The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

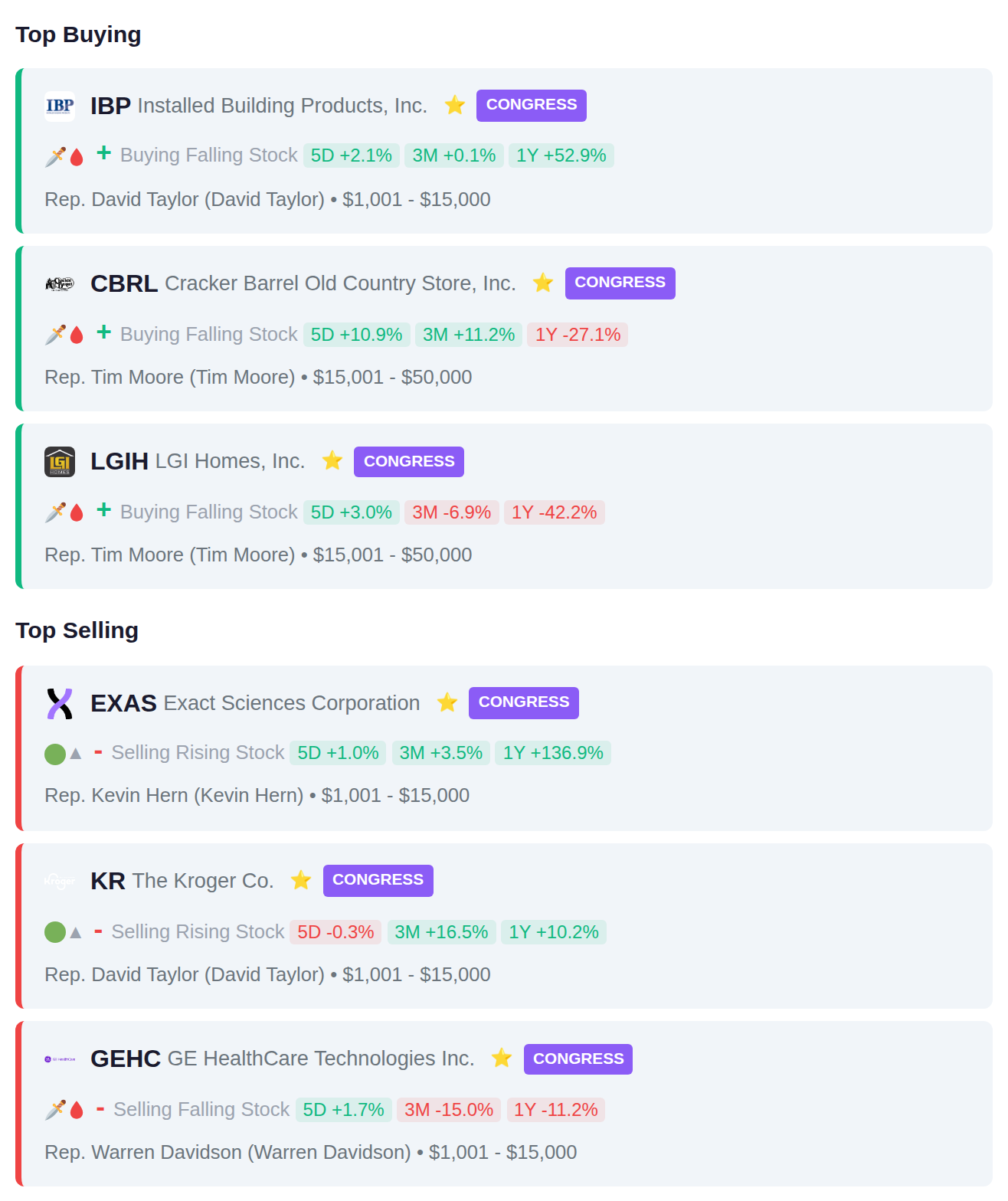

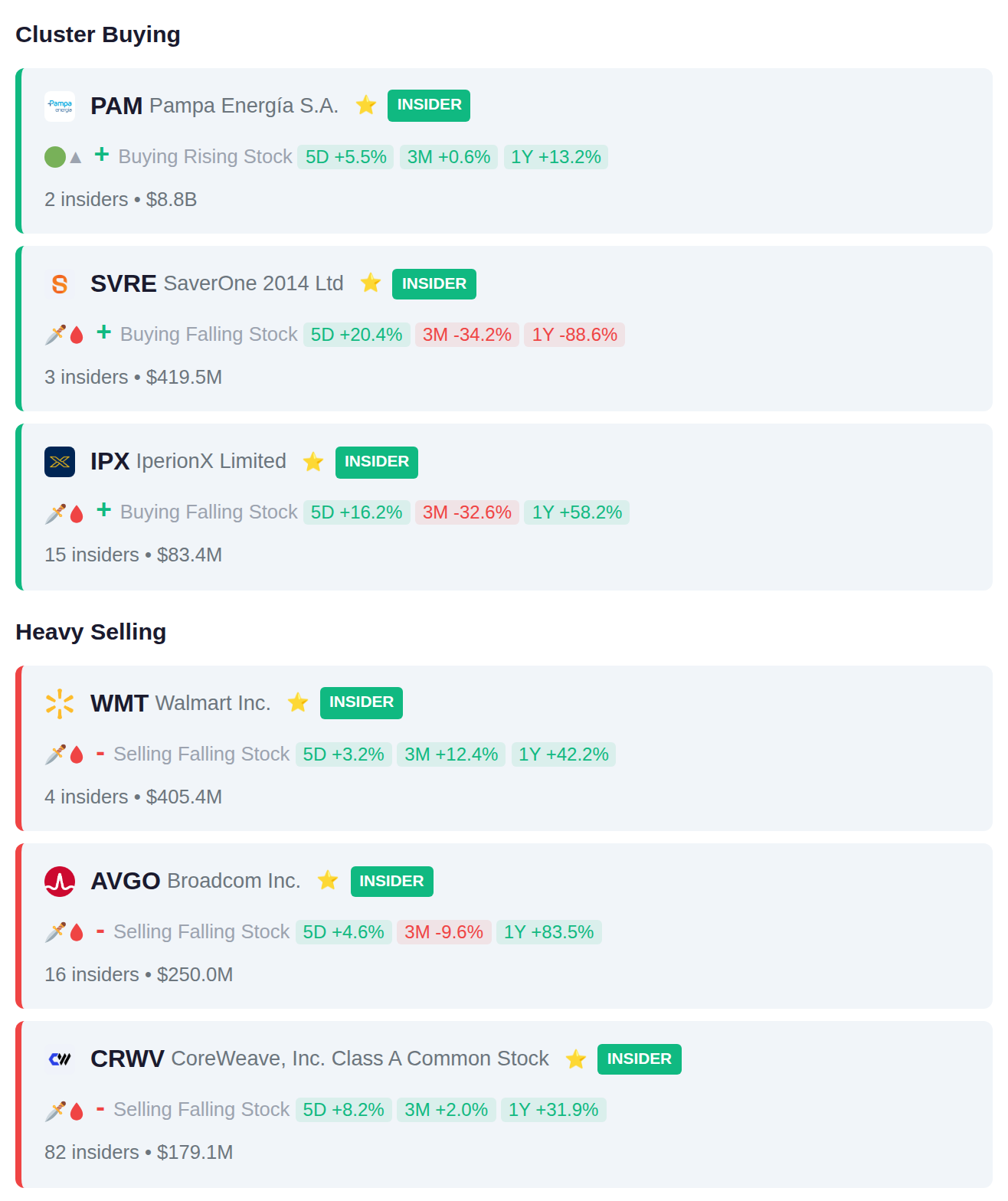

While VIX cratered 13% and everyone pretended calm returned to markets, four insiders at Walmart (WMT) quietly unloaded $405.4 million in stock—the kind of exit that makes you wonder what they're seeing in those weekly sales numbers. Meanwhile, Rep. David Taylor picked up shares of Installed Building Products (IBP), AppLovin (APP) popped 6.8% on an analyst upgrade despite being down 33% this year, and MicroStrategy (MSTR) somehow rallied another 6.6% while sitting on $14 billion in Bitcoin paper losses. Here's what smart money is doing today.

📚 Jargon Buster

Housing Starts

How many new homes builders broke ground on. When mortgage rates are 8%, this number goes to sleep.

Equity volatility remains elevated with the VIX at 23.87, though the 13.0% weekly decline suggests some easing of fear in stock markets from higher levels. The picture diverges sharply in fixed income, where the MOVE index dropped 42.9% to 10.48, indicating unusually low bond market volatility and a stark contrast to the lingering caution still present in equity markets. This split between asset classes reflects uncertainty about equity direction while bond traders appear relatively sanguine about interest rate movements.

|| Market Sutra ||

"When the data whispers, the market listens."

