The Edge

Know What They Know

🐷 PIG ROAST

💬 Word on the Street

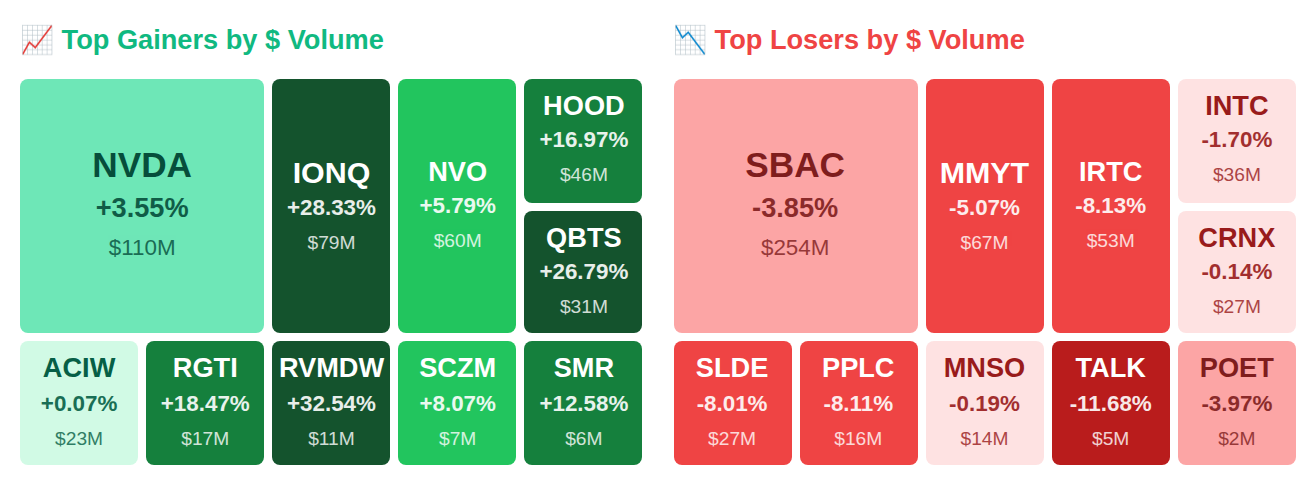

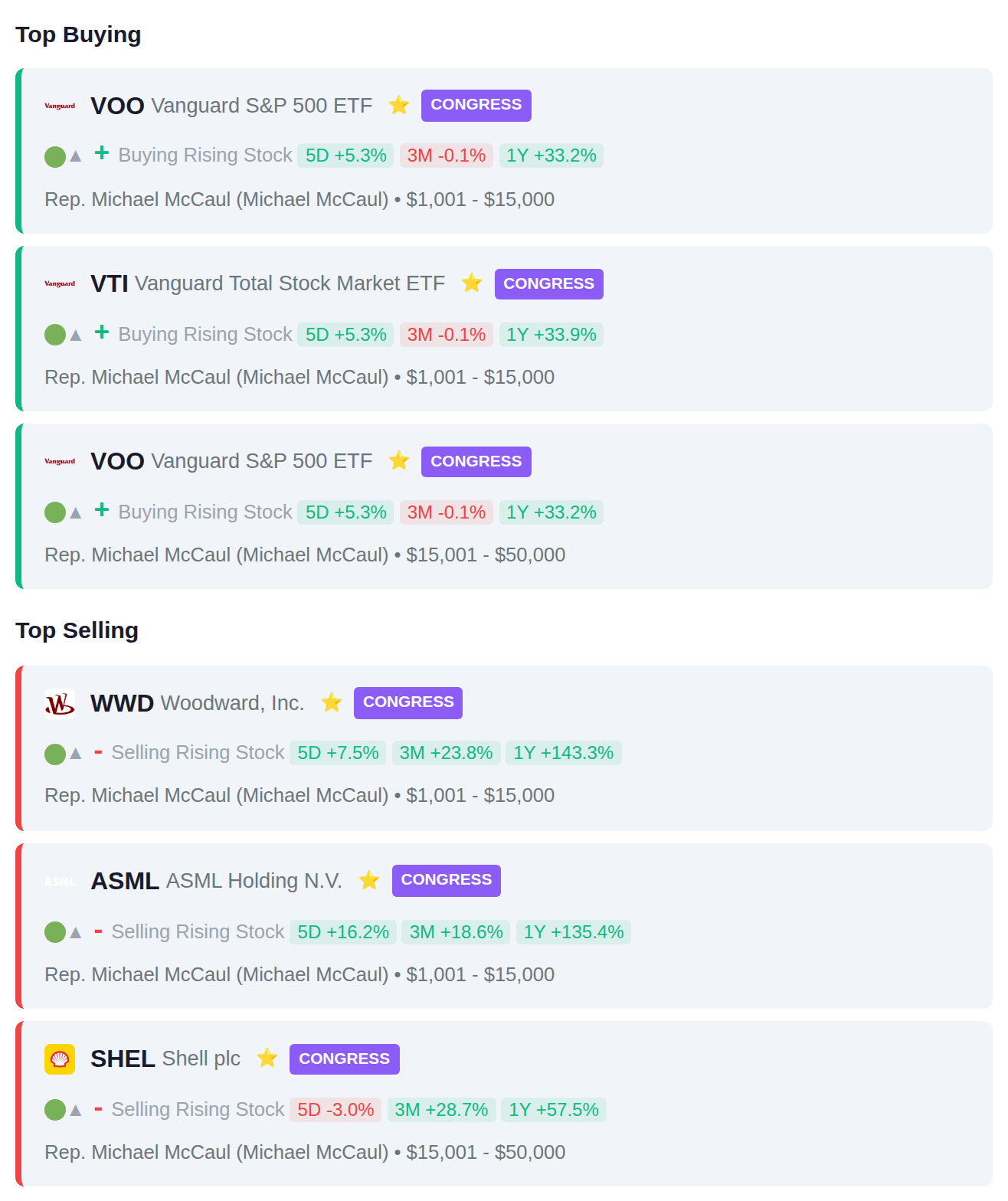

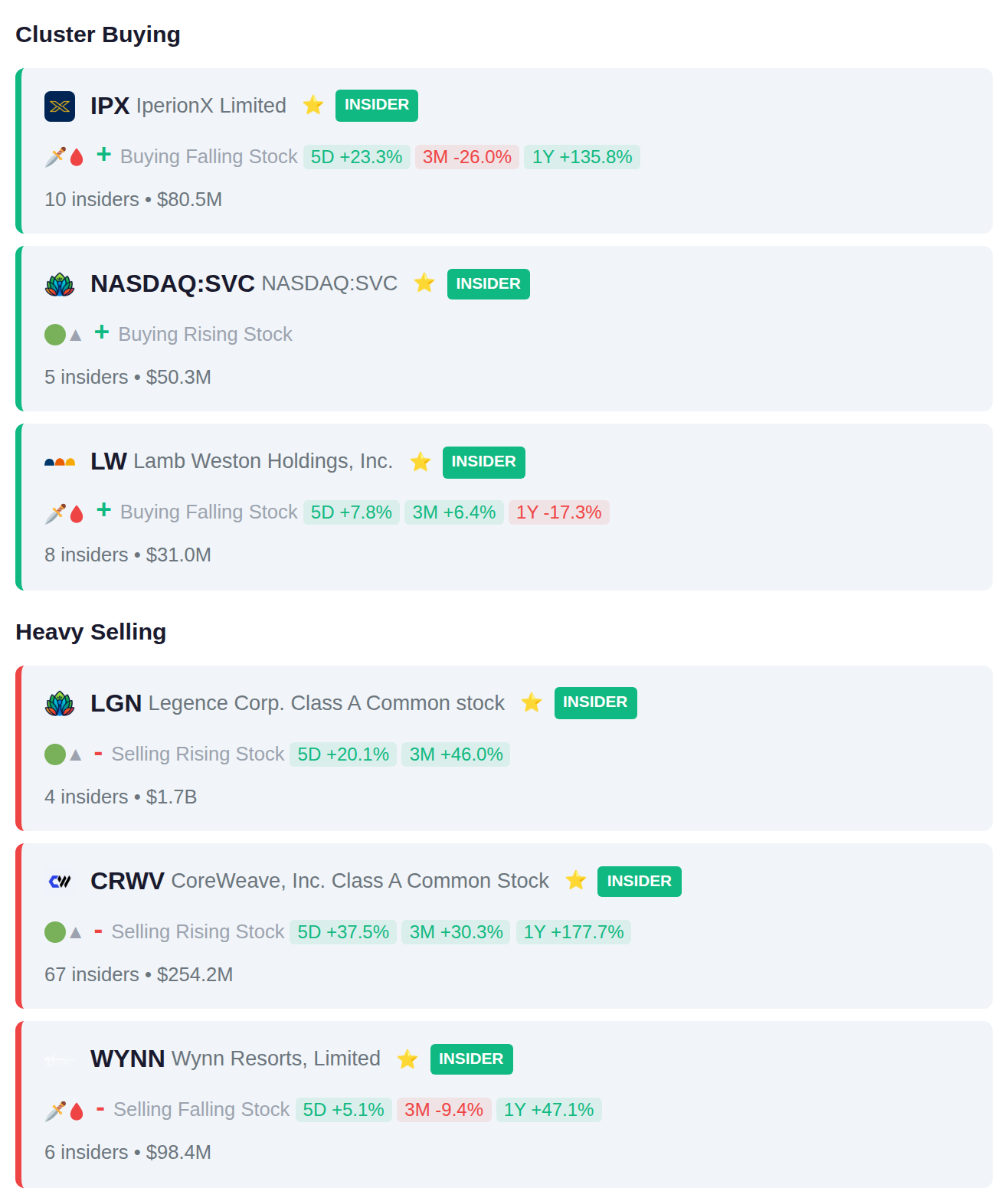

While Rep. Michael McCaul (R-TX) quietly scooped up VOO shares and volatility collapsed 20.9%, insiders at Live Nation Entertainment (LGN) dumped $1.7 billion in a single day—part of a $2.3 billion net outflow that tells a very different story than the headlines. Oracle's massive 2.8 gigawatt deal sent Bloom Energy Corporation (BE) rocketing 24% after hours, and Bernstein's $130 price target sparked a 10.3% surge in Robinhood Markets Inc. (HOOD), but the smart money's selling-to-buying ratio suggests the sharks are swimming in a different direction. Here's what smart money is doing today.

📚 Jargon Buster

Inverse WSB

Whatever the sub is piling into this week, short it and buy your real lambo in 18 months.

The VIX declined sharply to 19.12, falling over 20% week-over-week and settling into normal range after a period of elevated concern in equity markets. Meanwhile, bond market volatility told a different story as the MOVE index surged 32% to 16.02, signaling increased uncertainty in fixed income despite remaining at historically low absolute levels. This divergence suggests equity traders have grown more comfortable while bond market participants are pricing in greater rate uncertainty or duration risk.

|| Market Sutra ||

"The hardest part of a rally is believing in it."

