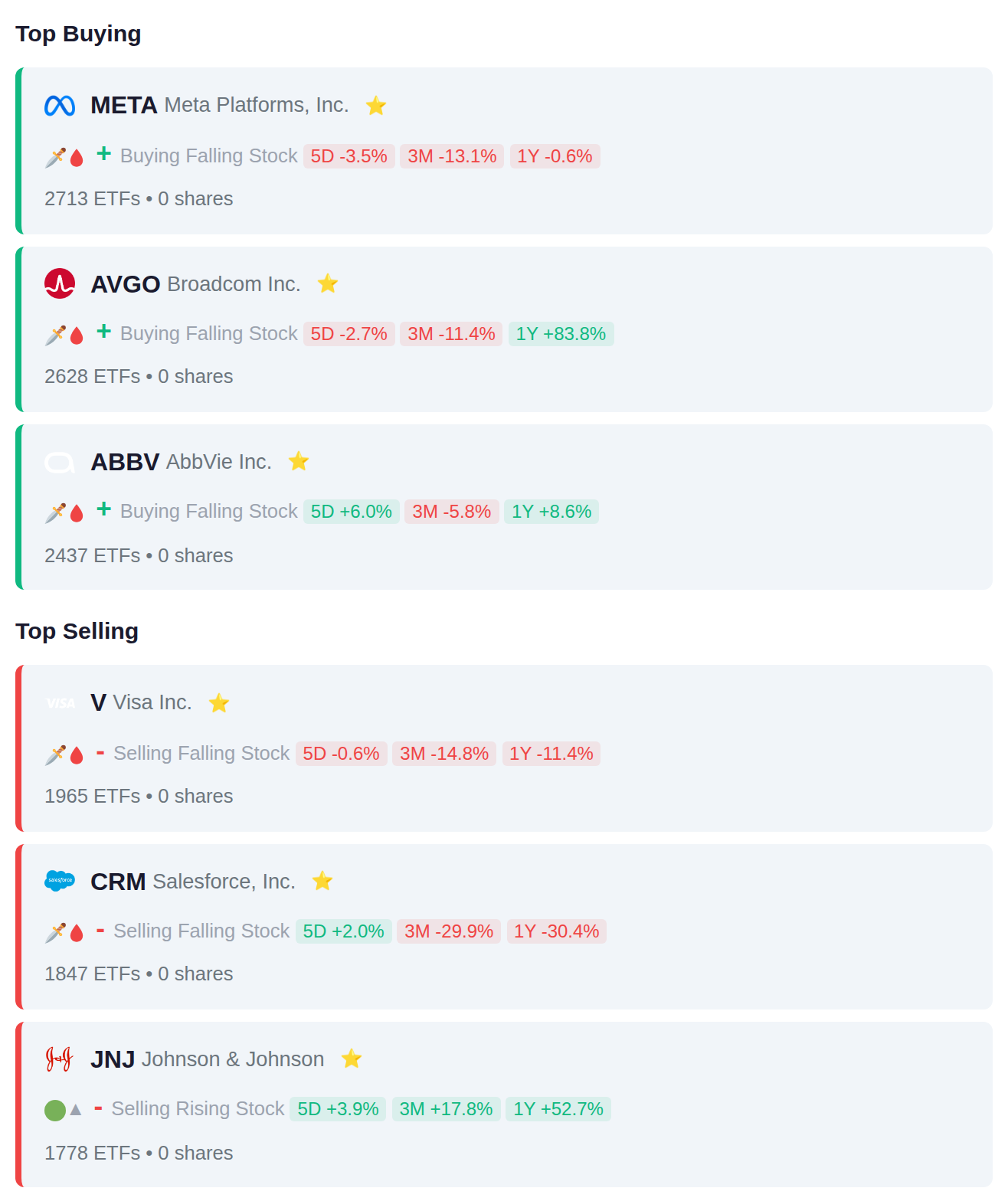

Exchange-traded funds rotated out of payment processors, enterprise software, and healthcare stalwarts during the period, with 1,965 ETFs reducing Visa positions, 1,847 trimming Salesforce, and 1,778 cutting Johnson & Johnson. Simultaneously, institutional money flowed into social media and semiconductor names, as 2,713 ETFs added Meta Platforms and 2,628 increased Broadcom holdings, while 2,437 accumulated pharmaceutical giant AbbVie, suggesting a shift from diversified healthcare into focused pharma exposure.

Rep. Tim Moore purchased shares of Cracker Barrel (CBRL) and made multiple purchases of LGI Homes (LGIH), while divesting from Krispy Kreme (DNUT). Meanwhile, Rep. Warren Davidson sold GE HealthCare (GEHC) and Rep. David Taylor reduced his position in Chevron (CVX), with the activity showing concentrated buying interest in consumer discretionary and homebuilding sectors alongside exits from healthcare and energy positions.

Multiple insiders at META executed 42 transactions involving purchases or award activities, while CRM recorded 8 similar insider transactions during this period. On the distribution side, WHLR saw 6 insiders sell positions totaling $31.4 billion, GRDN had 10 insiders reduce holdings worth $419.3 million, and WMT reported 5 insiders selling approximately $407.0 million in shares.

Seventy-six companies report earnings today, with institutional accumulation patterns evident in XOM.NE and 5942.T ahead of their releases. Distribution signals have emerged in MAPI.JK and BSDE.JK, also scheduled to report today. Yesterday's session saw notable moves with KOD gaining 74.5%, PPTA advancing 11.7%, and USAS declining 10.2%.