— Soft inflation prints in late 2022 triggered massive rotation before the Fed acknowledged it

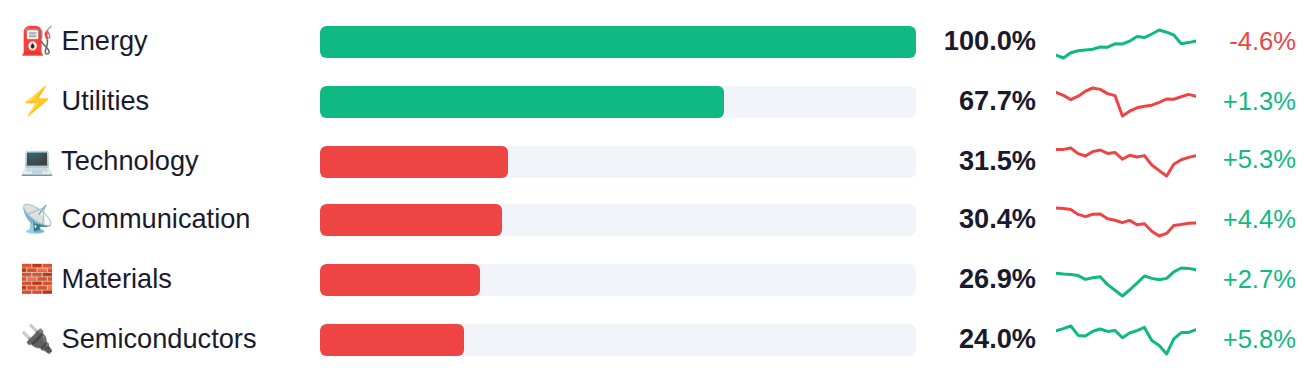

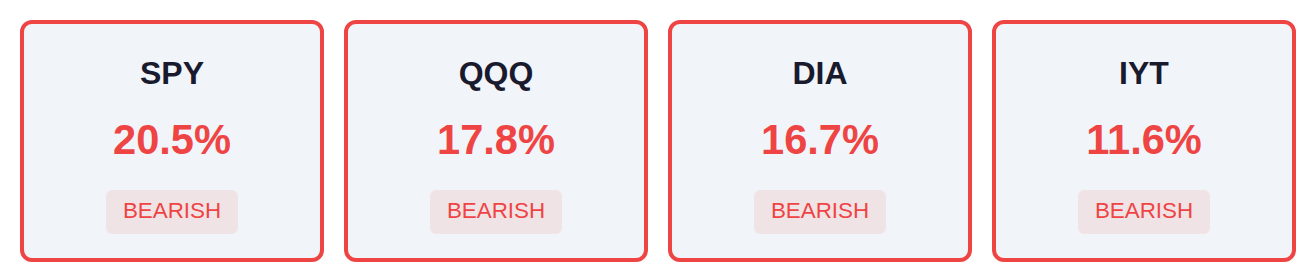

Energy is demonstrating the strongest relative performance with full participation, while Utilities and Technology are showing meaningful but more moderate leadership at 68% and 32% respectively. The market is experiencing notably weak breadth across major indices, with SPY, QQQ, and DIA all registering participation below 21%, suggesting gains are concentrated in a narrow set of names even within the leading sectors. Real Estate, Industrials, and Financials are lagging significantly, creating a bifurcated market where defensive sectors like Utilities are performing alongside more cyclical areas like Energy, an unusual combination that reflects mixed economic signals.

Federal Reserve net liquidity stood at $6.68 trillion as of April 1st, increasing $18.2 billion week-over-week, which typically correlates with expanded market liquidity conditions when the metric rises. The next H.4.1 statistical release providing updated Fed balance sheet data drops Thursday, April 9th.

Yesterday's ISM services data painted a concerning stagflationary picture as the prices paid component surged to 70.7—beating estimates of 67.0 and jumping 7.7 points from February's 63.0—while the headline PMI disappointed at 54.0 versus 54.8 expected and employment collapsed to 45.2, missing estimates by 5.8 points and falling deep into contraction territory from 51.8 prior. The 70.7 prices reading marks the highest level since June 2022 when the Fed was aggressively hiking rates, suggesting persistent inflation pressures in the services sector which comprises roughly 70% of the U.S. economy. Today's focus shifts to February durable goods orders where headline orders are expected to decline 0.5% after a 0.4% gain, though the core ex-transportation measure is forecast to rise 0.5% versus 0.4% prior, while tomorrow brings heightened scrutiny on FOMC minutes and speeches from Fed officials Daly, Waller, and the critical policy discussion as markets weigh whether yesterday's sticky services inflation combined with weakening employment will complicate the Fed's rate path deliberations.

