The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

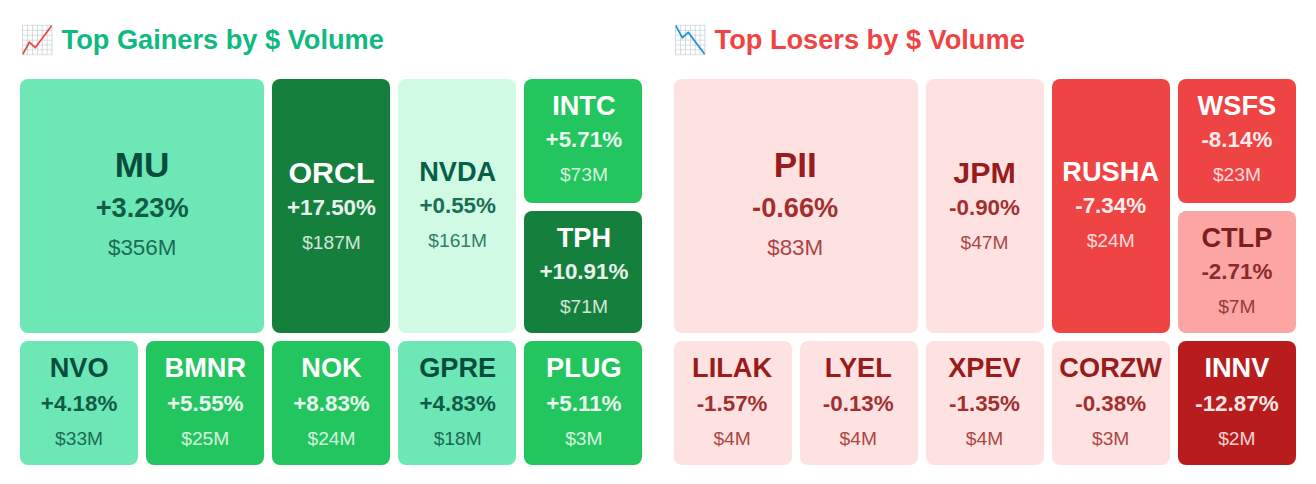

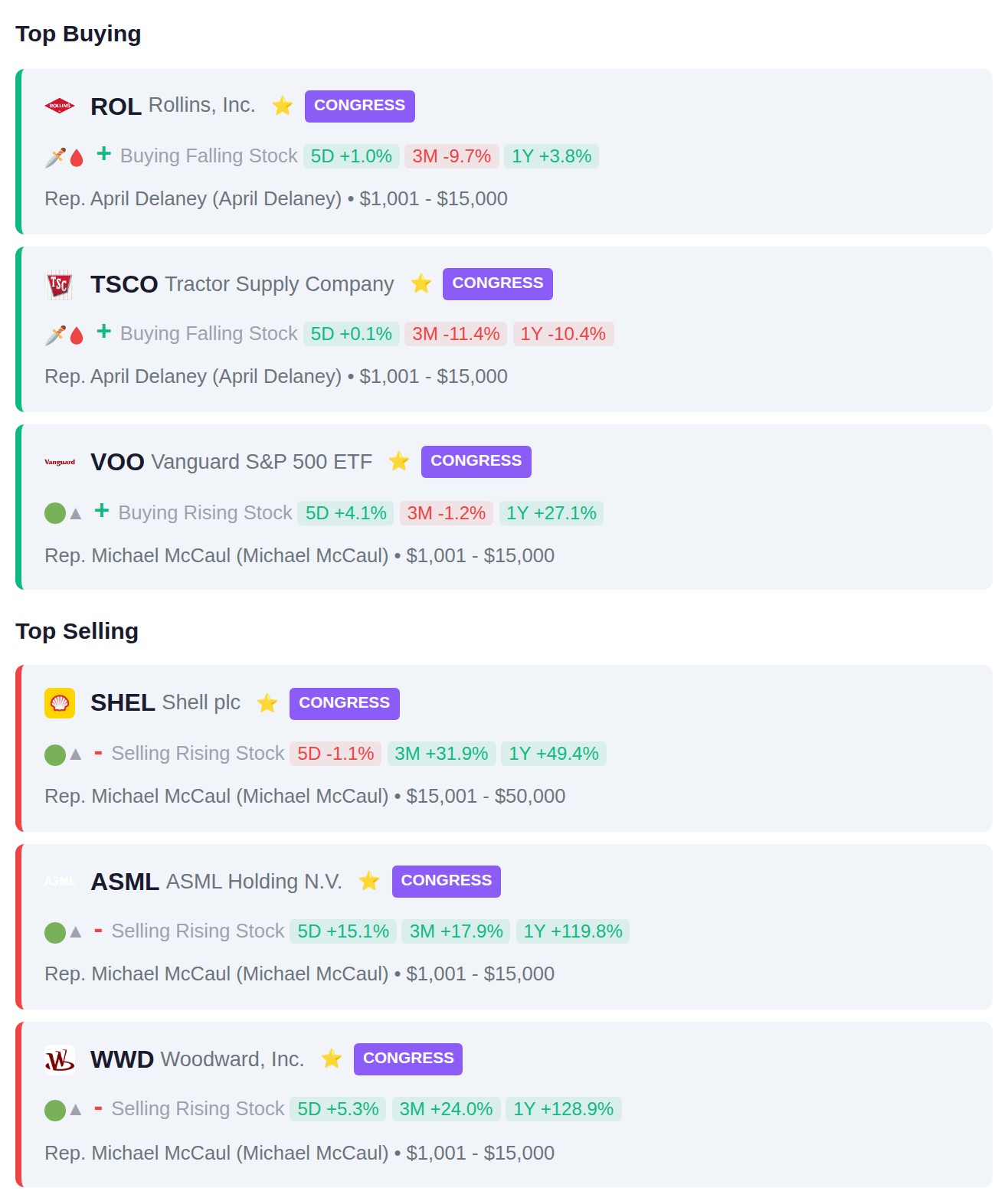

While Oracle Corporation (ORCL) surged 12.7% after hours and Revolution Medicines, Inc. (RVMD) rocketed 41.4% on cancer trial news, the smart money crowd quietly dumped $2.6 billion versus just $456.2 million in purchases—a $2.2 billion net outflow that tells a different story than the headline rips. Rep. April Delaney (D-MD) was among the rare buyers, adding Rollins, Inc. (ROL) shares worth up to $15,000, while four insiders at Lingo Telecom (LGN) collectively unloaded a staggering $1.7 billion in what might be the exit of the year. Here's what smart money is doing today.

📚 Jargon Buster

Regarded

Highest compliment on WSB. “This DD is so regarded I just YOLO’d my rent money.” Thank you for your service.

The VIX declined nearly 20% this week to settle at 19.23, returning to normal levels after pulling back from elevated fear territory, suggesting equity market participants are experiencing reduced anxiety about near-term stock price swings. Meanwhile, the MOVE index measuring bond market volatility surged 74.6% to 13.29, though it remains at historically low absolute levels, indicating fixed income markets saw a notable pickup in expected price fluctuations even as they stay relatively calm. This divergence shows equity volatility cooling while bond volatility heated up from an extremely subdued base, reflecting different risk dynamics across the two asset classes.

|| Market Sutra ||

"Momentum is the shadow of conviction."