— Early 2009 felt like the world was ending, not beginning a bull

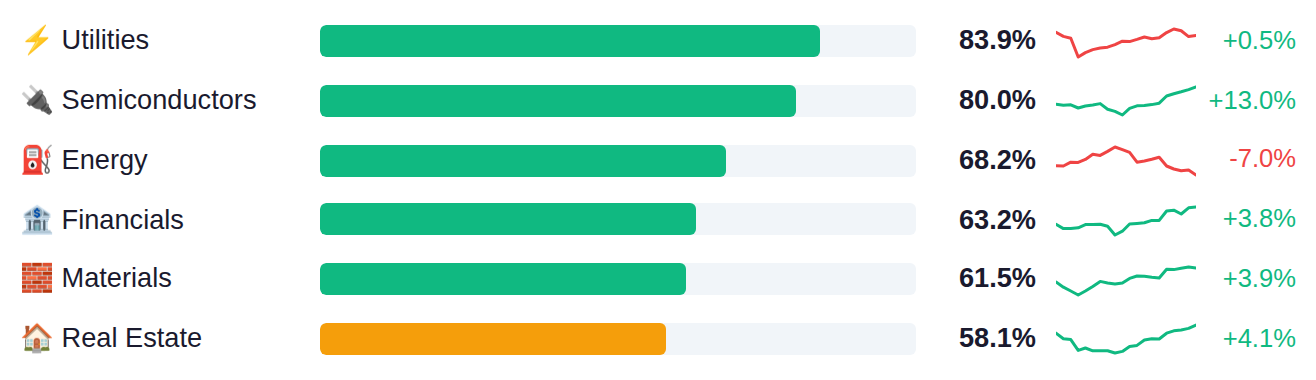

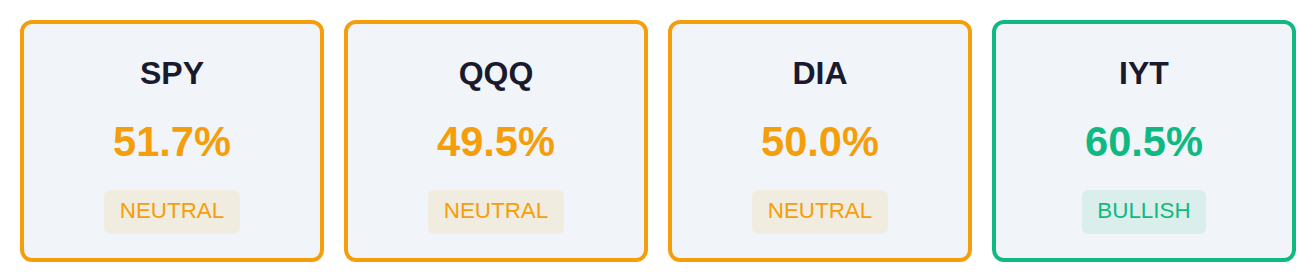

Market breadth remains narrowly balanced with major indices showing tepid participation between 50-52%, though transports display slightly healthier internals at 60%. A notable divergence has emerged as defensive Utilities lead at 84% while traditional risk-on sectors like Semiconductors maintain 80% strength, even as consumer-facing segments including Discretionary, Healthcare, and Staples significantly lag in the 31-40% range. This mixed leadership pattern, combining both defensive positioning and select technology strength alongside consumer weakness, suggests investors are navigating conflicting signals about economic conditions and growth trajectories.

As of April 8, Fed net liquidity stands at $6.69 trillion, up $18.5 billion week-over-week, indicating an expansion in system liquidity that historically correlates with supportive conditions for risk assets. The next H.4.1 release drops Thursday, April 16, which will show whether this liquidity expansion continues or reverses.

Yesterday's producer price data delivered a significant cooling signal, with headline PPI coming in at 0.5% versus the 1.1% estimate—a 60 basis point beat—while Core PPI printed at just 0.1% against expectations of 0.5%, suggesting wholesale inflation pressures moderated sharply in March despite recent tariff concerns. The API crude inventory build of 6.1 million barrels versus the expected 1.3 million drawdown points to weakening demand dynamics that could reinforce disinflationary trends, though traders will look to confirm this with today's official EIA report (estimated at +2.1M). Market attention today shifts to the Fed's Beige Book for qualitative insights on tariff impacts across districts, while tomorrow's retail sales and jobless claims data will test whether consumer resilience is holding—initial claims are expected at 215K versus last week's 219K, and any upside surprise in continuing claims (estimated 1,840K versus 1,794K prior) would signal labor market softening that could accelerate the Fed's rate-cut timeline.

