The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

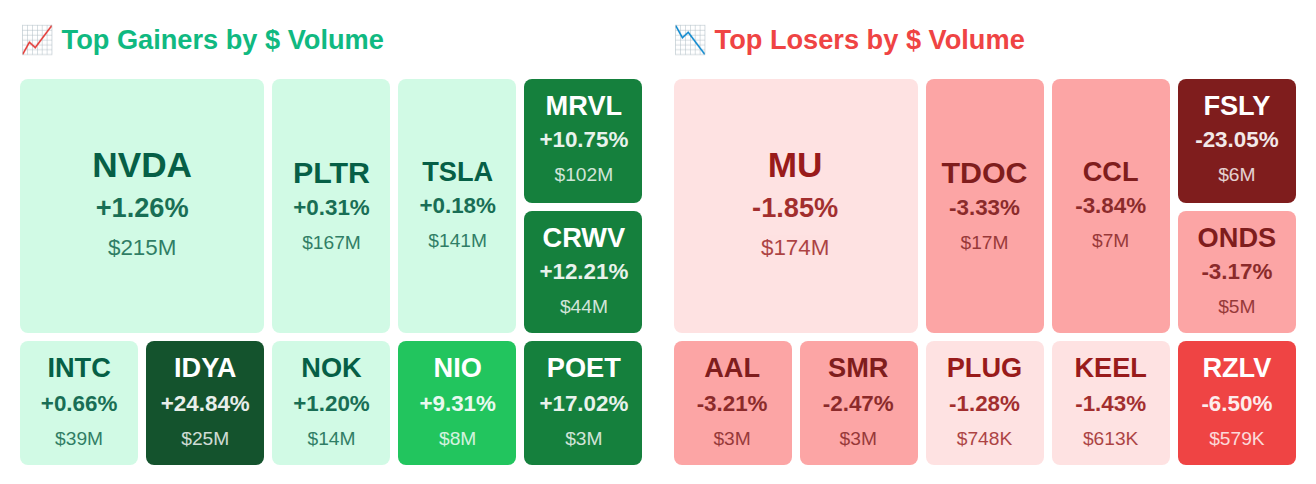

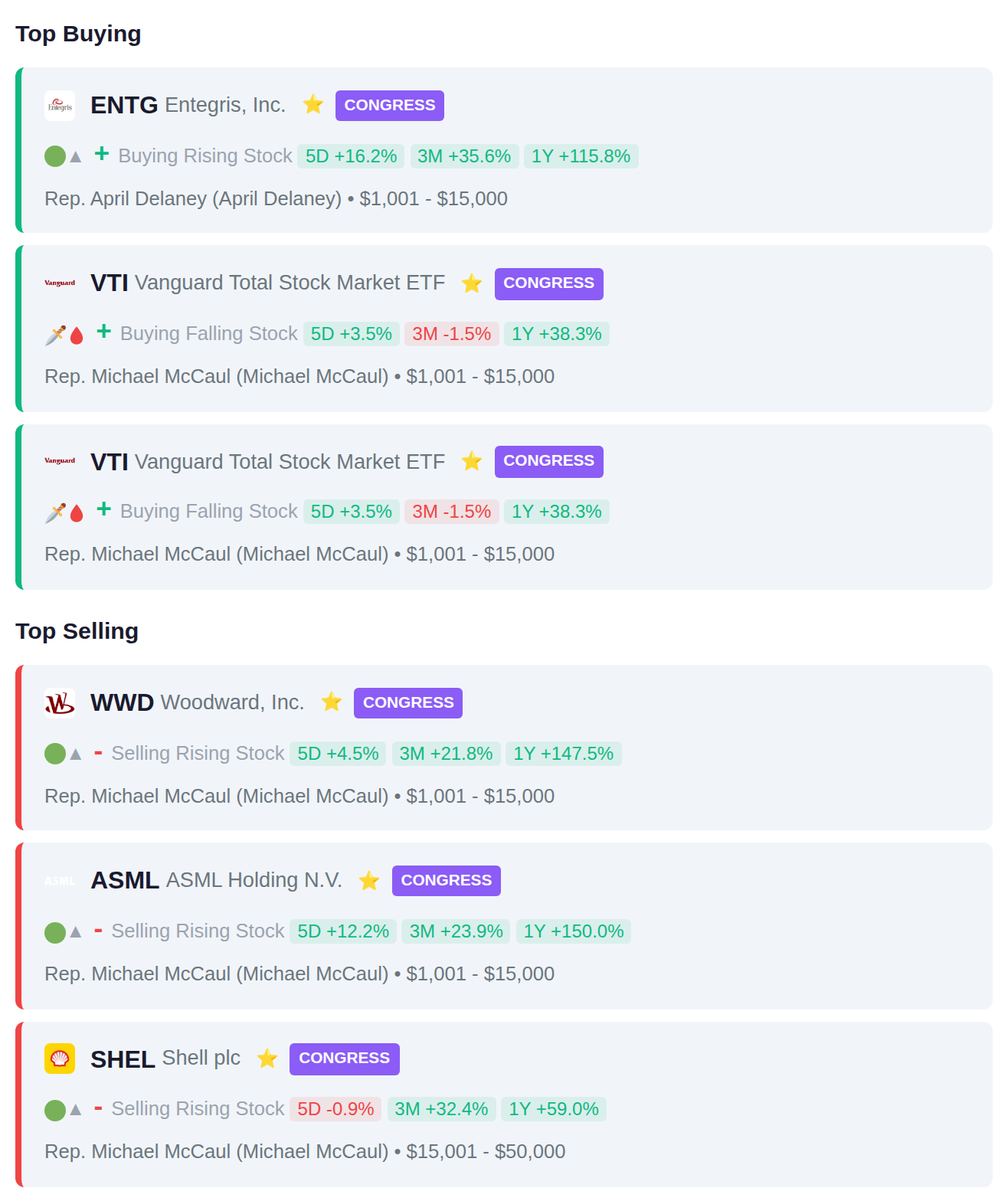

While Rep. April Delaney (D-MD) quietly added Entegris Inc. (ENTG) shares and insiders at Live Nation Entertainment (LGN) dumped $1.7 billion in stock, the real aftermarket chaos hit Applied Optoelectronics (AAOI)—up 13% to $150.60 on a volume frenzy after its 1,307.5% one-year rocket ride—and Coherent Corp. (COHR), which surged 8.2% to $307.50 on a silicon carbide breakthrough fueling AI data center dreams. With $2.3 billion in net smart money outflows and the VIX plunging 20.6% to 19.5, someone's rotating aggressively while others cash out big. Here's what smart money did today.

📚 Jargon Buster

Autism Strength

The superpower that lets apes hold through -90% because “fundamentals still strong 💪🧠”

Equity market volatility declined sharply this week, with the VIX falling over 20% to 19.49 and settling into normal territory, suggesting reduced concern among stock investors about near-term price swings. In contrast, bond market volatility told a different story, as the MOVE index jumped 28.5% to 10.90, indicating heightened uncertainty in fixed income markets despite remaining at historically low absolute levels. This divergence between equity calm and rising bond market jitters reflects differing assessments of risk across asset classes, with fixed income traders appearing more cautious about potential interest rate or policy shifts than their equity counterparts.

|| Market Sutra ||

"The best signals appear when nobody is looking."