— Apple's repeated earnings beats kept reinforcing long-term conviction

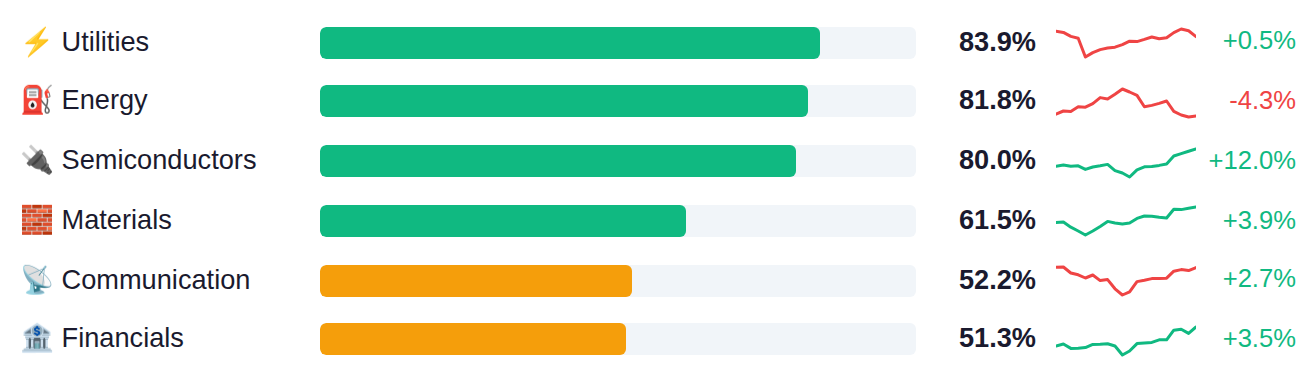

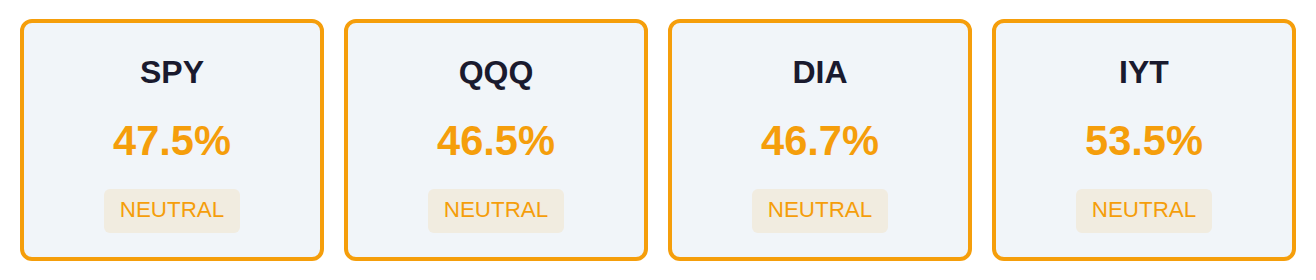

Market breadth remains tepid across major indices, with the S&P 500, Nasdaq, and Dow all showing fewer than half of their components above key moving averages, while the transport index demonstrates marginally stronger participation at 54%. A notable sector divergence has emerged, with Utilities, Energy, and Semiconductors exhibiting strength above 80% internal breadth, contrasting sharply against defensive Consumer Staples and growth-sensitive Healthcare and Consumer Discretionary sectors languishing below 35%. This split between select cyclical leadership and broad-based weakness in consumer-facing sectors suggests an uneven market structure despite pockets of concentrated strength.

As of April 8, Fed net liquidity stands at $6.69 trillion, up $18.5 billion week-over-week, indicating an expansion in system-wide liquidity that historically correlates with supportive conditions for risk assets. The next H.4.1 release is scheduled for Thursday, April 16, which will show whether this liquidity injection continues or reverses.

Existing home sales fell 3.6% month-over-month in March to 3.98 million annualized units, missing the 4.06 million estimate and marking the lowest level since October 2023 as mortgage rates hovering above 6.5% continue to freeze the housing market. Today's focus shifts to producer-level inflation with the PPI expected to accelerate sharply to 1.2% from 0.7% the prior month—a significant 0.5 percentage point jump that would represent the fastest monthly gain since February 2023 and likely reflects the recent surge in energy prices. Tomorrow brings a packed calendar including the Fed's Beige Book and import prices data expected at 2.0% versus 1.3% prior, with the combination of elevated wholesale and import inflation potentially complicating the Fed's rate-cut calculus while three Fed speeches today could provide clues on policymakers' evolving views on the inflation trajectory.