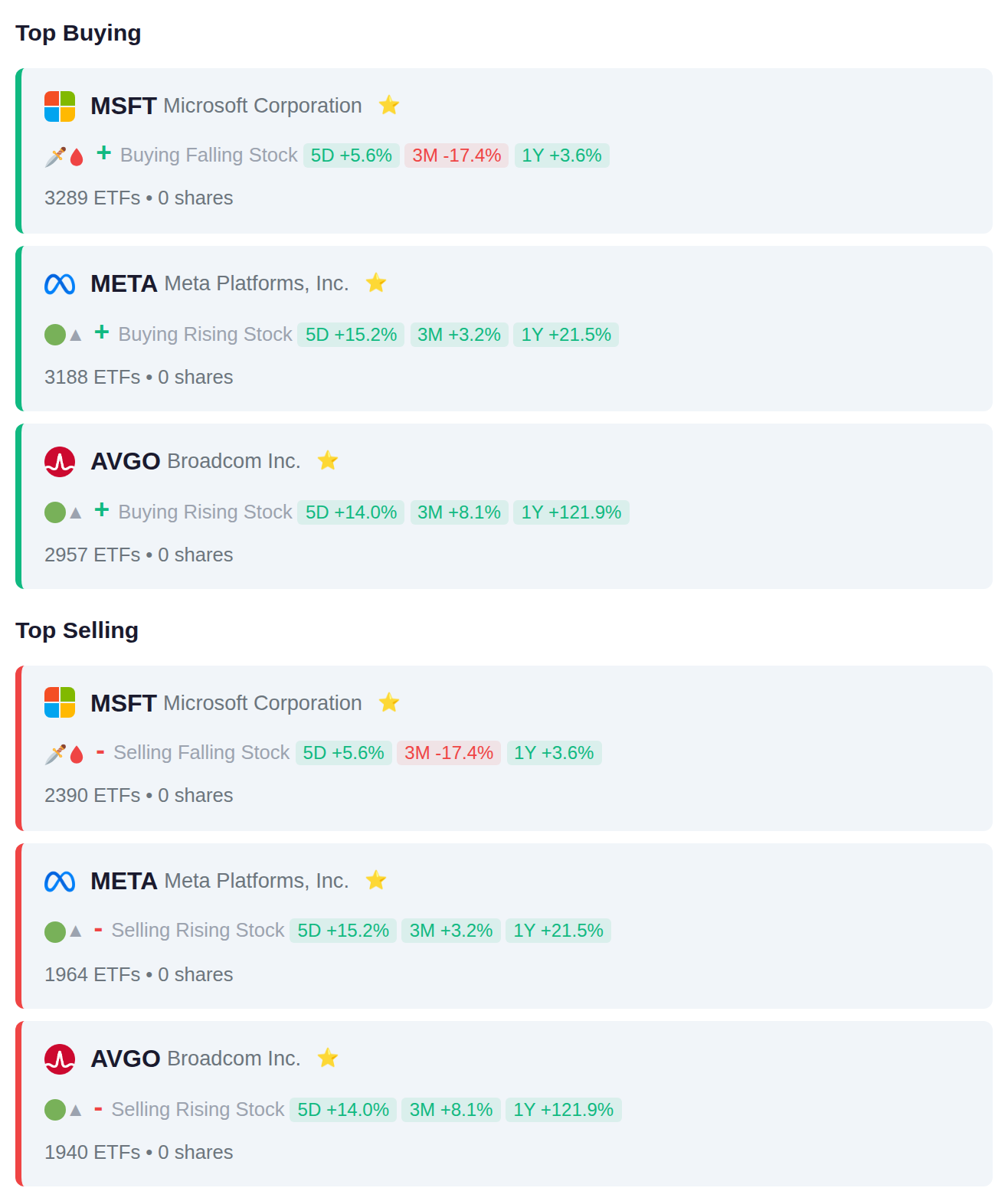

Large-cap technology continues to see mixed institutional positioning, with approximately 3,200 ETFs adding exposure to mega-cap names like MSFT and META while roughly 2,000 ETFs trimmed these same positions—suggesting sector rotation within tech rather than broad exits. The split activity in semiconductor exposure via AVGO (2,957 adding vs 1,940 removing) mirrors the divided institutional sentiment across the technology sector as funds rebalance between growth segments.