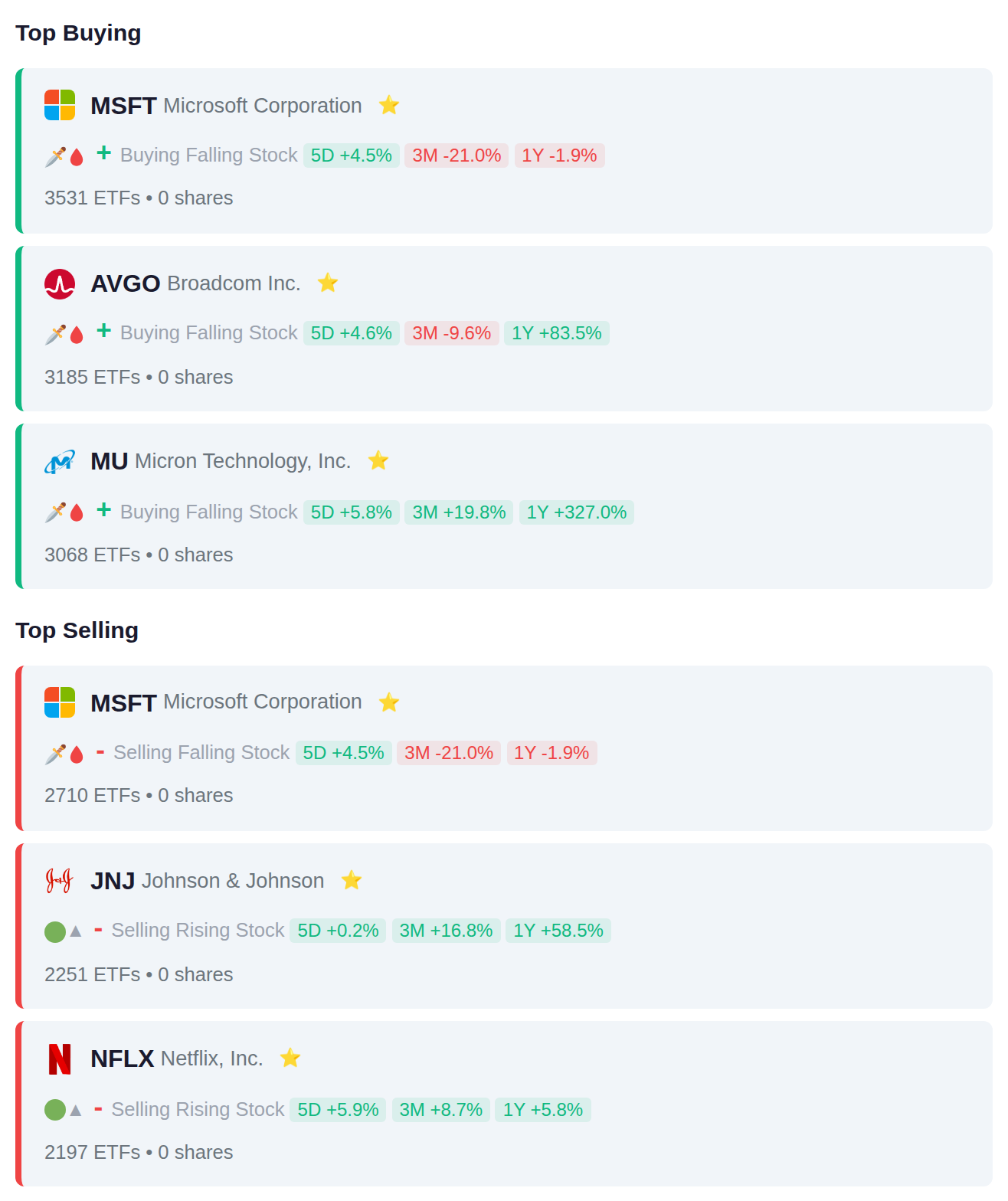

Large-cap technology names dominated institutional ETF flows this period, with MSFT drawing additions from 3,531 ETFs despite 2,710 simultaneously reducing positions, while semiconductor exposure expanded via AVGO and MU accumulation by 3,185 and 3,068 funds respectively. The removal activity showed a defensive rotation away from healthcare stalwart JNJ (2,251 ETFs selling) and streaming leader NFLX (2,197 ETFs selling), suggesting institutions rebalanced from consumer discretionary and healthcare into chip-heavy technology sectors.

Congressional trading activity shows Rep. David Taylor made offsetting moves by purchasing IBP while selling KR, both in the consumer staples sector. Representatives Tim Moore concentrated purchases in two positions (CBRL and LGIH), while Reps. Kevin Hern and Warren Davidson each reduced single healthcare-related holdings (EXAS and GEHC respectively).

Over the past week, 15 insiders at IPX coordinated purchases while 82 insiders at CRWV executed sales totaling $179.1M, representing the most concentrated cluster activity. Additional notable coordinated selling occurred at WMT where 4 insiders offloaded $405.4M in shares and at AVGO where 16 insiders disposed of $250.0M in holdings.

Yesterday's session saw ATX.V surge 10.7%, while Japanese names 8923.T and TIIAY advanced 6.3% and 5.8% respectively. Today's earnings calendar features 32 companies, with accumulation signals noted in 1377.T and 2659.T, while institutional distribution has been detected in NCKL.JK and 2726.T ahead of their reports. No companies are scheduled to report tomorrow.