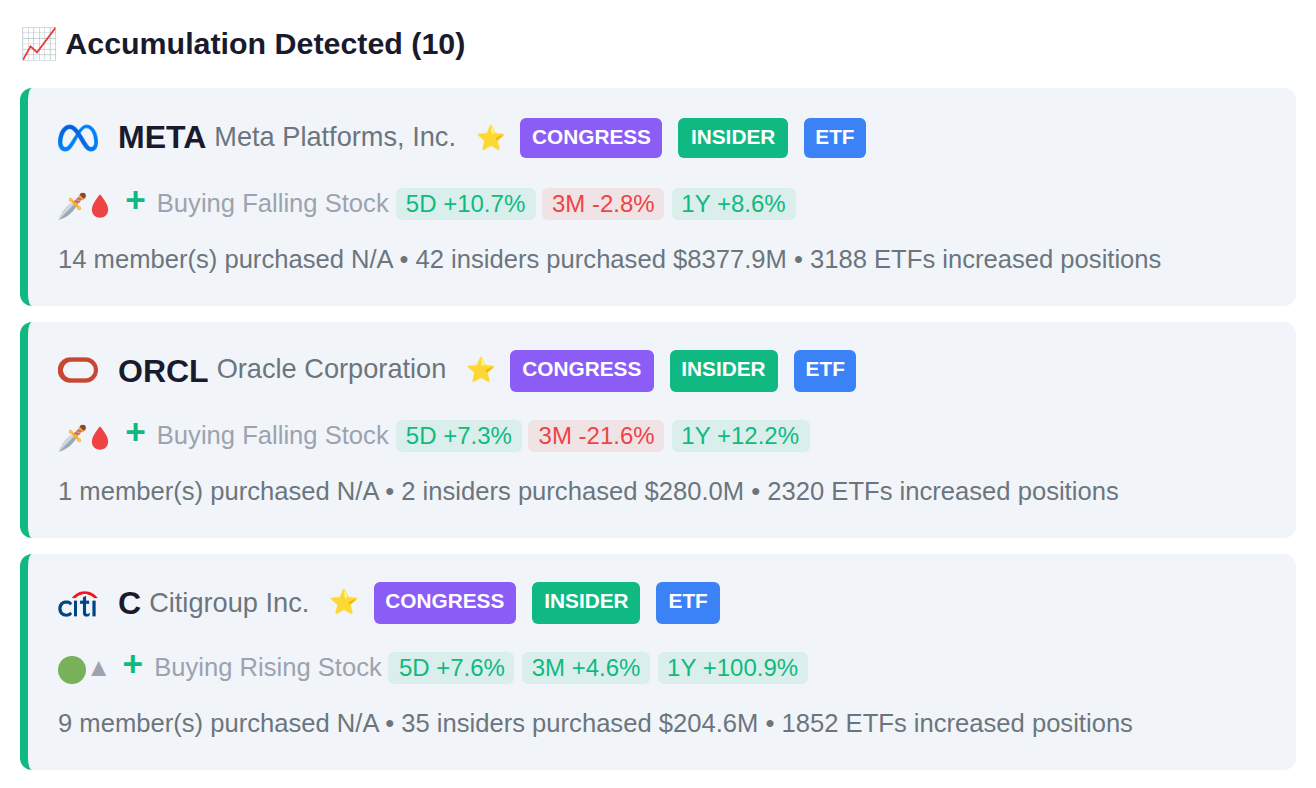

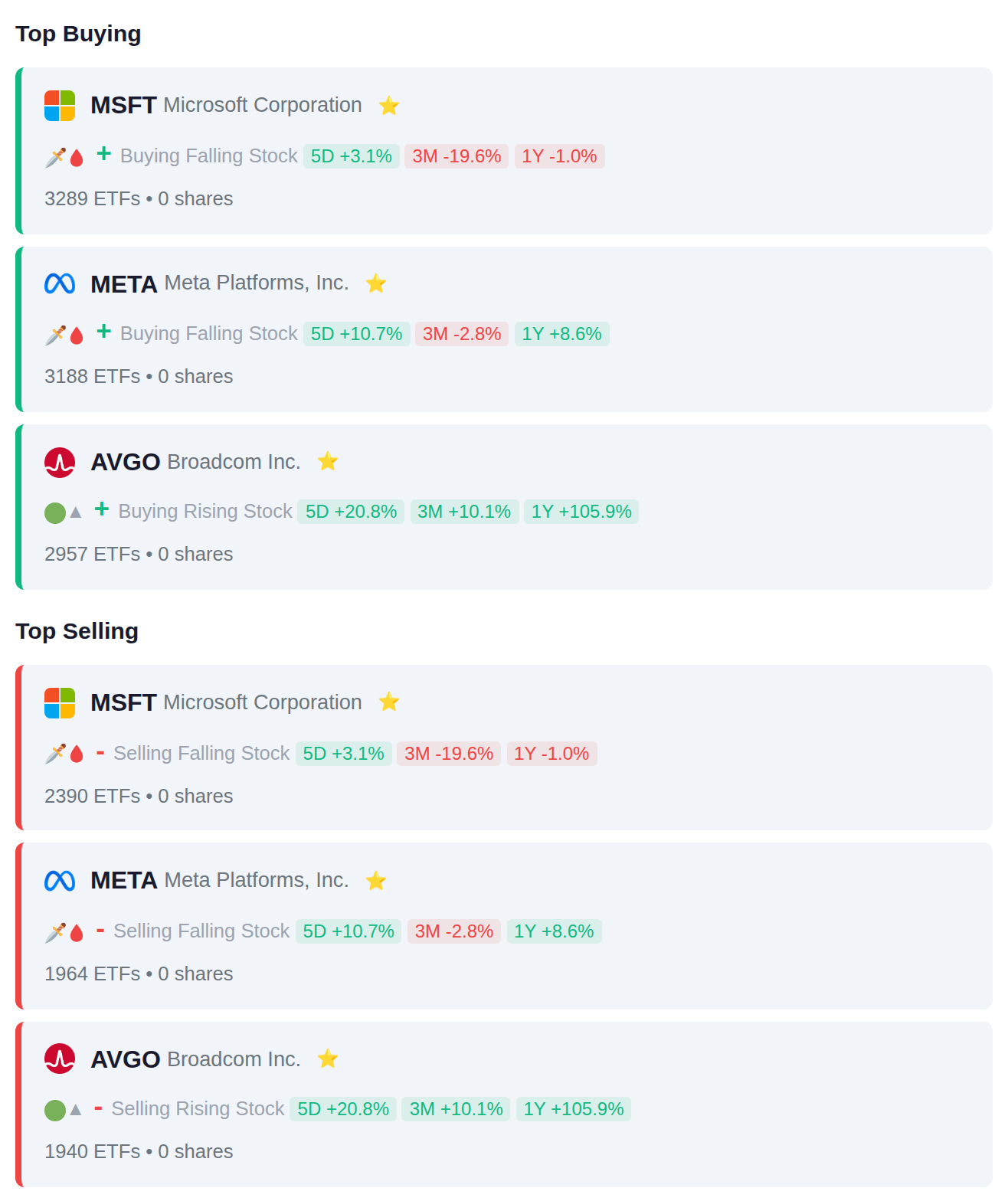

## Institutional Flow Summary Technology remains the primary battleground for ETF positioning this quarter, with **3,289 funds adding Microsoft**, **3,188 adding Meta**, and **2,957 adding Broadcom**, while a smaller but significant cohort reduced exposure (2,390, 1,964, and 1,940 funds respectively). The split decision—10 ETFs net adding versus 10 net removing—suggests institutional investors are **rotating within mega-cap tech** rather than abandoning the sector, potentially favoring AI infrastructure plays over broader technology exposure.

Rep. April Delaney purchased shares of Rollins Inc. (ROL), Tractor Supply Company (TSCO), and Vanguard S&P 500 ETF (VOO), while Rep. Michael McCaul also added a position in VOO but reduced holdings in Shell PLC (SHEL), ASML Holding (ASML), and Woodward Inc. (WWD). Both representatives showed activity in the broad market S&P 500 index fund, while McCaul's transactions indicated a shift away from international energy and semiconductor exposure.