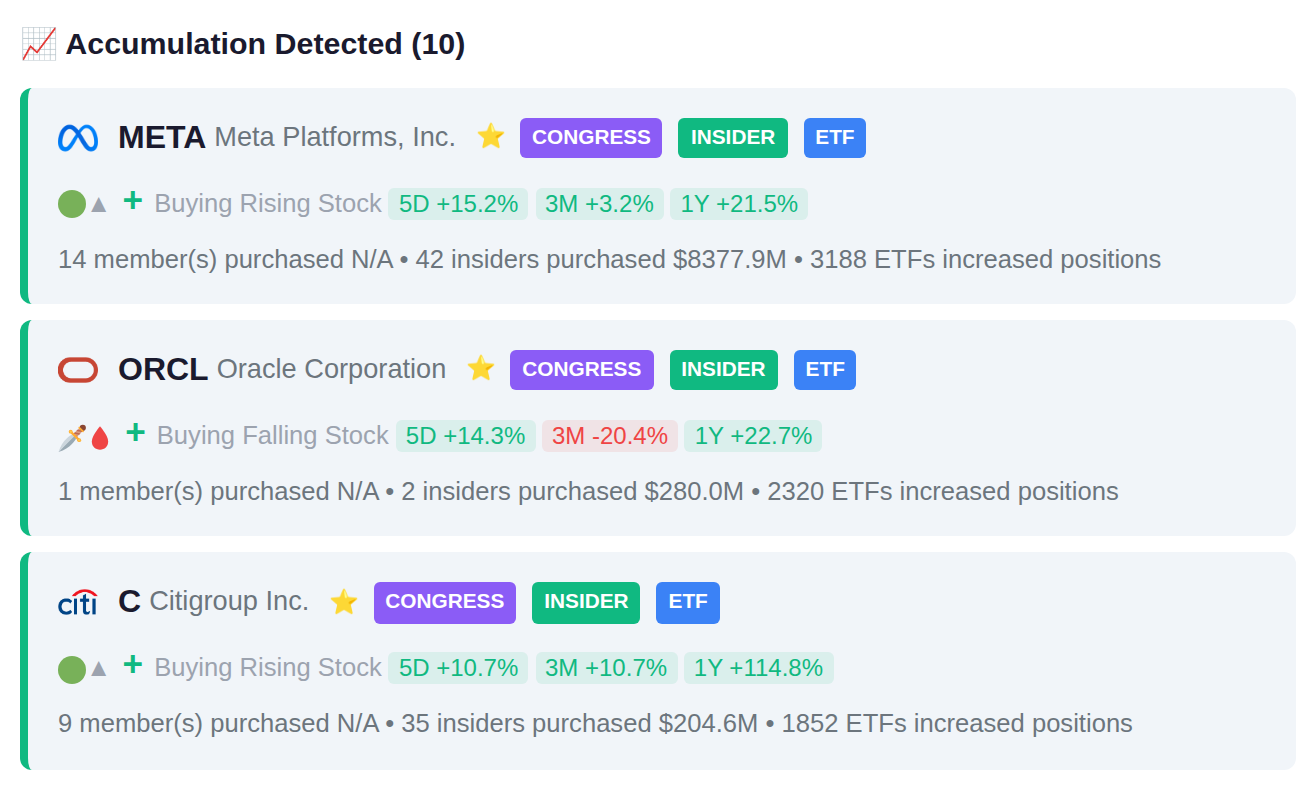

Rep. Michael McCaul recently executed multiple transactions, purchasing broad market index funds VOO and VTI while selling individual stock positions in WWD, ASML, and SHEL. The trading pattern shows a shift from individual company holdings toward diversified index fund exposure.

Notable cluster activity this week shows 10 insiders purchasing shares of IPX while 8 insiders added positions in LW, representing coordinated accumulation activity. On the distribution side, 67 insiders at CRWV collectively sold $254.2M in shares, followed by insiders at LGN offloading $1.7B across 4 transactions and 6 insiders at WYNN reducing positions by $98.4M.

Approximately 160 stocks report earnings today, with accumulation signals present in UNH.BA and 3750.HK ahead of their results. Distribution signals have emerged in BACRP and ICICIGI.BO, which also report today. Yesterday's session saw notable moves in 0QZZ.L, which gained 11.8%, ATX.V up 11.6%, and C advancing 10.7%.