— Breadth turned bullish in 2016 before headlines noticed

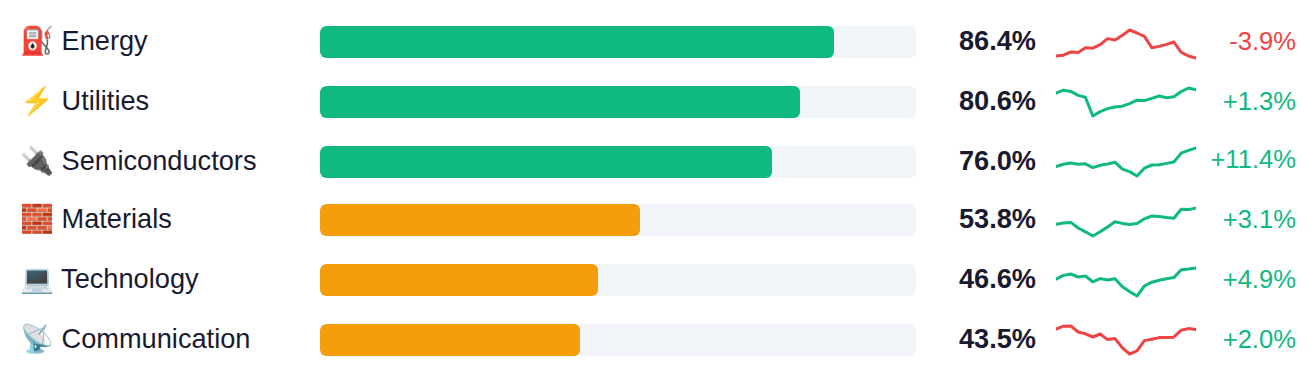

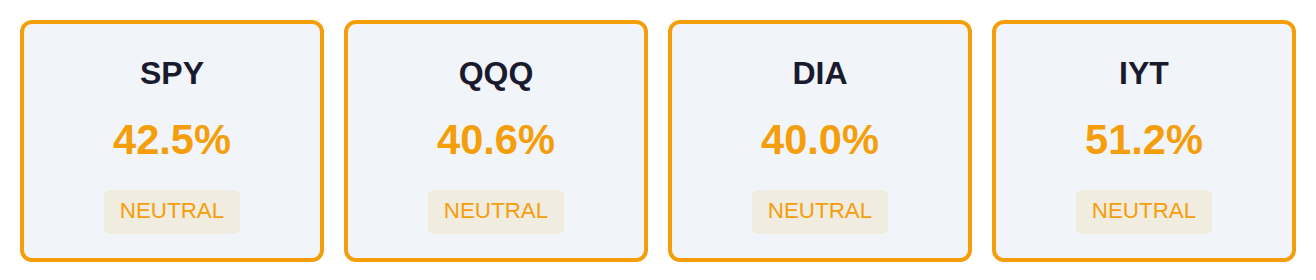

Market breadth remains compressed with fewer than half of constituents participating in the current advance across major indices, though transportation shows marginally better internal strength at 51%. Energy, utilities, and semiconductors are leading with participation rates above 75%, while defensive sectors including consumer staples, healthcare, and consumer discretionary show notably weaker participation below 40%, suggesting a bifurcated market with momentum concentrated in cyclical and technology-related areas rather than broad-based strength.

As of April 8, Fed net liquidity stood at $6.69 trillion, declining $18.5 billion week-over-week, which represents a tightening in system-wide dollar availability that historically correlates with increased pressure on risk asset valuations. The next H.4.1 report releases Thursday, April 16, which will reveal whether this liquidity drain accelerated or reversed course.

March inflation data came in cooler than expected across most measures, with core CPI rising just 0.2% month-over-month versus the 0.3% estimate and the 2.6% year-over-year rate beating the 2.7% forecast, though the headline monthly jump to 0.9% from February's 0.3% marks the sharpest single-month acceleration since June 2022. The more concerning development emerged in consumer sentiment, which plunged to 47.6 from 53.3—the lowest reading since June 2022—while one-year inflation expectations surged to 4.8% from 3.8%, the highest since November 2023 and a full 60 basis points above the 4.2% estimate, suggesting consumers are pricing in persistent price pressures despite the Fed's tightening campaign. Traders now turn to today's existing home sales data (expected at 4.06M versus 4.09M prior) and tomorrow's Producer Price Index forecast at 1.2% month-over-month—nearly double February's 0.7%—which could signal building pipeline inflation pressures even as consumer-level readings moderate.