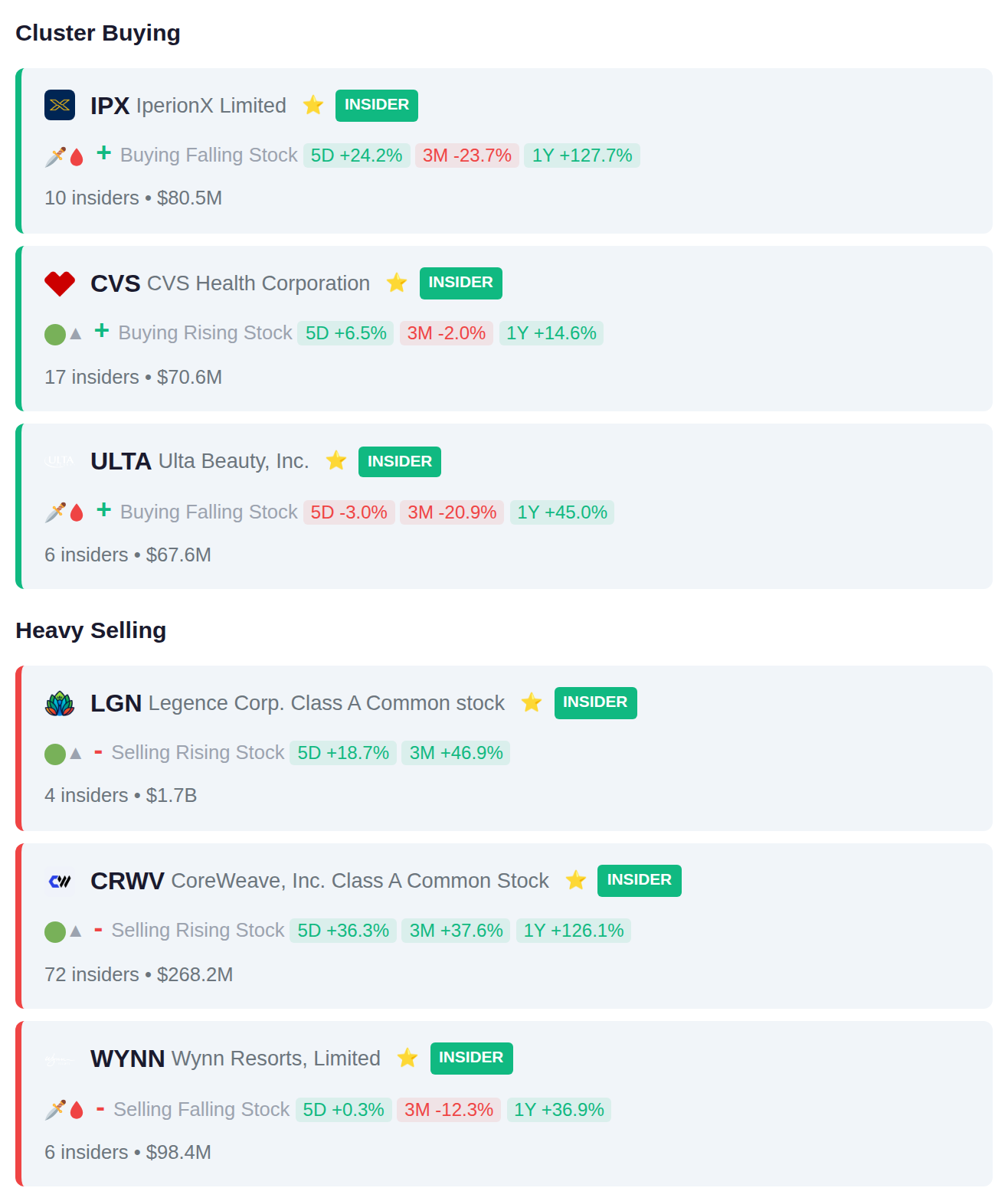

Last week saw notable cluster activity with 17 insiders at CVS Health and 10 insiders at IPX acquiring shares, while 72 insiders at CRWV collectively sold $268.2 million in stock. The activity resulted in balanced signals overall, with 15 accumulation patterns matching 15 distribution patterns across tracked companies.

Today's earnings calendar features 244 companies reporting results, with notable smart money activity surrounding several names. JPM.NE and 0Q1F.L have recently shown accumulation signals from informed investors ahead of their reports, while 9602.T and ICICIPRULI.BO have experienced distribution activity. Yesterday's session saw significant price movement with 002439.SZ climbing 12.8% and ATX.V gaining 9.1%, while 3349.T declined 5.5%.