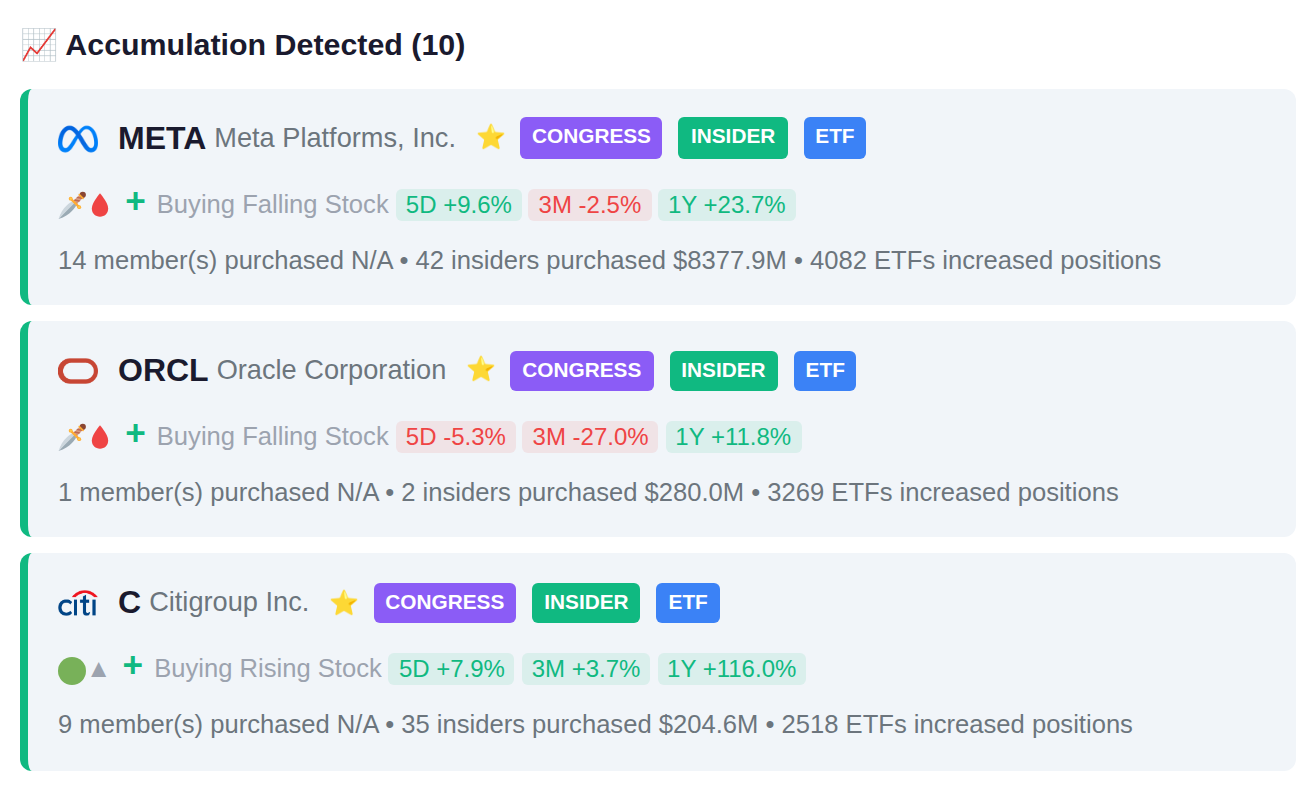

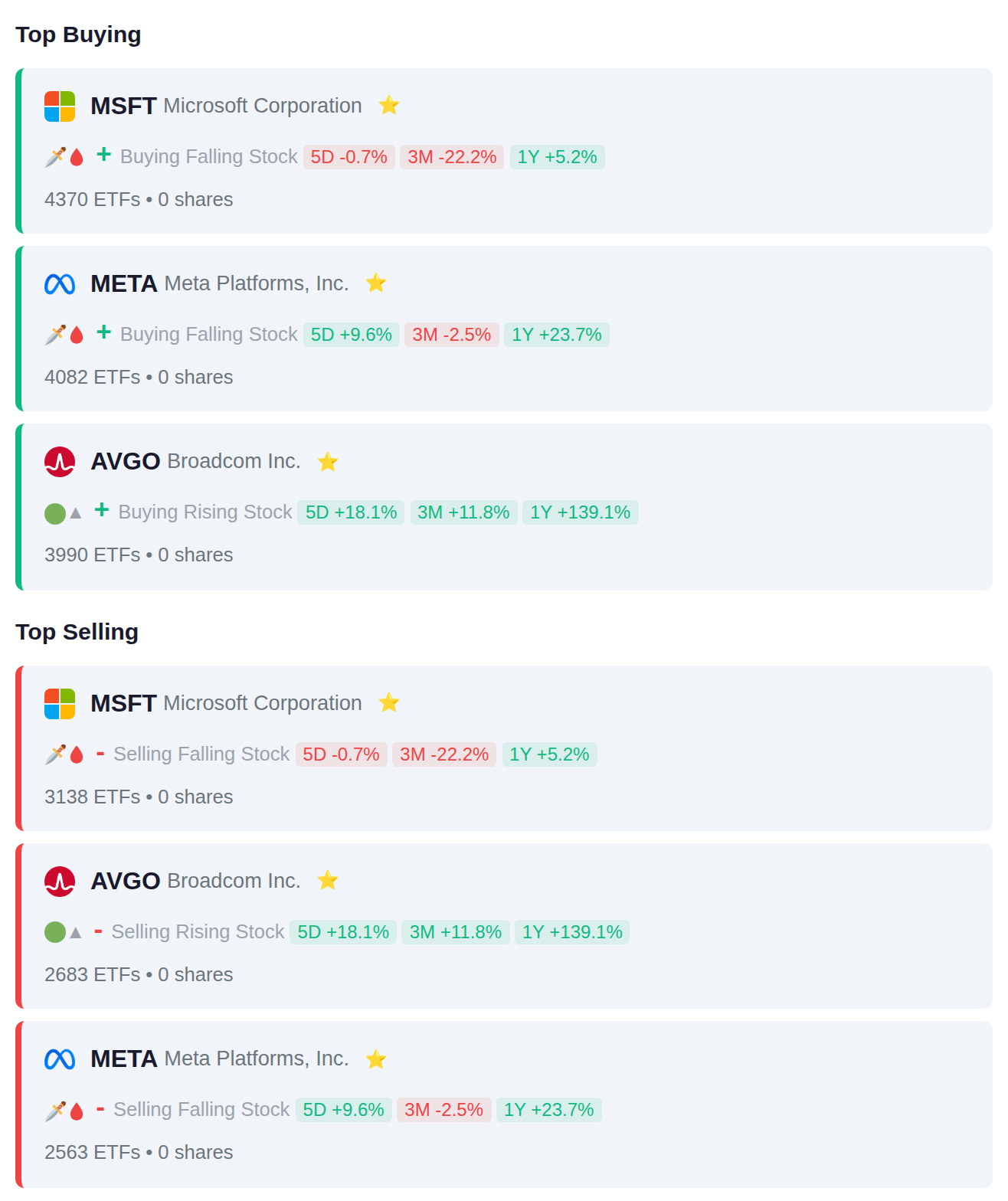

Institutional flow data shows mixed positioning in mega-cap technology, with 4,370 ETFs adding Microsoft positions while 3,138 reduced them, alongside similar split activity in Meta (4,082 adding vs 2,563 removing) and Broadcom (3,990 adding vs 2,683 removing). The balanced 10-to-10 ratio of funds increasing versus decreasing exposure suggests institutional managers are rotating within the technology sector rather than making directional bets on the space overall.

Rep. Michael McCaul executed multiple transactions, reducing positions in WWD, ASML, and SHEL while adding to VTI holdings through two separate purchases. Rep. April Delaney purchased shares of ENTG, while McCaul's activity shows a shift from individual stocks toward broader market exposure through the Vanguard Total Stock Market ETF.

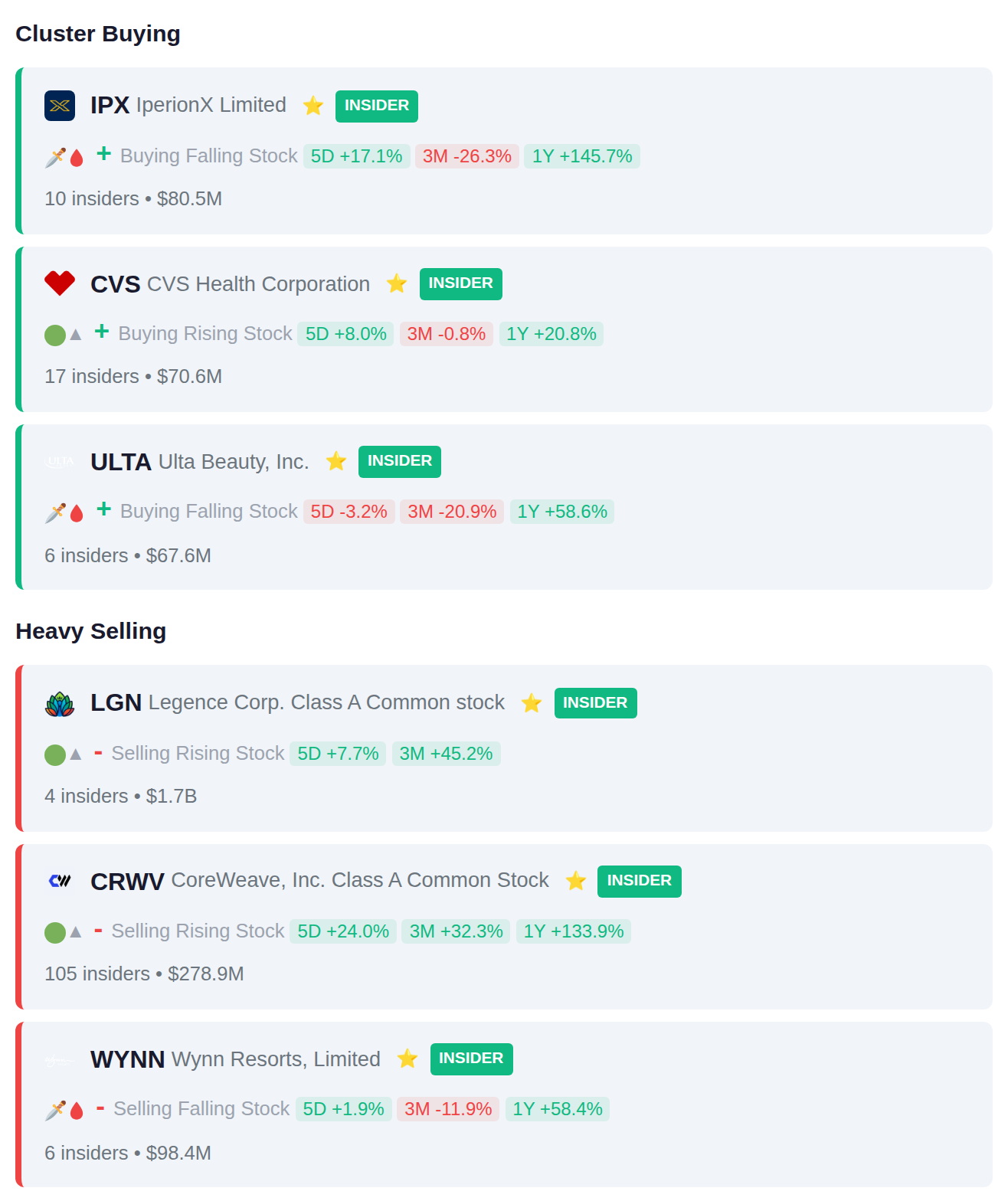

Recent insider activity shows concentrated accumulation at CVS Health with 17 insiders adding positions, while IPX recorded 10 insider purchases and ULTA saw 6 insiders acquiring shares. On the distribution side, CRWV led with 105 insiders selling $278.9M in aggregate, followed by significant dispositions at LGN where 4 insiders offloaded $1.7B and WYNN where 6 insiders reduced positions totaling $98.4M.

Today's earnings slate features 122 companies, with notable smart money positioning in 4530.T and GS.NE showing recent accumulation signals ahead of their reports. Meanwhile, institutional investors have reduced positions in BISI.JK and 2408.TW, which also report today. Yesterday's session saw significant moves in LOT, which surged 31.9%, while 000977.SZ and 6919.TWO gained 19.1% and 18.0% respectively.